/cdn.vox-cdn.com/uploads/chorus_asset/file/25673333/2172439499.jpg "Boeing is cutting 10 percent of its workforce")

")

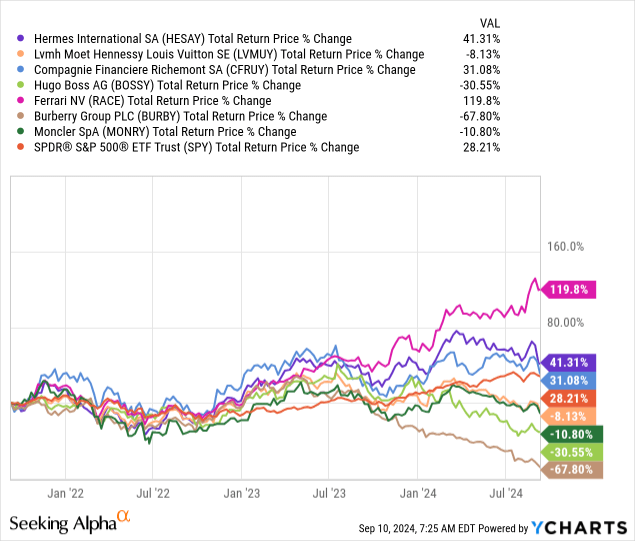

One of the most surprising recent developments in the market has been how quickly luxury stocks went out of favor. Bloomberg is calling the $240 billion rout “just the beginning”, UK’s luxury powerhouse Burberry (OTCPK:BURBY) is being removed from the FTSE 100 (UKX), and some Swiss luxury watchmakers are asking their government for help.

This is leading many investors to question whether the luxury sector is less insulated from economic weakness than previously thought, with many previously believing it was an almost “recession-proof” sector. Even French luxury powerhouse Louis Vuitton (OTCPK:LVMUY) and Italian fashion icon Moncler (OTCPK:MONRY) have recently experienced some weakness.

It appears that brands that have a significant share of affluent customers are experiencing more issues, while those targeting exclusively the ultra-wealthy still performing well. Two examples are Hermès (OTCPK:HESAY), with their insanely expensive Birkin bags, and super-car maker Ferrari (RACE), which cater to the 1% of the 1%. The problem with investing in these two companies is that their valuations already largely reflect the power of their brands. We are more interested in looking at companies that might be experiencing some issues, but where the market’s negativity might have gone too far. We think that might be the case with Hugo Boss (OTCPK:BOSSY), which is now trading at a fraction of its sales, despite being one of the most valuable German fashion brands and having operations in 131 countries around the world.

Q2 Financial Results

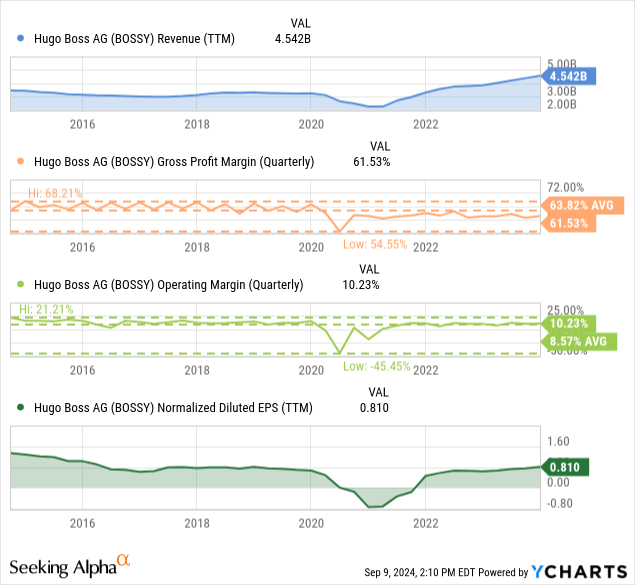

Hugo Boss reported relatively weak results for the second quarter of financial 2024, although better compared to its peer average. The company delivered a -1% revenue growth compared to the previous year’s quarter, while its peers averaged -4%.

Some of its peers include companies like Burberry, Capri Holdings (CPRI), Moncler, and Ralph Lauren (RL) among others. This means the company gained some market share, but at the expense of profitability, as the company increased operating expenses including marketing, resulting in a 42% year-over-year decline in EBIT. The company is taking several cost measures to help restore a good level of profitability going forward.

Hugo Boss Investor Presentation

Brand Strength

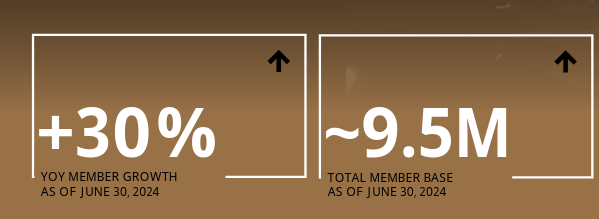

Some signs of brand strength can be seen with the company’s pricing power, reflected in high gross profit margins of close to 62%, for comparison, The Gap (GAP) has gross profit margins about 20% lower. There is also anecdotal evidence of the brand strength, which includes achieving a multi-year collaboration with David Beckham, or the Queen Letizia of Spain seen wearing Hugo Boss clothing. Another sign pointing to brand strength is the number of customers becoming loyalty members, which is approaching 10 million.

Hugo Boss Investor Presentation

For better or worse, most of the company’s sales continue to come from the BOSS menswear line, at roughly 70%. On the positive side, many customers see the purchase of this type of clothes as an investment in their careers. The downside is that the work-from-home trend is reducing the need to buy formal clothes. The company is adapting by expanding its offerings to include more casual options and even sports clothing.

Hugo Boss Investor Presentation

BOSS womenswear currently represents only about 10% of sales, but it is growing faster than menswear. It is also affected by the work-from-home trend, but here the company is expanding toward more casual and sporting offerings too.

Hugo Boss Investor Presentation

Finally, the HUGO brand represents about 20% of sales and is growing faster than both BOSS menswear and BOSS womenswear.

Hugo Boss Investor Presentation

Hugo Boss also earns a small amount of high-margin revenue from licensing the brand for things like fragrances, sunglasses, and accessories. Given the price of the clothes, it is not surprising that many customers want to try them before buying, which has meant that brick-and-mortar sales continue to represent the majority of sales, but the digital channels are not doing too bad as they represent about 20% of revenue.

Hugo Boss Investor Presentation

Financials

While sales continue to significantly exceed pre-pandemic levels, gross profit and operating margins are below their ten-year averages.

Future revenue growth is mostly expected to come from selling more to women, expanding the casualwear category, and growing the Asia Pacific region. Cost initiatives will also be key to restore profitability, as earnings per share (EPS) are lower than they were ten years ago as a result of the decline in profit margins.

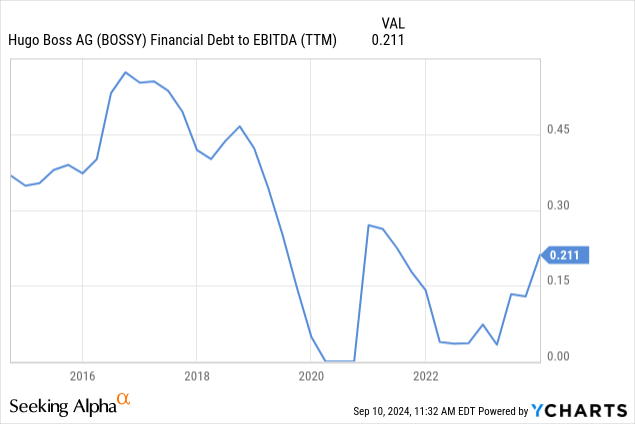

Hugo Boss has a solid balance sheet with relatively low leverage, which has resulted in the company having an investment grade credit rating. S&P Global (SPGI) has rated Hugo Boss ‘BBB’, but with a negative outlook.

Sustainability

Hugo Boss is differentiating itself also by its sustainability efforts, which customers are increasingly taking into consideration when buying clothes. The company is listed in the Dow Jones Sustainability Index and has a ‘B’ grade from non-profit CDP in relation to its efforts to mitigate its climate change impact. The company is targeting 0% polyester & nylon use and a 50% reduction to its CO2 emissions by 2030.

Hugo Boss Investor Presentation

Outlook

Despite the relatively difficult economic environment, Hugo Boss is still guiding for modest revenue growth in the range of 1% to 4% for the full-year.

The company also expects that cost measures taken during the first half of the year to support better profitability going forward, including reducing production costs and sourcing efficiencies. Still, its EBIT guidance remains quite wide, with the company expecting to deliver EBIT in the range of €350 million to €430 million. Compared to the €410 million delivered last year, this would imply growth between -15% and +5%, while free cash flow is expected to be around €500 million.

Hugo Boss Investor Presentation

Valuation

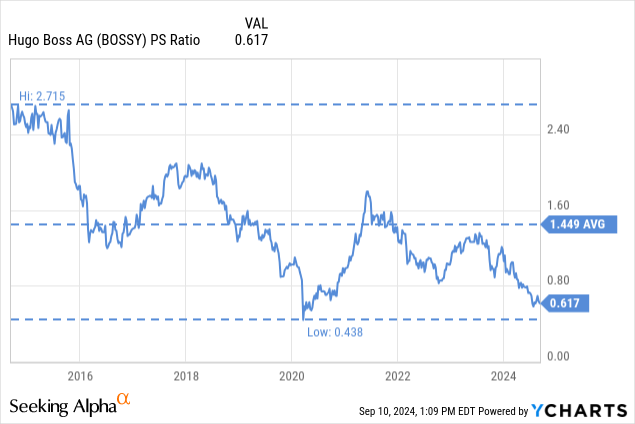

A big reason why it’s worth taking a look at Hugo Boss right now is that the valuation is looking quite attractive. With a market cap of approximately €2.5 billion and expected free cash flow of roughly €500 million this year, shares are currently trading at only ~5x expected FCF. Looking at other valuation metrics, it also becomes clear that Hugo Boss has rarely traded at such low valuation multiples. For example, it is currently trading at less than half of its ten-year average price/sales multiple.

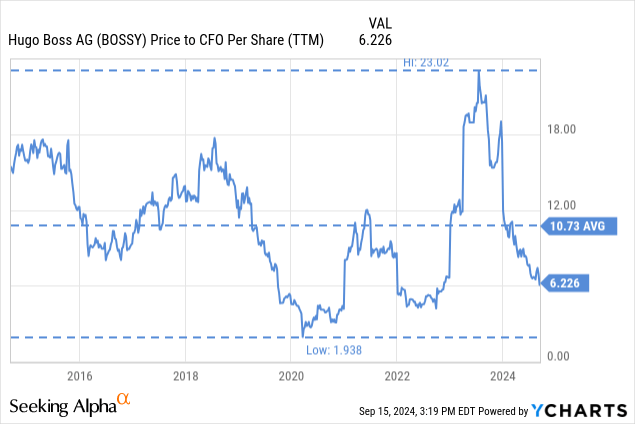

Shares are also trading at a significant discount to their ten-year price to cash flow from operations multiple. The dividend yield is also looking attractive at 3.7%.

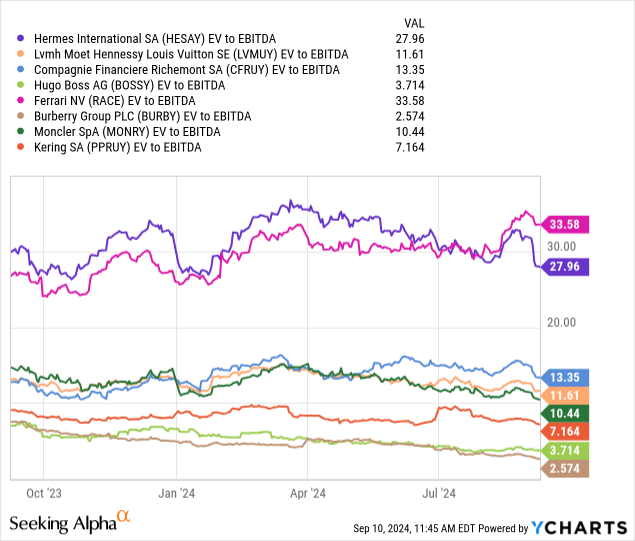

While we agree that Ferrari and Hermès have stronger brands, they are commanding an EV/EBITDA multiple almost an order of magnitude higher. Compared to most luxury powerhouses, Hugo Boss looks very attractive, only Burberry shows a lower EV/EBITDA. Still, with Burberry posting double-digit comparable sales declines and scrapping its dividend, we find Hugo Boss a better option.

Risks

In general, we consider the apparel sector relatively risky, with fashion trends constantly evolving and fierce competition. Still, some brands do have real pricing power, especially in the luxury segment. As this pricing power usually results in more attractive profit margins and returns on investments, the companies that own these brands tend to trade at an elevated premium.

While we believe Hugo Boss is a relatively strong brand, it is nonetheless being negatively affected by a weaker consumer, especially in the UK and China. Another important risk for the company is the work-from-home trend, which tends to reduce the need for more formal clothing. It is therefore possible that conditions could get worse for the company before they get better. Still, these risks are mitigated by the fact that the company is still generating significant amounts of free cash flow, and the very undemanding valuation.

Conclusion

Consumer weakness is starting to have a negative impact even on some luxury brands. It appears the only ones currently avoiding the headwinds are the most exclusive ones catering to the ultra-wealthy, such as Ferrari and Hermès. Still, brands like Hugo Boss have demonstrated to have decent pricing power and brand strength. Currently trading at approximately five times expected free cash flow for the year and at less than half their ten-year average price/sale multiple, we think Hugo Boss shares are worth considering. The apparel sector is one we do not particularly like, and Hugo Boss has many risks that should be taken into consideration, including the work-from-home trend. However, the current valuation is low enough to make the shares worth considering.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here

")

")

")

")