Booze souffle")

Thesis

iShares Russell 2000 ETF (NYSEARCA:IWM) offers an effective way to gain exposure to U.S. small-caps at a time where small-caps appear to be primed for outperformance relative to large-caps.

ETF Overview

IWM is an exchange-traded fund that provides exposure to 2,000 underlying U.S. public small-cap companies. The ETF is passive, attempting to replicate the results of the Russell 2000 Index. The Russell 2000 is market-cap-weighted like the S&P 500 Index.

Price Versus Performance

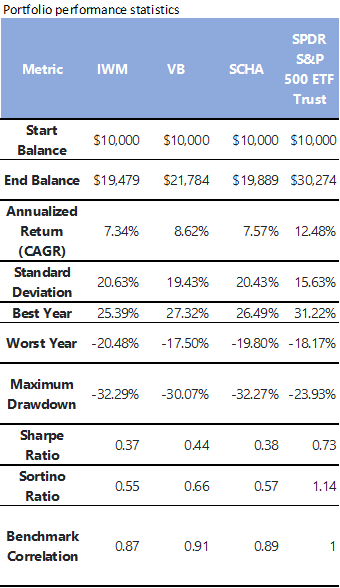

While it is passive, IWM’s expense ratio is higher than peers at 0.19% (for instance, Vanguard Small-Cap ETF (VB) has an expense ratio of 0.05% and Schwab U.S. Small-Cap ETF (SCHA) has an expense ratio of 0.04%). Those two ETFs follow different indices, which, due to licensing, might explain some of the discrepancy in expenses. While it may not seem like a big deal initially as all three are providing passive exposure to the same thing, U.S. small-cap stocks, the reality is that the performance results (since January 1, 2015) have been very different, with VB leading in terms of absolute (by almost 1.30% annualized) and risk-adjusted performance. I included the SPDR S&P 500 ETF Trust (SPY) for reference (acting as the benchmark).

Jan 2015 – May 2024 (Portfolio Visualizer)

The market return for the ETF may diverge from the Russell 2000 Index, primarily due to the expense ratio, but it’s historically been within 20 basis points annualized. As of June 24, 2024, IWM traded at a 0.02% discount to NAV. IWM is very liquid with a 30-day median bid-ask spread of 0.00%, which compares favorably to 0.02% for SCHA.

Future Results

Overall, it’s hard to say which ETF will outperform in the future; however, based on past results, VB looks to provide the better risk-adjusted returns with the lowest drawdown and greatest absolute return of the three passive U.S. small-cap ETFs mentioned. That said, I wouldn’t immediately rule out IWM. IWM is highly liquid, providing flexibility and optionality. The Russell 2000 Index is the index that many fund managers benchmark themselves against. It is somewhat of the gold standard of small-cap indices, so the added expense may be worth it for some.

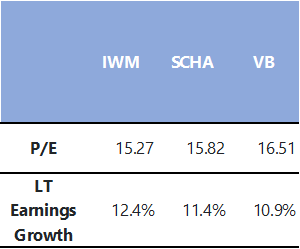

Looking at Morningstar data, VB has the highest P/E multiple while delivering the lowest long-term earnings growth. IWM actually provides the lowest P/E multiple and the highest long-term earnings growth. This suggests to me that IWM may outperform SCHA and VB in the future.

Morningstar

Why Small-Caps

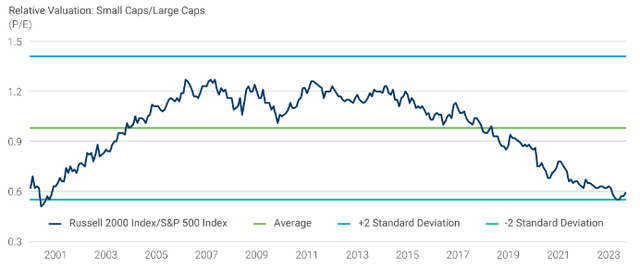

With the Fed increasingly considering reducing interest rates, small-caps are an excellent allocation for several reasons. First off, small-caps are more exposed to the economy and should disproportionately benefit from any economic stimulus versus their large-cap peers. Second, small-cap stocks are trading at a huge discount to their large-cap peers. The chart below is through September 2023 (the discount is even larger now given the massive spread in performance between small-caps and large-caps YTD).

Based on data from January 2000 through September 2023. For illustrative purposes only. (Lazard)

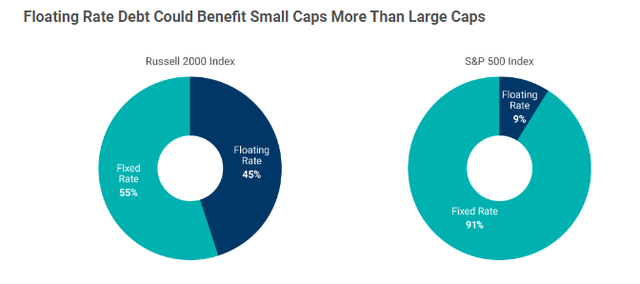

Third, small-cap stocks are much more leveraged than their large-cap peers (3.2x net debt-to-EBITDA versus 1.6x for the S&P 500, per Lazard) and almost half of their outstanding debt is floating rate debt, so if interest rates go down, small-cap interest payments go down significantly relative to large-caps.

As of 30 September 2023. (Lazard)

Conclusion

There are now over 3,200 ETFs, which provide a wide assortment of investment options. It is difficult to determine which ones will succeed and which ones will wither away; however, passive ones based on widely followed and well-regarded indices are likely to stick around. Given the drastic undervaluation of small-caps relative to large-caps and the probability of rate cuts in the future, it would be wise to look at possibly adding some small-cap exposure. Doing so passively provides great options, like VB, SCHA, and IWM. IWM provides exposure to the most widely-followed small-cap index, providing a level of comfort and familiarity that VB and SCHA don’t provide. IWM also provides the lowest P/E and highest earnings growth, suggesting a possibility of outperforming its peers. At the same time, VB has provided superior absolute and risk-adjusted returns since 2015. I would carefully consider all options before investing.

Read the full article here

")

")

")

")