")

GCT Semiconductor (NYSE:GCTS) went public in March, following a SPAC merger with Concord Acquisition Corp III, from which GCT saw $50 million in gross proceeds to support the company’s growth. Recent noteworthy MoUs and market opportunities in 5G tech, makes GCTS an attractive stock that presents alpha in the semiconductor industry. GCTS began trading publicly just about six months ago, and I believe this offers investors an early entry into a potential semiconductor growth story.

GCT Semiconductor – Company Overview

GCT Semiconductor is a fabless designer and supplier of advanced 4G and 5G chip modules and IoT semiconductor solutions. GCT Semiconductor focuses on RF and baseband products that are the core of 4G and 5G connectivity. 5G, the fifth generation of wireless cellular connectivity, is pertinent to the current era of mobile technology and how we use the Internet, and it is set to usher in a wide array of transformative changes across various industries. Concepts like the deployment of AI at the edge, enhanced mobile broadband (“eMMB”), massive Internet of Things (“mIoT”), and ultra reliable low latency communication (“URLLC”) are being accelerated due to advancements in 5G technology; these concepts are the cornerstone of current technology trends. For example, Edge AI makes it possible for autonomous vehicles to process vast amounts of data from cameras, sensors, and radars on the go and in real time, making self-driving capabilities possible, while URLLC enables low latency real-time communication between these autonomous vehicles to improve safety and traffic management.

5G technology faced unwarranted backlash during the COVID-19 pandemic, as conspiracy theories falsely claimed that 5G networks were responsible for the virus’ spread. Despite these baseless and widely debunked theories, which briefly went mainstream in certain circles, 5G has proven to be a critical enabler of modern innovations, driving progress across industries rather than being the “villain” it was wrongly made out to be.

As global markets and industry-specific vertical ecosystems transition from 4G to 5G, research shows it will add over $1 trillion to global GDP by 2030, as well as massive job and GDP growth in the US in the next decade. Every market research firm projects a double digit compound annual growth rate for the 5G infrastructure and services markets in the next decade.

GCT Semiconductor has positioned itself as one of the front-runners in next-gen chip design and the imminent 5G evolution, with its portfolio of 4G LTE, IoT, and 5G products. I consider GCTS more attractive due to its fabless business model. We have witnessed impressive growth stories of fabless chip designers these past few years. NVIDIA (NVDA) is a very solid example of such a growth story as its focus on a high growth sector like AI has spurred its growth into the world’s most valuable semiconductor company as of today, and making NVDA the hottest stock of the decade. GCT Semiconductor is currently heavily focused on 5G, a similar high growth sector. Just as AI has been the main growth driver for NVDA in recent times, 5G has the potential to propel GCT Semiconductor to high levels of success, given the increasing demand for 5G technologies and IoT solutions.

GCT Semiconductor has recently secured some noteworthy MoUs and partnerships and announced vital milestones, including a recent MoU with Samsung (OTCPK:SSNLF) to accelerate the development of 4G and 5G chipsets and modules, and another noteworthy MoU inked in April this year with Saudi-owned Aramco (ARMCO) to help build the country’s 4G, 5G and AI ecosystems into futurist communications infrastructure. In late July GCT’s Luna CAT-12 LTE module cleared FCC certification and became commercially available.

A Look At GCT Semiconductors Financials

GCT Semiconductor isn’t profitable yet; and as a recently-listed R&D-intensive tech company still in its growth phase, I don’t expect much in terms of operating income for at least a few more quarters. However, I expect sales growth and operating margin expansion, which could eventually lead to profitability, as the company’s 5G products fully roll out in 2025. The 5G products will most likely be high-margin, considering the 5G products could attract premium pricing because of GCT’s patent and IP portfolio of 5G techs.

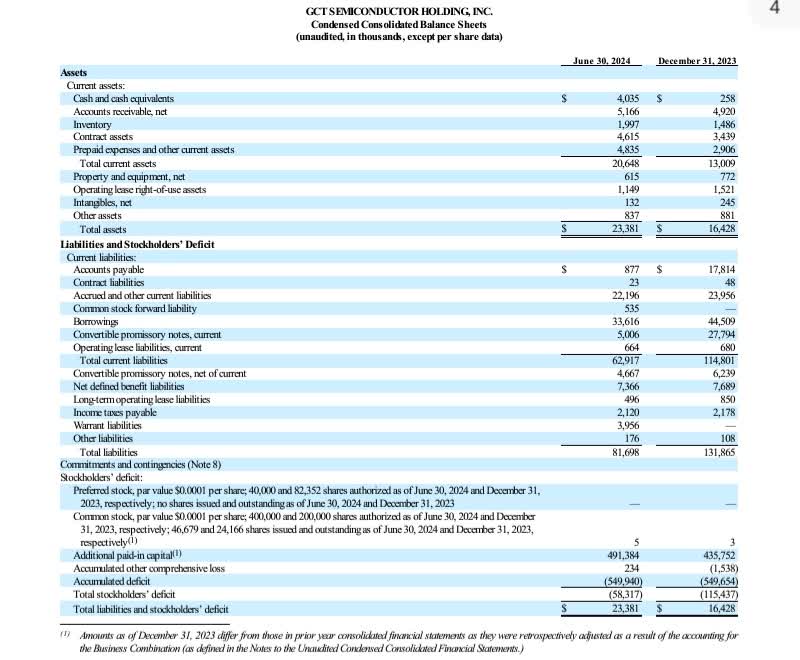

Balance sheet (GCT Semiconductor’s filing)

GCT’s balance sheet reflects negative working capital, with Quick and Current ratios around 0.3. The liquidity on the balance sheet could be well considered a red flag; however, GCT has a $50 million equity line of credit agreement with an affiliate of B. Riley Securities and that should provide a cushion for short-term liquidity challenges and help the company deleverage and recapitalize, while 5G product potentially improves sales and cash flow when they fully roll out.

Q2 cash flow reflects a $9.6 cash burn from core operations for the quarter. With current cash balance at $4 million, if GCT burns cash at the same rate, the company’s runway is critically short. Here again, the $50 million ELOC facility should provide GCT with a temporary buffer and an extended runway. GCT’s management is confident that the financing available under the ELOC agreement and other capital resources available to the company will be sufficient to keep the company running for at least the next year.

While Q2 marked an anomaly regarding 4G product sales, we expect a positive rebound of our 4G chipset sales to take place in the future. We anticipate continuous demand for both existing and new 4G products even as we focus on launching our 5G product and servicing that demand. As an example, our recently announced multi-mode 4G chipset GDM7243SL is ideal for industrial, utility and satellite applications, including for 450Mhz networks and has received a lot of attention. We expect strong demand for this product even as the market evolves toward 5G. With the additional expected initial deliveries of our 5G chipsets to commence during Q4, we are looking forward to offering high-demand, high-quality products to large and rapidly growing markets.

John Schlaefer, CEO GCT Semiconductor, during Q2 earnings call

Truly, the radio access network (“RAN”) market has declined in recent times, sinking by 9% YoY in 2023. Major stakeholders predict further woes to continue in the global RAN market till the end of this year. The 4G services market is set to decline by ~7% this year, from $585 billion to $540 billion. As 4G coverage has reached its peak in many regions, there’s reduced demand for new 4G infrastructure and devices, leaving companies with excess 4G inventory. The focus on 5G investment further slows 4G sales, exacerbating the 4G inventory issue.

Grandviewresearch.com

While forecasts reflect continued decline in the global 4G services market, a surge in demand for 5G and double-digit CAGR (as high as 50% growth rate) over the next decade are expected in the 5G services market. And here lies the top line expansion and overall turnaround potential for GCT Semiconductor. The company’s 5G portfolio is a strong catalyst.

The Company remains confident based on the progress of its 5G chipset development and reiterates the expectation to have its 5G chipsets available for broad sampling to customers during the fourth quarter of 2024, with volume shipments commencing in the first half of 2025.

Excerpt from Q2 conference call

B. Riley initiated coverage of GCT Semiconductor recently with a “buy” rating and an $8 price target in twelve months – a 190% gain from current price, citing the potential for GCT to achieve profitability and operating margin expansion in the next four to six quarters, driven by 5G sales. Though I believe that B. Riley’s target isn’t out of place, considering the immense potential the 5G products roll out have for the company, it is still worth mentioning that B. Riley was GCT’s special advisor in its SPAC merger; hence, I won’t rule out some possibility of sell-side bias in its coverage of GTCS.

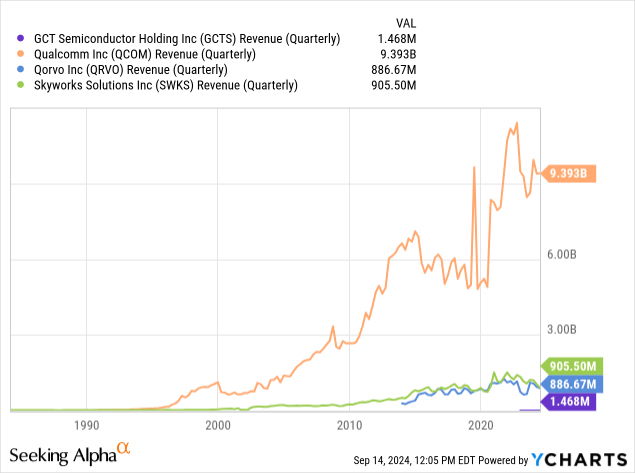

GCT Semiconductor’s sales for Q2 was $1.4 million. GTCS currently has a market cap of around $128 million at a $2.8 share price and a ~28x price-to-sale multiple. To meet B. Riley’s $8 price target, GCT Semiconductor’s sales must grow by ~820% to reach ~$13.5 million in 12 months, based on the current P/S multiple of around 28x. This growth rate isn’t far from what is feasible if GCT delivers its 5G products according to timeline, considering the revenue of peers focused on 5G.

Peer P/S comparison (Seeking Alpha)

Several fabless semiconductor peers like Qualcomm (QCOM), Qorvo (QRVO), and Skyworks Solutions (SWKS), also focused on 5G, trade at much lower sales valuation compared to GCTS. However, GCTS has a much smaller market cap and revenue; hence, its current higher P/S multiple of ~28x isn’t necessarily overvalued, in my view. This is because small-cap companies like GCT often trade at higher multiples due to their growth potential in emerging markets (5G market in this case), where there is room to expand sales rapidly. Additionally, GCT’s positioning in semiconductor niche markets, and its potential for future contracts with major clients justifies the premium multiple.

Risks

While GCT Semi’s 5G roll out presents a compelling growth opportunity, there are several risks worth noting by investors. First is the liquidity risk the company faces with only $4 million in cash and about $5.2 million in accounts receivable as immediate sources of liquidity for the company. While the $50 million ELOC provides a buffer, relying on external financing could be risky if market conditions worsen or if the company underperforms.

Talking about market conditions, supply chain disruptions in the semiconductor industry is one factor that could hamper the company’s smooth rollout, thereby creating bad market conditions for the company. The semiconductor supply chain remains vulnerable to disruptions, and this could impact GCT’s ability to launch products timely. I think initiatives by occident governments, like the U.S CHIPS and FABS Acts, are still in their early stages and are yet to have such an effect that would greatly mitigate semiconductor supply chain disruptions for now.

Takeaway

The sell-side $8 twelve-month target price for GTCS isn’t far-fetched; however, I’d like to take a wait-and-see approach to confirm sales growth in Q3, Q4, and FY24 results, considering that alpha shipments for 5G products will begin in Q4. It is also pertinent for investors to monitor how the timelines for the first 5G products roll out are met, as meeting those rollout milestones will bode well for GCT and its growth.

Read the full article here

(NASDAQ:CGBD)")

")

")

")