")

Investment overview

I give a buy rating for Aramark (NYSE:ARMK) as there is a visible path for the top line to continue growing, supported by both volume and pricing, and margins to expand based on historical and peer performance.

Business description

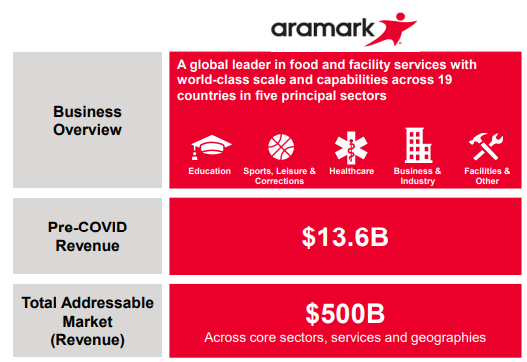

ARMK is a leading global contract catering operator (its previous uniform segment has been spun off as Vestis). Business segment wise, ARMK reports two business segments: US Food and Support Services [USFSS], which is ~72% of 2Q24 revenue, and International Food and Support Service [IFSS], which is 38% of 2Q24 revenue. The business serves a wide range of verticals, from healthcare to education to businesses and even correctional facilities. ARMK primarily competes with Sodexo and Compass.

Growth supported by volume and pricing power

I see a visible path for ARMK to continue growing revenue via both volume growth and an increase in prices. Below, I discuss my thoughts on each of these drivers.

ARMK

Starting with volume, there is still plenty of room for ARMK to capture share as the total addressable market [TAM] is estimated to be around $500 billion (as per the 2022 investor update), and based on ARMK’s latest run rate revenue (1H24 revenue of ~$8.61 billion), it only has less than 5% market share. If we combine the revenue from the other two players (Compass and Sodexo), the top three players only account for ~17% of the market share.

May Investing Ideas

Scale matters a lot in this industry, as it provides significant cost advantages in several areas. The biggest advantage is the ability to source food ingredients at a cheaper price than a subscale player, as it has sufficient volume to negotiate a cheaper price (this has been repeatedly mentioned in past earnings calls). Remember that this is a food catering business, so a large part of the underlying cost is the cost of goods sold. Additionally, scale is important because of route density. Having customers densely located near each other enables better labor efficiency (fixed cost leverage, as the cost of labor to deliver ingredients or food is fixed). Put together, this translates to a structural cost advantage that enables scaled players to outcompete subscale players when it comes to pricing.

I believe the trend of outsourcing to a specialist provider will continue, as outsourcing to a specialist provider removes the challenges of running catering services in-house. This basically reduces the fixed cost of a business, which I believe is a priority in the current operating environment, where high rates have forced many businesses to relook at their cost structure.

May Investing Ideas

ARMK’s latest quarter performance continues to show that volume is strong across different verticals. Within the U.S. business, reported revenue growth was 13% y/y in Sports, Leisure & Corrections, where attendance levels and per capita spending for sports and other activities remained strong. Management also called out the growing presence in college sports. Education revenues grew by 6% y/y and Business & Industry grew by 16%, aided by both new business wins and increased participation. Internationally, every country and region within the ARMK portfolio saw organic revenue growth.

Next, regarding pricing, as I noted above, while catering is a competitive market, the industry is led by three big players. Their large scale not only enables them to have economies of scale in food procurement, but it also allows for more sources of differentiation. For instance, large players can afford better quality, breadth, and variety of the food proposition for the end customer, which allows a degree of pricing power. As such, ARMK should have no issue raising prices in accordance with inflation rates. Management has also commented in the recent Bairds conference that their approach to pricing is to be consistent with inflation levels.

ARMK’s historical organic growth performance supports my claim. The business has almost always reported positive organic growth except during the subprime and COVID periods, which is understandable as businesses get shut down (contract loss for ARMK). This track record of growth also suggests that ARMK has a relatively resilient business model (unless there are major macro-events)

Margin upside

May Investing Ideas

I believe ARMK’s current EBIT margins have plenty of room to improve from here, which will drive faster earnings growth than revenue. Historically, as ARMK scaled bigger, margins have improved accordingly (in line with my view that having scale leads to structural cost advantage), touching a high of ~8% before COVID happened. There are few reasons to believe why margins would be structurally lower today, despite ARMK having a larger scale. Compass Group (the largest player in the world) saw a similar trend like ARMK, where the EBIT margin fell off the cliff from ~8% to -3.3% in 2H20 but has since rebounded by to ~7.4% as of 1H24. As such, I expect margins to recover back to historical levels in the next couple of quarters (margins actually did recover back to ~6.5% over 3+ years).

Based on my understanding, margins are depressed at the current levels because of the large contract wins over the past few years. Given that it takes time for on-site margins to mature (mentioned in the 1Q23 earnings call that it takes a few years to mature), margins should eventually inflect upward.

Our growth-focused strategies are working, and we are seeing favorable margin trends driven by prior year’s new contract maturities, scale efficiencies in our purchasing and tight SG&A cost management, and which has been helped by moderating inflation. Company 1Q24 earnings

Valuation

ARMK May Investing Ideas

Based on my research and analysis, I see an attractive upside to ARMK.

- Given the visibility of upcoming revenue (due to the contractual nature of the business), I trust the guidance that management put out for FY24, in that revenue will grow by 9% organically and adj operating income will grow by 18.5% (midpoint of the 17–20% range). Management was implicitly guided to an adj. EBIT margin of 5.9% in FY24 (50 bps expansion). Given that ARMK continues to add new contracts (and has one large contract recently), expanding back to ~8% margin might take a while. Assuming the same 50bps expansion rate, I believe ARMK can continue to grow adj EBIT at >10%, achieving $1.3 billion in FY26. I then convert this to GAAP EBIT using historical rates.

- Stock should continue to trade at a discount to Compass, given that margins are still lower. Compass currently trades at 16x forward EBIT, and ARMK trades at 15x forward EBIT. I expect ARMK to continue trading at 15x.

Risk

Growing adoption of work-from-home practices is a major growth headwind for ARMK, as it means fewer employers in physical offices (or on-site). This impacts ARMK on two levels. One is that there will be fewer opportunities for new business wins. On-site revenue (less spending per capita) will see a decline. Major macro-events like subprime or COVID will cause ARMK financials to suffer, just like they did in the past.

Conclusion

I give a buy rating for ARMK as I expect it to continue capturing share in this large and growing market. Its competitive advantage, stemming from its scale, should provide cost advantages in both procurement and logistics. Additionally, margins have room for improvement as recent contract wins mature. The risk is that more businesses will adopt work-from-home, which will cause less demand for on-site catering services.

Read the full article here

")

")

")

")

")