")

Chris, it’s Marvin. Your cousin, Marvin Martin. You know that new sound you’re looking for? Well, listen to this")

Introduction

If you’re a dividend investor or someone highly focused on income generation, then REITs deserve a spot in your portfolio. But like anything, all REITs are not created equal. When selecting companies for income generation, I think investors should have a good mix of growth & income stocks.

There are other stocks or sectors that are good investments as well, but REITs are usually a good addition as a result of their business structures. One REIT in particular that I think deserves a spot in your portfolio is CareTrust REIT (NYSE:CTRE). In this article, I discuss the company’s latest earnings, fundamentals, and why they deserve a spot in your portfolio.

Previous Thesis

I last covered CareTrust REIT in early April in an article titled: This Near 5% Yielding REIT Is A Great Long-Term Buy For Dividend Investors. The title is pretty self-explanatory as I’m high on the company’s future. Since then, however, the REIT’s share price has been relatively flat in comparison to the S&P which is up roughly 5%.

This is good for investors as interest rates are likely to decline in the near future, possibly providing some strong upside to the sector going forward. I touched on the company’s performance over the past year vs its peers, which saw CTRE up nearly 27%. Impressive considering the downward pressure the high-interest rate environment has caused on the REIT sector. I also touched on their dividend safety and balance sheet, both of which were solid.

Positioned For Further Growth

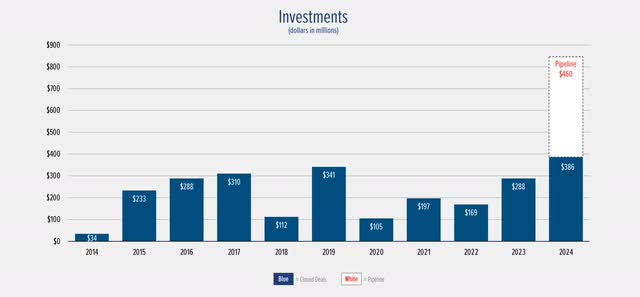

The main reason why I think CareTrust REIT deserves a spot in your portfolio is the accelerated growth the REIT has been seeing over the past year. During their Q1 earnings back in May, they managed to continue this closing on more than $200 million worth of new investments.

So far, they’ve made nearly $400 million in acquisitions alone. For context, this is higher than the $288 million they achieved in 2023. Year-over-year, their property count significantly grew from 205 properties and 18 operators to 297 properties and 30 operators!

They entered into new states as well. This grew from 24 states to 30 over the same period. In the chart below, you can see CTRE has been on an acquisition spree over the past two years. And this is expected to continue as management has nearly a half of billion of additional acquisitions in its pipeline.

investor presentation

Earnings & Dividend

Moreover, with interest rates projected to decline in the next few months, I expect this to continue going into 2025. However, despite their impressive acquisitions, CTRE’s earnings have been relatively flat over the past year. For Q1, FFO came in at $0.35, missing analysts’ estimates by a penny. But revenue managed to grow more than 5% to $63.07 million, beating estimates by more than $3 million.

Their acquisitions have translated to impressive revenue growth, while their bottom line has remained relatively flat. Over the past year, revenue has grown from roughly $51 million in Q1’23 to $63 million in Q1’24 – a growth rate of nearly 24%. This is in comparison to peer Omega Health Investors (OHI), whose revenue grew nearly 11.5% from $218.2 million to $243.29 million over the same period.

Author creation

So, to be fair, both have seen some decent growth in their top lines, with CTRE besting their larger peer by more than double. But regarding CTRE’s bottom line, this has remained relatively flat in the past year. From Q1 of 2023 to now, FFO was the same at $0.35. Their peer OHI saw theirs tick up by $0.02 year-over-year from $0.66 to $0.68. Additionally, this declined by $0.01 in the previous quarter for CareTrust. FAD, or funds available for distribution, was also flat at $0.37 in both quarters.

One reason is the REIT only collected 98% rent during the quarter. The remaining 2% were from Senior Housing operators that haven’t been performing well as a result of headwinds from the current macro environment. But management expects to continue working through this with these tenants. And anticipates this to improve and collect future payments going forward.

Despite FFO & FAD coming in at $0.35 and $0.37 respectively in both quarters, both actually grew double-digits by 32.9% and 33.1% respectively. FFO was $46.5 million, while FAD was $48.7 million. For investors, higher funds available for distribution is better as this is similar to AFFO.

A higher FAD also signals that a REIT’s dividend is likely safer. However, this depends on if the company has been heavily diluting shareholders to raise capital, as REITs typically do. And considering the high-interest rate environment, this is a smarter move in comparison to borrowing at a high-interest rate.

Over the past year, CTRE has issued shares, growing their share count from roughly 99 million shares to 133.3 million at the end of their most recent quarter. Despite this, the dividend remains well-covered with $41.2 million in paid dividends in comparison to $48.7 million in funds available for distribution. This gives them a safe payout ratio of 85%.

Balance Sheet Supports Future Growth

I touched on the CareTrust REIT’s balance sheet during my last article, in which they had a very low net debt to EBITDA of just 1.4x. During Q1, they managed to lower this to an all-time low of just 0.6x, a level I have not come across in my years of researching REITs. This puts them in a very favorable position to continue making acquisitions for the foreseeable future. Additionally, this is well-below management’s target range of 4x – 5x.

Their cash & liquidity levels were also strong, with $345 million in cash on hand and $600 million on the revolver. This increased from $300 million at the beginning of the year. Their fixed-charge coverage ratio was also strong at 7.5x. Management touched on their low leverage, stating they wouldn’t be surprised to see this tick further down in the coming months, as they have been funding acquisitions with equity instead of debt.

According to their CEO, if they decide not to use equity and available liquidity, this would still put them at a very conservative 3.6x net debt to EBITDA. This is in comparison to OHI, who had a net debt to EBITDA of 5.03x and a fixed-charge coverage ratio of 3.9x.

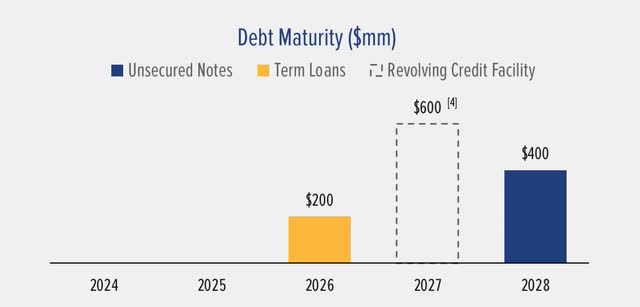

Sabra Health Care REIT’s (SBRA) net debt to EBITDA stood at 5.55x at the end of their most recent quarter. Both SBRA & CTRE’s debt maturities were well-staggered with little to no debt due until 2026 while OHI had $800 million total maturing in 2024 & 2025. And seeing by their well-staggered debt maturities, CTRE is poised for strong growth, likely surpassing its peers.

investor presentation

Valuation

At a forward P/FFO ratio of 17.1x using midpoint of guidance, I think CTRE is still a buy here, especially for long-term investors. This is in comparison to OHI’s forward P/FFO ratio of 12.1x. CTRE has managed to outperform OHI, which is the reason they command a higher valuation. Moreover, this will likely continue over the next few years as the REIT executes on its growth strategy.

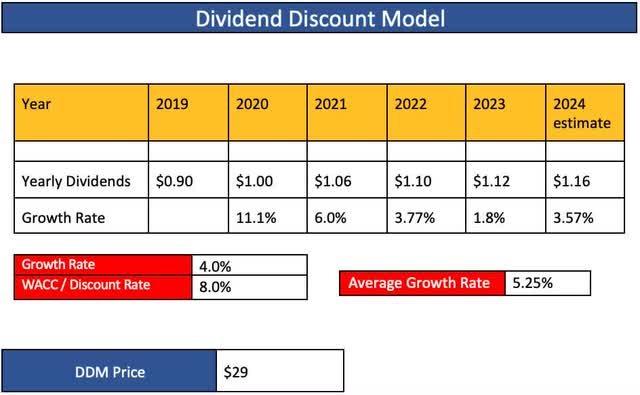

CareTrust REIT is expected to post some strong earnings growth over the next 3 years with an average growth rate of 7.2%, which is high for a REIT. And if they can execute, I suspect their share price will follow suite. Using the Dividend Discount Model, I have a price target of $29, roughly 18% upside. I also decided to be generous with a 4% growth rate, as CTRE is expected to post a higher growth rate in the coming years.

Author DDM

Risks & Conclusion

As previously mentioned, CTRE failed to collect rent from some of the senior housing operators, who also happened to be their weakest tenants. And while interest rates should decline in the coming months, this could very well push the economy into a recession if they’re not.

If so, the REIT could see additional tenants default on rent payments, negatively impacting their financials in an economic downturn. This would also impact their dividend safety, which is currently safe, but higher than I prefer to see. At 85%, this gives CTRE little margin for error and future tenant headwinds would likely push this higher, thus resulting in a sell-off.

Although I don’t anticipate this happening, this is something shareholders should be aware of going forward. However, CTRE’s balance sheet puts them in a comfortable position to work through this if need be. And as a result of their strong pipeline and upside potential, I continue to rate CareTrust REIT a buy.

Read the full article here

")

")

")

")

")