")

My Thesis

I’ve been covering Cleveland-Cliffs Inc. (NYSE:CLF) stock since June 2021, and all along I’ve been bullish on the stock for many reasons. The last time – in March 2024 – I argued that CLF had some reasons for margin expansion in the medium term, being driven by strong management (in my opinion) that prioritized buybacks and debt reduction. I advocated for buying the stock, which seemed undervalued in light of its superior projected growth rates in FY2025 and implied multiples that were well below those of its peer group. Since then, unfortunately, CLF has managed to significantly underperform the broad market, falling by ~22% amid the S&P 500 index’s (SPY) (SP500) return of 6.7%:

Seeking Alpha, Oakoff’s coverage of CLF stock

Despite the recent underperformance, I still think CLF is a solid medium-term pick for investors looking for growth stories in the steel industry. The company remains undervalued and the actual positive effect of future margin expansion, while delayed, is still a relevant catalyst to watch.

My Reasoning

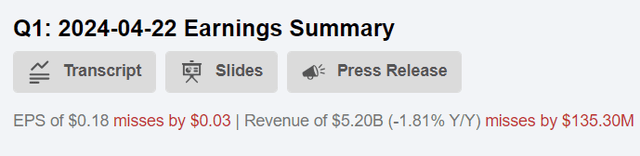

I can’t say CLF’s first-quarter results were as solid as I thought they would. The firm showed adjusted EPS of $0.18, which was below the consensus forecast of $0.22 but better than last year’s loss of $0.05 per share. The bottom line was impacted by “charges and losses totaling $202 million, primarily due to the indefinite idling of the Weirton tinplate facility and the loss on extinguishment of debt.” Organic revenue declined by 2% YoY to $5.2 billion ($135 million below the consensus), while adjusted EBITDA increased by 70%, with the EBITDA margin widening by 400 basis points to 8.0%.

Seeking Alpha, CLF

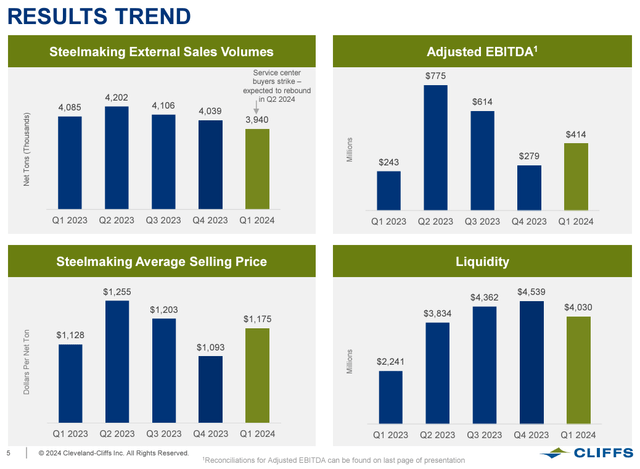

I was definitely pleased to see that the adjusted EBITDA began to show impressive growth, as I already noted above. Steelmaking average selling price was up 7.5% QoQ (+4.16% YoY) with external sales volumes decreasing by 3.55% compared to last year. However, according to the company’s latest IR presentation, CLF expects a rebound in service center buyers’ demand in Q2 2024. So, I think the company’s EBITDA growth in Q1 is just the beginning, given that the pricing remains more or less stable.

CLF’s IR materials

Also, important to note here that Cliffs maintained its outlook for 2024, including steel shipment volumes of 16.5 million net tons (vs. 16.4 million net tons in FY2023), and steel unit cost reductions of ~$30 per net ton. The company also expects to benefit in 2Q from lower costs under its guidance, which, given the forecasted increase in demand, sounds good. I believe the margin expansion assumptions outlined in my previous articles remain valid – this continues to be my baseline scenario.

In addition to the expectation of increasing orders from service center customers shortly and perhaps better margins thanks to rising spot pricing, the CEO Lourenco Goncalves said during the latest earnings call that the U.S. automotive production stays resilient.

<…> Our automotive business carried the day for us once again as the automotive sector in the US continues to improve, growing for the fourth consecutive year.

<…> But all in all, I see Q2 returning to a more — much more normal mix between service center and distribution and automotive. So automotive will continue to be good. Service center and distribution will become bigger, and that will bring the mix back to where the mix normally is.

The auto industry helped CLF offset a temporary buyers’ strike from service centers in January and February, and if the resilience stays in place – which I think it will, based on still-depressed auto inventory levels – we may expect a richer mix and better growth rates in the coming quarters.

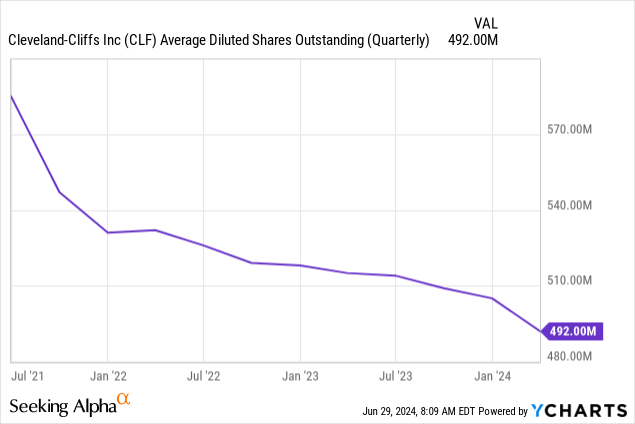

I like the way the company deploys its capital by skillfully balancing growth investments with worthwhile shareholder rewards. According to the press release, in Q1, Cliffs bought back ~30.4 million common shares, using up the remaining $608 million of its $1 billion share repurchase program at a mean price of ~$18.79 per share. After that move, the Board of Directors approved another stock repurchase program for a maximum amount of $1.5 billion, which will allow it to purchase shares “through open market or privately negotiated transactions”.

Seeking Alpha, CLF

Over the last 3 years, the buyback program has helped to significantly reduce the number of shares outstanding and based on the future plans and the new buyback program, we can expect this to continue, since the CEO called the stock repurchases “a better use of capital than any M&A opportunities at current valuations.”

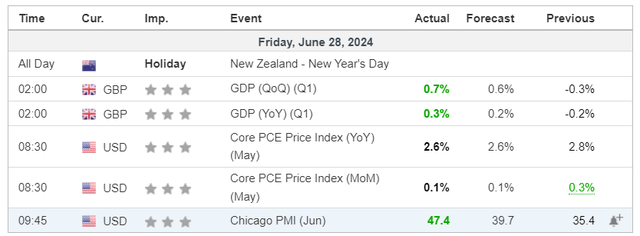

Attentive readers may wonder: if everything is as good as I describe, why has the CLF stock price fallen by 25% YTD and is still looking downwards? Recently, CLF has been downgraded by various banks (like JPM) and research agencies such as GLJ, which set the price target for CLF at around $10/share due to “overly optimistic Q2 estimates amid signs of an economic weakening”. However, as we can see from the latest Chicago PMI data, which came in much stronger than expected on Friday, GLJ’s assumption of a “weakening economy” may be far from the truth, as normally a higher-than-expected PMI indicates that the manufacturing activity in the economy is expanding, which usually reflects increased production and demand for goods.

Investing.com

Also, JPMorgan analysts shared concerns that CLF’s Q2 estimates could be overestimated and there are fears among investors about buybacks financed through debt. They added that after Q1, the buyback amount should fall and lower forward pricing, coupled with higher CAPEX, should result in less attractive FCF and overall shareholder returns. Furthermore, Morgan Stanley has also cut their price outlook for steel and scrap due to an accelerated decline in prices caused by softening demand.

Despite the risks described above, I continue to believe that CLF shares have great potential. Even after a number of investment banks almost simultaneously lowered their forecasts for CLF’s sales and earnings per share, we see that their relatively depressed estimates assume earnings growth of 128.26% in 2025, giving an implied price-to-earnings ratio of just over 11x:

Seeking Alpha, CLF, Oakoff’s notes

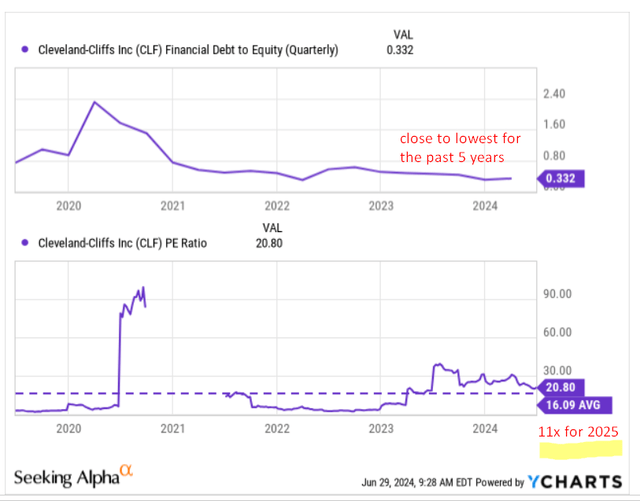

I understand that many are concerned about the debt burden on the company’s balance sheet, but nevertheless, the 11x P/E figure for 2025 is an undervaluation of ~31.25% compared to the 5-year average multiple, when in fact the debt-to-equity ratio is around the lowest in recent history 5 years:

YCharts, Oakoff’s notes

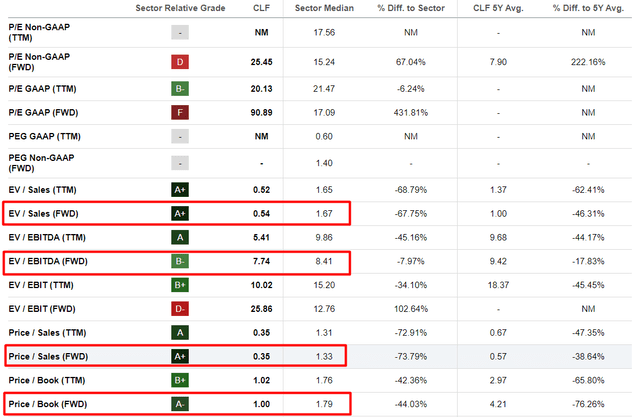

In addition, other forward-looking valuation multiples such as EV/Sales, EV/EBITDA, and P/B also point to an undervaluation compared to the industry norm of 67.75%, 8%, and 44% respectively. CLF is currently one of the cheapest steel producers in the U.S.

Seeking Alpha, Oakoff’s notes

In the table above, you may have also noticed that the 5-year average non-GAAP P/E Cliffs has is ~7.9x, which is less than FY2025 non-GAAP P/E of 11x. It appears the YCharts above may show a GAAP-based ratio, hence the difference. Personally, I don’t see a problem/overvaluation here. I believe we should consider average industry multiples, and in comparison, Cliffs remains undervalued at 11x in my opinion, even though its 5-year average FWD GAAP P/E ratio appears lower. It’s crucial to understand that these average indicators include both positive and negative metrics – this naturally lowers the averages. Cliffs has often reported negative net earnings in the past. Therefore, if we go by the industry average, I think we may call Cleveland-Cliffs cheap once its multiple aligns with analysts’ projections of 11x by the end of 2025.

If analysts are right and CLF’s GAAP EPS really is under threat, I can include a negative surprise of ~5% for EPS in my forecasts given the actual strength of the US economy (judging by recent PMI data). But even in that case, the implied P/E ratio for 2025 is 11.7x – that’s a 27% undervaluation to the average P/E ratio at which the company has traded over the past 5 years. I’ll use this calculated upside figure as the basis for my price target (the end of 2025).

Risks To My Thesis

As I mentioned in my previous articles, the steel industry, in which CLF plays an important role, is indeed very cyclical, and if you suddenly find yourself on the wrong side of the cycle, your long position can suffer greatly. So far, the CLF stock price has fallen – I hope this stops shortly, but I could be wrong. You can avoid the risk by either placing stop-loss orders or taking a longer-term position.

In addition to that, numerous analysts who have lowered their price forecasts for both steel in general and CLF stock, in particular, may be in a better position to assess the situation around, and my assessment, which differs from the consensus, could prove to be the loser this time.

Maybe the analysts really are right – this is what Argus Research (proprietary source, Argus Research’s commentary on CLF, dated 04/29/2024), whose opinion I respect and always listen to, wrote in their latest report on CLF:

We view Cleveland-Cliffs as a well-run company with a strong track record in its industry; our long-term rating is BUY. However, earnings are in a down cycle due to pricing and current valuations to earnings appear reasonable, given the company’s long-term track record against the broad market.

Your Takeaway

Despite reporting below consensus estimates and falling like a rock recently, CLF remains a great “Buy” in the medium term, in my opinion. The company showed impressive growth in adjusted EBITDA, which I think should only expand going forward amid a rebound in demand from service center buyers and cost reduction program continuation. The company has also been actively returning capital to shareholders, having completed a $1 billion share repurchase program and initiating a new $1.5 billion buyback plan. Additionally, Cliffs’ commitment to green steel production has positioned it to receive significant federal grants, further enhancing its growth prospects. My valuation calculations say that even if CLF misses the current 2025 EPS consensus by 5%, the stock will still be undervalued. I conclude that the upside potential is about 27% – this is my price objective for 2025.

I reiterate “Buy” for CLF stock again.

Good luck with your investments!

Read the full article here

")

")

")

")

")

")