")

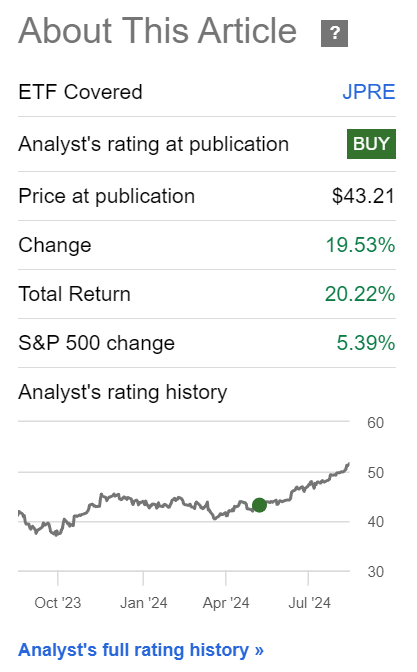

A few months ago, I recommended the JPMorgan Realty Income Fund (NYSEARCA:JPRE), an actively managed real estate investment trust (“REIT”) fund managed by JPMorgan Asset Management. So far, JPRE has performed well, returning over 20% in the past few months and far outpacing the S&P 500 Index (Figure 1).

Figure 1 – JPRE has performed well (Seeking Alpha)

What was the driver for JPRE’s rally, and is it likely to continue?

Expectations for Federal Reserve rate cuts have boosted the valuation of long-duration real estate assets. JPRE’s manager deftly repositioned the fund towards capturing upside returns by adding to economically sensitive sectors like Office and Industrial REITs and reducing defensive exposures.

Looking forward, I continue to recommend JPRE as a relative buy for real estate exposure. With a weakening economy being the primary cause of the Fed’s pivot on interest rates, I believe we may need to reposition defensively in the coming quarters, and I trust JPRE’s experienced managers will do the right thing.

Brief Fund Overview

The JPMorgan Realty Income ETF is an actively managed fund that primarily invests in stocks of REITs across the market cap spectrum. The JPRE ETF has a long history and was formerly known as the JPMorgan Realty Income Fund (a mutual fund), but was converted into an ETF in May 2022. The JPRE ETF has almost $380 million in AUM and charges a 0.50% net expense ratio (Figure 2).

Figure 2 – JPRE overview (JPRE factsheet)

Imminent Rate Cuts Boost Real Estate

The main driver behind the surge in real estate-related stocks and REITs has been the imminent beginning of a Fed rate-cutting cycle. Currently, there is a 50/50 chance of a 50 bps rate cut at next week’s September FOMC meeting, and investors have priced in 125 bps of rate cuts into year-end (Figure 3).

Figure 3 – Investors have priced in 125 bps of rate cuts into year-end (CME)

Since the July FOMC meeting, when the Federal Reserve Chairman opened the door to a September rate cut, interest rates have been declining rapidly in anticipation of the beginning of the Fed’s rate cuts. The 10-year treasury yield recently declined to 3.6%, the lowest level since early 2023 (Figure 4).

Figure 4 – Anticipation of Fed rate cuts have caused long-term treasury yields to plummet (stockcharts.com)

Real estate and REITs, being long-duration assets, saw a re-rating in their valuations and the JPRE ETF surged higher (Figure 5).

Figure 5 – Lower long-term interest rates have driven JPRE higher (Author created with price chart from stockcharts.com)

JPRE Has Gone On The Offensive

Looking at JPRE’s holdings, we see the fund manager has been quite active in recent months, with JPRE’s sector allocation shifting dramatically since April. Allocation to Office REITs has gone from 4.5% of the portfolio to 30.4%, Apartment has increased from 15.7% to 23.2%, and Industrial has increased from 10.4% to 19.8% (Figure 6)

Figure 6 – JPRE sector allocation has shifted dramatically since April (am.jpmorgan.com)

Allocation to defensive Health Care REITS has decreased from 15.6% to 5.8% and Diversified REITs have declined from 32.9% to 4.1%.

Overall, this suggests the JPRE has gone on the ‘offensive’, taking advantage of the boost in valuations from lower interest rates to buy ‘cheap’ office and apartment REITs.

This has allowed the JPRE ETF to keep pace with passive REIT funds like the iShares U.S. Real Estate ETF (IYR) in the past few months during the valuation re-rating (Figure 7).

Figure 7 – JPRE has kept pace with passive funds during re-rating (Seeking Alpha)

JPRE’s ability to quickly switch from defense to offense and vice versa has allowed the fund to outperform the passive IYR ETF, with a 31% total return since May 2022 compared to IYR’s 28.7% (Figure 8).

Figure 8 – JPRE has outperformed since relaunching as ETF (Seeking Alpha)

In fact, if we stretch JPRE’s performance history back further, since the original mutual fund’s inception in January 1998, the JPRE ETF and its predecessor mutual fund have delivered total returns of 820% to July 31, 2024 (Figure 9).

Figure 9 – JPRE has a long history of creating value (JPRE factsheet)

This compares favorably to the FTSE Nareit All Equity REITs Total Return Index, which only returned 730% in total returns over the same time frame from January 1998 to July 2024 (Figure 10).

Figure 10 – FTSE Nareit All Equity REITs Total Return Index (Author created with data from NAREIT)

Rising Tide Lifts All Boats But Stick With The Experienced Hand

Looking forward, although a rising tide has lifted all boats with most real estate funds and REITs rallying in the past few months, I continue to recommend investors stick with the JPRE ETF, as the fund manager’s deep expertise and willingness to play defense will likely prove useful in the coming quarters as the economy slows.

For example, the U.S. unemployment rate recently triggered the Sahm Rule, which says that when the three-month moving average of the unemployment rate rises by half a percentage point from the cycle low, the economy may already be in a recession (Figure 11).

Figure 11 – Triggering of the Sahm Rule suggest U.S. economy may be weakening (St. Louis Fed)

If the U.S. economy continues to weaken, I expect recent winning sectors like Office and Industrial REITs may underperform, as they are more economically sensitive compared to defensive REIT sectors like Health Care. In this scenario, I believe JPRE will rotate out of offense and back into defense.

Conclusion

The JPMorgan Realty Income ETF has performed well in the recent months as the real estate asset class has been buoyed by expectations of interest rate cuts by the Fed. JPRE’s sector allocation was able to quickly switch from playing defense to offense, demonstrating the manager’s ability to add alpha.

Looking forward, I continue to recommend the JPRE as a buy for real estate exposure, as a weakening economy may require the manager to play defense once again in the coming quarters.

Read the full article here

")

")

")