")

Brendan Fraser yeets Peter Dinklage across a bathroom before water boarding him while demanding some emeralds. Then it gets weird")

Co-authored by Treading Softly.

I was recently touched and extremely disheartened reading the story about Denise Prudhomme. Perhaps you have not heard her story. She was an employee at Wells Fargo (WFC) who clocked in for work and was found dead four days later. No one had noticed that she had passed away for days on end until a colleague found her dead body. According to the police at this time, they believed that she had been dead for many days.

Well, I am a big believer in putting 100 percent effort into anything you do, whether that be work or play, research or writing, or just about anything. I also understand that there are limits to what you get back from what you put in.

According to the Bureau of Labor Statistics, 5486 individuals died at work in 2022. Meanwhile, the American Institute of Stress claims that 120,000 individuals die of work-related stress every year.

Work and stress can both cause fatalities; it’s statistically true. While the chances are smaller than other causes of fatalities, if you take the American Institute of Stress’s claim at face value, it would make it the 5th leading cause of death in the United States.

So today, I want to focus on something that doesn’t take from you, robs you of life force or energy, or even potentially claims your life altogether. Let’s move away from looking at stress and work and focus instead on something that can provide for you, your family, and your descendants over the long run. I love investing my energy and my focus on things that provide returns.

This is why I created my unique Income Method. It’s a philosophy on financial management, a perspective on life, but most importantly, key guiding rules for how to manage an investment portfolio. You see, unlike work, in which you must trade your health for wealth in the form of a paycheck, stress can rob you of energy and life in different situations that may or may not financially reward you. Approaching the market from an income investing philosophy can reduce stress and improve your financial situation.

Let’s dive in!

Dividends are Irrevocable Returns

You don’t have to be a market participant for very long to know the phrase “past returns do not guarantee future results.” That phrase is quoted at the beginning of every earnings call, or anytime that you’re discussing an investment. It applies anytime you point to a chart and look at the past 10 years and claim that that’s going to continue on into the future.

It’s just a simple truth.

The past does not govern or determine the future events that could be coming down the pipes that have never been seen or approached before by that specific company. They could radically alter the trajectory or the health of the company. This is one reason why I recently discussed with my investment group, High Dividend Opportunities, that you shouldn’t take comfort in unrealized capital gains. You see, something unrealized can disappear. I can promise you that I will give you $1,000,000, but if I pass away before ever fulfilling that promise, your unrealized gain of $1,000,000 can vaporize – unless you had some form of writing to be able to prove it. Likewise, the unrealized capital gains you see in a number of the stocks in your portfolio, and that’s all they reward you with, are a vapor on the wind. They’re here today and can be gone tomorrow. One bear market, one bankruptcy filing, or one bad choice by management, and those returns that are unrealized can vaporize.

On the contrary, a dividend is a cash payment given to you by the company. It’s a form of return that, once received, can never be taken back. This is one reason why dividends are what I like to call an irrevocable return. A return that once you have it, you can do whatever you want with it. That stock has still provided you that return regardless of the future. It’s a down payment today for opportunities tomorrow. Whether you reinvest that back into the company to show continued faith in it or you take it and spend it on a meal with your loved one, that dividend is a return part of the total return equation. It can never be reduced back down. It’s one reason why I love high-yield dividends because if I can get 10% back from my return every year, in a decade I have 100% of my capital back, and the investment continues to churn more thereafter.

This is unlike a workplace, where you have now given something of yourself to get something back. It is also unlike investing in growth, where you’re hoping that the value will rise so that someone else will give you more than you gave to get it. One reason that gold continues to rise in value is its scarcity, but also because there’s continued demand for it. Gold itself doesn’t accumulate value. It’s the continued rise in demand for gold that increases its value over time, as well as the devaluation of fiat currencies like the U.S. dollar. Gold becomes more valuable against the dollar because they keep printing more dollars, but they’re not finding new gold at nearly the same rate. If a massive stockpile of gold was to be discovered, the value of gold versus the dollar would plummet if that gold flooded the market and drained away the demand.

My dividend, once received, is mine forever. I may spend it frivolously, or I may spend it prudently. However, it is still mine, and the total return equation, from the point you buy to the point you sell, is the change in the value of your investment plus any dividends received. That “plus any dividends received” section continues to grow with each dividend that I receive and will not be subtracted from. This is one way that dividends can provide for you financially; they provide you an irrevocable return that you can then choose to use however you choose to use it.

I believe that people are often the best determiners of how they spend their money, not a third party like a corporate management team or a government entity.

Dividends Can and Often Will Outlive You

If we think about seeking things that will provide for us instead of taking from us; those that won’t take our time, energy, and life, but will instead provide for us to reduce the amount of energy, time, and life we have to give out to other tasks, dividends are a wonderful provider. Not only because they can provide for you in this lifetime, but also because quality income from quality sources can out-provide your lifespan. They can provide you with financial security up to the point where you pass away, and they can continue to provide for your loved ones or future generations.

There has been a fundamental shift within the American perspective as far as generating wealth goes. We’ve moved away from trying to generate wealth that will be passed on from generation to generation, enabling our next of kin to have more success than we had. We’ve turned into a perspective where it’s my money, and I earned it, so I want to spend it all before I pass away. This is a risky gamble because if you mistime when you’re going to pass away, you may end up with nothing at the end. I advocate for a long-term perspective, generating the wealth that I can enjoy today but also providing financial well-being for future generations.

I’m not looking to make my entire family tree unbelievably wealthy. Instead, I am looking to help them by greasing the gears of success without having to necessarily give up as much life as I had to find my success. I’m not looking to create entitlement, but I’m looking to give enablement towards success through their hard work without financial constraints always being at their heels.

If we look at the history of stalwart dividend payers and funds, we can see that they can readily continue to pay beyond your natural lifespan, providing for your heirs and their heirs. The beautiful thing about my Income Method is that it’s not focused just on you. It’s focused on you, your next generation, the next generation, and so forth because the principles are timeless, even if the investments that are being held are finite and have set maturities. Consider some of these beautiful examples of long-term dividend payers and how they could pay you, your children, your grandchildren, and so on:

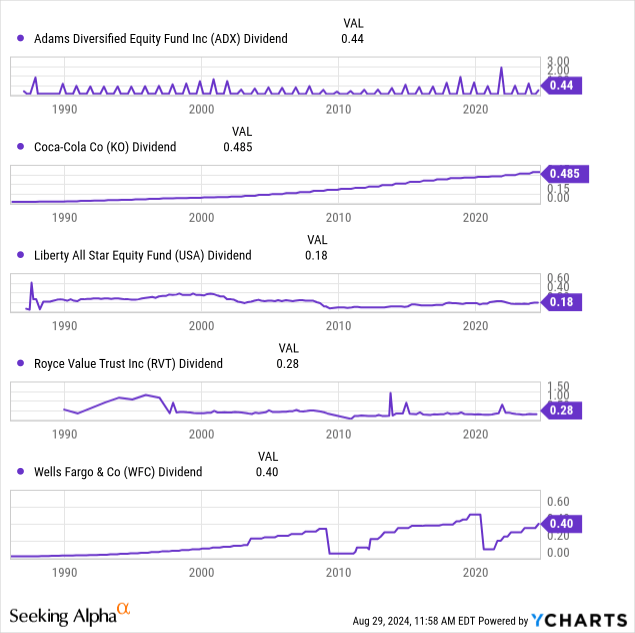

WFC is a very well-known major financial institution within the U.S., well-known for various banking issues, from allegedly opening accounts for customers without their knowledge to having its assets capped by regulators due to compliance issues. We also remember the employee mentioned above died, and no one noticed for days.

Royce Small-Cap Trust (RVT) is a CEF (Closed-End Fund) that invests in small-cap value stocks and pays a quarterly variable distribution based on its trailing Net Asset Value (NAV). Born in 1986, the fund has seen several bull and bear markets and has delivered market-beating returns to patient shareholders. Today, RVT offers a 7.6% yield to benefit from allocations to a discounted asset class in a slowing economy with frothy equity valuations.

Liberty All-Star Equity Fund (USA) is a CEF that invests in a mixture of growth and value investments. USA is unique in that its portfolio is managed by multiple sub-advisors who each invest using unique methods. Since its inception in 1986, USA has outperformed the market while paying a variable distribution each quarter based on the funds’ trailing NAV. Currently, USA pays a 10.5% yield, a level above its 10-year average.

Adams Diversified Equity Fund (ADX) is one of the oldest CEFs existing. It historically paid small quarterly distributions and a massive year-end payout in December. Recently, however, ADX has switched its distribution practice to be more in line with the USA and RVT funds. The 95-year-old CEF currently yields 8.5%.

The Coca-Cola Company (KO) is a massive multinational company focused on various soft drinks. KO is an excellent example of a company that manages growth effectively while continuously rewarding shareholders with 60+ years of continuously growing dividends.

All of the above investments have three to four decades of dividend-paying history.

The market is pouring out income to those who are willing to collect it, and it will continue to do so beyond your lifespan. Dividends can provide for you in ways that so many other avenues to generate wealth cannot.

Conclusion

Today, we’ve taken a moment to recognize that your workplace and the stress in your life are both trying to kill you. While your workplace may claim that it cares, it could also be the place where you pass away and no one finds you for days. Instead of giving our lives away to our employer, we should be trying to pour our energy and focus into something that will provide for us, even if we’re not continuing to work for it. Building an income-generating portfolio can provide you with the income you so desperately need in retirement. Whether it is retiring at retirement age or choosing to retire early, having a passive income stream is a massive benefit and, often, essential.

Take action today. Don’t hesitate to build a portfolio that will provide you with essential income, so you don’t need to give up your health for a paycheck. The ideas listed above are a great jumping-off point to achieving a paycheck-replacing income stream.

When it comes to your retirement, I want it to be marked by the word abundance—an abundance of income that overwhelms your expenses, an abundance of opportunities that you can explore because you’re not financially constrained, an abundance of memories to think back on and share that was made possible by living in true financial freedom without financial constraints.

That’s the beauty of my Income Method. That’s the beauty of income investing.

Read the full article here

Q3 2024 Earnings Call Transcript")

")

")

")