")

Interested in the latest Lego set based on Jaws, but never seen the movie? Lego can help with that")

Today, we dive into an analysis of Deere & Company (NYSE:DE), an American manufacturing firm well-known for their famous green and yellow tractors and other construction and agricultural equipment. The shares seem universally loved here on Seeking Alpha (I, II, III) but the company did just announce some controversial job and production cuts in the middle of an election year. This also came after the company disclosed it was moving some of its production capacity from a facility in Iowa to Mexico in 2026. Despite some better-than-expected results from its last quarterly report, the stock of Deere is down some 10% so far in 2024.

Seeking Alpha

In addition, the annual John Deere golf tournament kicks off on Thursday. All making for an appropriate time to look at this American manufacturing mainstay. An analysis follows below.

Not surprisingly, Deere is headquartered in the middle of America’s heartland in Moline, IL. The company operates out of four separate business segments which are self-exclamatory: Production and Precision Agriculture, Small Agriculture and Turf, Construction and Forestry, and Financial Services. The stock currently trades around $360.00 a share and sports an approximate market cap of just over $99 billion. The company operates on a fiscal year that begins October 1st.

Recent Results:

May 2024 Company Presentation

The company reported its Q1 numbers on May 16th. Deere & Co. delivered GAAP earnings of $8.53 a share, more than 60 cents a share above expectations. This compares to earnings per share of $9.65 a share for the same period a year ago. Revenues did fall just over 12% on a year-over-year basis to just north of $15.2 billion. However, sales were $1.9 billion north of the consensus.

May 2024 Company Presentation May 2024 Company Presentation May 2024 Company Presentation May 2024 Company Presentation

As can be seen above, results from all the company’s business segments except for Financial Services were down significantly from the same period a year ago. Management expects net income of approximately $7 billion in FY2024, with similar net operating cash flow.

May 2024 Company Presentation

Analyst Commentary & Balance Sheet:

Despite the impressive Q2 top and bottom-line beat, the analyst community remains mixed around Deere’s current prospects. Since quarter numbers posted, seven analyst firms including J.P. Morgan, TD Cowen and Evercore ISI have maintained/assigned Hold ratings to the stock. Eight analyst firms including Barclays, Oppenheimer and Goldman Sachs have reissued Buy/Outperform ratings on the equity. Price targets proffered among these bullish analysts range from $400 to $465 million.

One corporate officer did just dispose of just over $6 million worth of equity on June 25th. Of note, this is the only insider activity in the stock since October of last year. According to the 10-Q filed for the first quarter, Deere & Co. had just over $6.6 billion in cash and marketable securities on its balance sheet. The company also listed just under $41 billion in long-term debt and $17.7 billion in short-term borrowings.

Net interest costs during the second quarter rose to $836 million from just $569 million in the same quarter the prior year.

Corporate Headwinds:

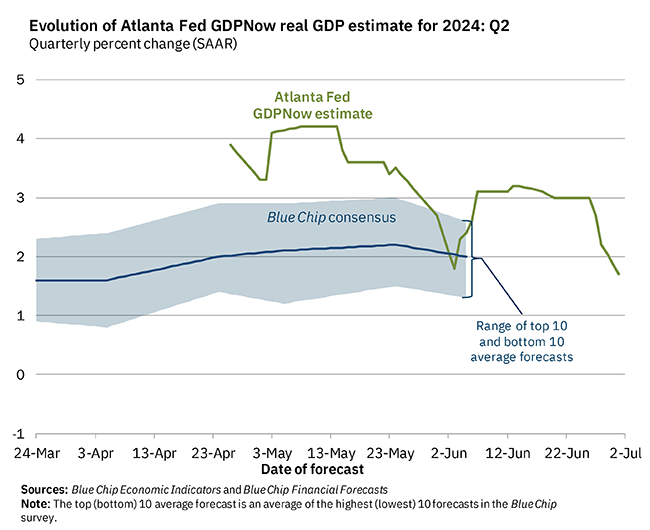

GDPNow

The company faces some significant economic headwinds right now. First, the overall economy is slowing. After recording 4.9% GDP growth in the third quarter of last year, the economy slowed to 3.4% GDP growth in the fourth quarter. In the first quarter of this year, growth slowed dramatically to 1.4%. Things are not looking much better than in the second quarter, with the Atlanta Fed’s GDPNow ratcheting down its projection for Q2 GDP growth from 3.1% to just 1.7% earlier this week.

Since the Federal Reserve started to tighten monetary policy in March 2022, interest rates have gone up substantially. This includes on corporate debt, where interest expense has gone up significantly for Deere. Construction spending for May unexpectedly declined by .1% on a month-over-month basis yesterday. The consensus was for a .3% rise. After a record year for apartment deliveries in 2023 in the U.S., large building materials company Builders FirstSource, Inc. (BLDR) is expecting a 20% to 30% drop in multifamily building starts in 2024. I highlighted this in a recent article on that company. Those shares are also down since I slapped a ‘Sell’ on them on April 1st.

Seeking Alpha

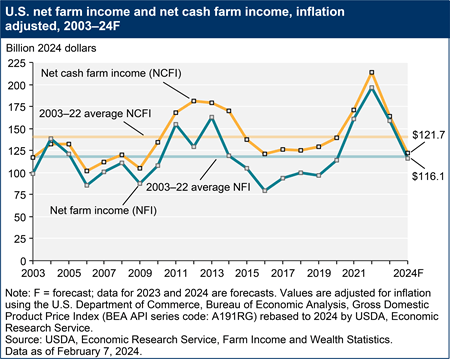

Finally, after posting all-time highs in 2022, farm income fell 16% in 2023 and is projected to continue falling at a sharp rate (25%) in 2024.

USDA

Conclusion:

Deere made $34.69 a share in FY2023 on just over $55.5 billion in revenues. The current analyst firm consensus has profits slipping to just $25.40 a share in FY2024 as revenues fall to $45.5 billion. They project a very slight decline in both earnings and revenues in FY2025.

Deere currently trades at just over 14 times forward earnings and provides an annual dividend yield of just over 1.6%. This is a significant discount to the nearly 22 times forward earnings the S&P 500 currently trades at. However, Deere operates in a cyclical industry and most always trades at a notable discount because of that.

Earnings in FY2025 are projected to be significantly below those of FY2023, and the company currently faces economic headwinds on multiple fronts. Therefore, until economic conditions improve for the segments Deere & Company primarily serves, I am passing on any investment recommendation around the stock.

Read the full article here

")

")

")

")

")

")