“The most fun I had going to see the new Joker movie was in the car ride to and from it, because I was listening to Warhammer 40K lore on the Horus Heresy. And just listening to that was better than seeing Joker Folie a Deux”")

Shares of Brighthouse Financial (NASDAQ:BHF) have been a poor performer over the past year, losing 19% even as other annuity providers like Jackson Financial (JXN) and Equitable (EQH) have rallied. The pain is likely to continue, with BHF reporting a very disappointing Q2 on Tuesday. I last covered BHF in May when I opted to keep shares a “buy” despite a weak Q1. In hindsight, I gave too much attention to its low valuation and not enough to its weak results, with shares subsequently down 5%, and I should have downgraded shares three months ago. Given a more troubling Q2, I am downgrading shares now and would not buy on this weakness.

Seeking Alpha

Statutory results were problematic

In the company’s second quarter, Brighthouse earned $5.57 in adjusted EPS, beating by $1.20. This would seem like good news for investors; however, insurers generate both GAAP, or financially reported results, as well as a separate set of financials for statutory purposes, which is what regulators use. Accounting regulations around liabilities and hedges vary for its different set of financials, so while BHF reported a profit to shareholders, it lost $600 million on a statutory basis.

As you can see below, Brighthouse now has $5.4 billion of statutory capital, down from $6 billion in Q1 and $7.6 billion last year. Because of this decline, its statutory risk-based capital (RBC) ratio is now between 380-400%. It is important to see most insurers operate consistently above 400%; given BHF’s business mix, I like to see 400-450%. BHF is now running below this level.

Brighthouse Financial

Now to be clear, this is not even remotely close to solvency challenge for the company, and over time, statutory results should improve. However, lower capital will constrain its ability and willingness to sell new products, reducing growth and slowing its transformation into an insurer with less risky products. More impactful, lower capital reduces the capacity of Brighthouse to dividend funds from the insurance entity to the holding company.

Cash flow will be constrained

Most of these dividends require regulatory approval, and with lower capital, there will be a need to retain more capital inside the insurance company. This is significant because the holding company is the entity that makes share repurchases. Now, Brighthouse’s Holdco has $1.2 billion of liquid assets, which means it can operate a few years without any dividends.

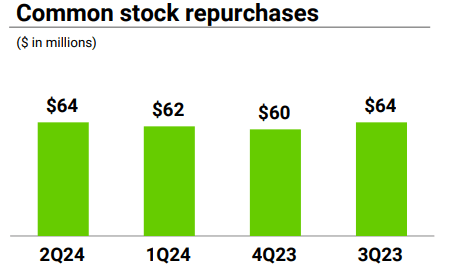

As a consequence, Brighthouse management opted to continue with buybacks in Q2, doing $64 million. It also has done $25 million quarter to date, and it plans to continue with this buyback program. Thanks to these buybacks, its share count is down about 7% over the past year.

The holding company has excess liquidity, so BHF can afford to do this; however, it is a somewhat aggressive financial policy. Regardless, it is always preferable to see capital returns supported by underlying cash flow rather than be funded simply by draining liquidity, especially as with recent market volatility, I am concerned BHF’s RBC ratio could deteriorate further in Q3.

Brighthouse Financial

Management expects to get RBC back above 400% and closer to target over “six to twelve months,” which is why it can continue to repurchase stock. Given recent volatility and the fact that the company has now reported a string of disappointments from increased reinsurance expense to declining statutory capital, I expect this to be more of a 12-month than a 6-month project.

Shield sales are consuming capital

Drilling into reported results, annuities adjusted earnings rose to $332 million from $291 million last year. Sales declined by 3% to $2.4 billion due to weaker fixed index activity. Given a high level of surrender activity, net flows were $-1.5 billion. Given the rise in rates relative to several years ago, policyholders are terminating old policies with low rates. This action leads to a surrender fee and boosts BHF’s profits.

In the near term, more surrender activity can help temper its asset growth and assist its capital rebuild. Still, even with negative flows, account values rose by $7 billion to $144.4 billion due to higher markets. This higher asset base supports increased fee revenue going forward. Even with capital constraints, BHF did over $2 billion in Shield annuity sales, a record.

As discussed last quarter, this growth in Shield policies has become a capital challenge. It originally hedges equity risk on its legacy variable annuities. However, the shield has grown so much, this hedge is now complete, meaning incremental policies need to be actively hedged. Shield was expected to consume about 5% of RBC/quarter. It was underwritten, ignoring the previous capital benefit. Given the significant capital drawdown, it is not entirely certain this is playing out as hoped.

Elsewhere, its run-off unit lost $30 million, due to weaker underwriting results. This was down from a $16 million loss last year, but better than the $48 million loss in Q1. Separately, its Life unit earned $42 million, after a $36 million loss in Q1. This unit lost an arbitration case with a reinsurer, which caused the weakness in Q1 results, and Q2 should be more of a representative run-rate.

Its investment portfolio remains secure

Beyond policies, BHF is benefiting from higher rates with $1.3 billion in net investment income from $1.2 billion last year. This strength came even as it earned 2.4% on alternatives vs a 9-11% expectation, given pressures on real estate valuations.

BHF had a $123 billion portfolio, and 97% of fixed income is investment grade, which should limit credit losses. Within the portfolio, $13.1 billion is in commercial real estate, my area of greatest concern. However, this portfolio has just a 66% loan to value and 2.3x debt service coverage. That LTV is largely based on a 2023 valuation, and just 13% of the portfolio has an LTV above 80%. As such, we would need to see significant further stress before BHF faces material losses. This is a risk to monitor, but I am comfortable with it.

Brighthouse Financial

Impaired dividend capacity leads me to downgrade BHF

Overall, Brighthouse’s free cash flow and dividend capacity to the parent is the primary question. Last year, it made a $350 million dividend payment. Due to shield becoming more capital intensive, I had seen $300 million in dividend capacity this year. With the need to rebuild capital and increased market volatility subsequent to quarter end, BHF needs to rebuild several hundred million dollars of capital, a year-long process.

In the interim, BHF can spend down holding company assets to maintain the pace of buybacks, but this is a temporary solution. More structurally, its ability to consistently dividend up capital to return to shareholders is increasingly uncertain, and for the next 2-3 years, dividends may average closer to $150-200 million, giving shares a sub-8% yield on free cash flow.

Last quarter, while rating BHF a buy, I noted a preference for Jackson, which continues to have 500+% capital, enabling it to much more sustainably return capital to shareholders. I would reiterate my preference for JXN. With its strong holding company liquidity giving BHF time to right the ship, I am not downgrading shares all the way to sell, instead just “hold.” But with JXN a “strong buy,” I emphasize there are better options in the insurance sector, and after yet another disappointment, I would not buy the dip on BHF.

Read the full article here

")

")

")

")

")