")

When I was a youngster hedge funds actually hedged things. If the fund operator owned a portfolio with high risk but the possibility of producing spectacular returns, the decision to hedge your bet was undertaken to reduce risk while holding on to the bulk of the large gains. This was often done by trying to buy the best firm in an industry while selling short the worst, often by buying put options. Sometimes this took the approach of buying or selling options on an entire industry likely to offset risks in a major bet on a single stock. It was like buying insurance against potential ruin if the major bet does poorly. That was yesterday. Most modern hedge funds are mainly out to ramp up profits by doing things like borrowing in a currency with low interest rates while focusing on a handful of favorite stocks. Warren Buffett actually did exactly the same sort of carry trade by borrowing in yen at .5% interest to pay for a large position in five huge Japanese trading companies. So far this has worked out brilliantly for Berkshire Hathaway (BRK.A)(BRK.B) as Buffett has trounced other investors in Japan who did not hedge against exposure to the yen.

What I want to discuss in this piece is pretty much plain vanilla hedging of risk in your portfolio and mine. Hedging to reduce or limit risks is not something I recommend doing on a regular basis but there are occasions when it may be important to limit risks. There’s a possibility that we are currently in one of those periods. This came to my attention while writing my previous article on India after its recent election. Two numbers jumped out at me as I did a quick check in order to confirm my assumption that the valuation of Indian stocks, though high for an emerging market, were in line with US valuations. The surprise was the U.S. valuations I discovered after a brief search. The S&P 500 Index ETF (SPY) now sells at 27.5 times earnings while the Nasdaq 100 ETF (QQQ) sells at a 34 P/E. That’s quite expensive by any measure and implies a duration of three decades unless there is a severe correction fairly soon. It’s probably time to give some thought to the potential correction and ways to deal with it.

Ask Yourself: What’s The Worst Thing That Can Happen?

Most market corrections don’t really require an effort to hedge. The market drops about 10% once almost every year. Corrections on that scale usually end within a month or two after which the market continues its upward march. There’s no point in trying to hedge. The only trouble is that A 20% correction always begins as a 10% correction and it doesn’t announce how long it will go on and how far it will ultimately drop. The next level – a 20% correction- comes fairly frequently, roughly every two or three years. It’s up to you to figure out how far the correction will go, and if you are like me, you are prone to make mistakes when you try to guess.

Most 20% corrections are brief, maybe a little longer than recoveries from 10% drops, but nothing deeply concerning. In the 2016 correction which stopped a tick or two short of 20% I was a buyer rather than a hedger, picking up a significant position in United Technologies which has now by merger become the larger part of RTX (RTX), a position I continue to be happy with. I bought more heavily in the one-month COVID crash of March 2020 which briefly exceeded 30%, taking advantage of the fact that a half dozen stocks I had always wanted to buy at the right price had suddenly become cheap. No regrets. If you’re pretty sure that a correction will stop at 20%, it’s probably better to buy than hedge.

The important question to ask yourself is pretty simple: What’s the worst thing that can happen? I think the best answer is a decline likely to take your portfolio down 40%-50% and keep it down for a while. Declines like this are uncommon and irregular, maybe every decade or two on the average. Over the six decades I have been in the markets there have been three that fit. The first was the inflationary crash of 1974 which took place when I was 30 and didn’t watch the markets as intensely as I do now. The 1970s were generally awful in the markets despite the fact that nominal economic growth was fine. Super high inflation made the 50% plus decline much worse than the nominal amount. A good hedge would have been owning commodities, especially oil and gas, as well as oil stocks, which performed brilliantly. I did own a couple of oil stocks.

What follows is a rule on crashes and major negative market events: They’re much more likely to persist and make it worth thinking about hedging if the market event is accompanied by something badly wrong with the economy. The opposite was the case with the 1987 Crash which looked like 1929 on the charts as the market began to roll over in September and finally crashed 40% in one day. It was actually a buying opportunity as the market was back to the highs within a few months with no harm to the economy. It helped to have a tennis friend who was CEO of a manufacturing company and told me not to worry, his business had a year and a half backlog. The insight: Pay attention to indicators from people you know well.

The other two events were 2000, when badly informed market newbies completely lost their minds over extremely overpriced dot.com stocks, and the 2008-2009 collapse caused by silly speculative house buying and banks which recklessly supported it with mortgages which became worthless, dragging major banks down with them. Remember the immortal words of legendary Chuck Prince, CEO of Citigroup (C), “As long as the music is playing, you have to get up and dance.”

The 2000 crash was mostly in tech stocks and a few blue chips. It lasted for three years, although the economic damage was limited to a mild recession quite a few of the dot.coms went bankrupt. Its major long-term affect was that tech stocks did not regain popularity until around 2014. My hedge consisted of owning a combination of value stocks and Treasury Bonds which then paid a nice 6%.

Many readers older than 40 will recall that in 2008-2009 a lot of banks actually went under, putting the entire financial system at risk causing President Bush to fear that “this sucker is going down.” It didn’t, but nobody knows how close it came. My hedge? Holding quite a bit of cash and Berkshire Hathaway (BRK.A) (BRK.B) which was certain to survive and would profit by picking up the pieces. On the other hand, I owned a position in Wells Fargo (WFC), thinking it was the best of the banks only to watch news come out over the next eight years or so as it turned out that their claim to be solid, well-managed, and brilliant at cross-selling was met by developments that challenged that view. Buffett himself was bagged by it and conservative funds like Dodge and Cox (DODGX) which had done well with financials in the past had several challenging years.

It may be that avoiding a large commitment to one group (such as financials) was, and is, the best way to survive a market collapse accompanied by huge risk to the economy. One amusing anecdote. One day in 2008 I glanced at the ticker and saw that Citigroup looked cheap around $50 and bought 1,000 shares just before the close. Ten minutes later I realized I didn’t feel good about this, did a little research, and got up early the next morning and sold the 1,000 shares at $49. That $1,000 loss was one of my best decisions ever on a stock which was soon selling under $5 and eventually prepared a reverse split.

What Does Hedging Cost? What Are The Alternatives?

The traditional way to hedge a stock position is to use put and call options. For the purpose of hedging you buy a put option or sell a call option or do a combination of the two, a strategy which is called a “collar” because it places the stock in a protected area above and below its present price. The purchase of a put option establishes a floor below which the value of your stock won’t go down because you can deliver it to the seller of the put at that price. The sale of a call option returns cash which adds income if the stock goes up or remains at its current price while reducing the amount you lose if the stock goes down.

The protection provided by a put is absolute in limiting what you can lose, but there’s a catch. All options are wasting assets, which means that their value diminishes as time passes before eventually going to zero. I will spare you the rather interesting math which describes the declining value but it’s one of the things you learn to pass the actuarial exam. The practical thing to remember that if the stock goes up or stays where it is you just lose the money you spend to buy the put. When you sell a call the fact that calls are also wasting assets is the problem of the buyer. If the price of the stock goes up by more than the premium received for the call, you will have sacrificed the amount by which the price increase exceeds the amount paid for the call.

In both cases time is very important. I have never had much enthusiasm for buying puts because the market is very good at pricing them and they tend to expire worthless more than half the time. Calls are different in that you are happy to pocket the premium if they expire worthless. There is a catch, however. While the option on American stocks have set expiration dates they may be executed by the holder at any time.

I learned this the hard way when a large call position I had written against Parker Hannifin (PH) was assigned, meaning an owner chose to exercise the calls in advance of their expiration date and my calls were among those randomly selected by call holders who wished to exercise and buy the stock at the call price. This was disastrous because I had written calls rather than selling the stock because I had large capital gains and wanted to avoid paying the cap gains taxes while continuing to own a stock I liked a lot.

I had done this a few times before. My trick was to watch carefully as expiration day approached and buy the calls back. No such luck this time. I lost the Parker Hannifin in my account and never bought it back. Meanwhile the PH I bought for my wife’s separate portfolio and didn’t hedge has now turned into a big winner. I had to pay the IRS the cap gains tax I was trying to avoid and lost the fun of patting myself on the back and telling myself how clever I had been. I also lost the arrogant belief that I could outsmart the market. What I gained was a lesson in my own limitations. It was the last time I ever tried to use options to hedge.

Fortunately there are a few other approaches which have an impact similar to traditional hedging. A couple of them are mentioned in the previous section. Here’s the short list:

- Own solid well-researched companies bought and held at cheap prices on the high probability that they will survive and continue to prosper.

- Own a portfolio that is truly diversified. By truly, I mean having positions which respond differently to various market conditions. Large defense companies, for example, grow slowly but dependably and have a customer who always pays its bills. Insurance companies always sell at a value price but have decent growth and modest risks not correlated to most of the market.

- Sell a bit of something. Perhaps a few shares of a stock or two in your portfolio you like the least. Perhaps better yet, a stock or two which has grown to such an overweight position that sudden bad news would do major damage.

- Have some cash and near-cash in reserve especially when you are well paid for it as you are in the current market environment. It will reduce the percentage your stocks are down and enable you to buy if the market gets really cheap. My current allocation is 60-20-20, the latter two numbers being fixed income up to five years and money market. The 5.5% plus return will feel good in a major correction.

- If confident in your holdings do nothing at all.

There are probably a few other ways to minimize losses in a large correction and if you can think of any I would like to hear them. One thing not to do, I should say, is rush out and sell like crazy.

Some Thoughts On Current Market Conditions

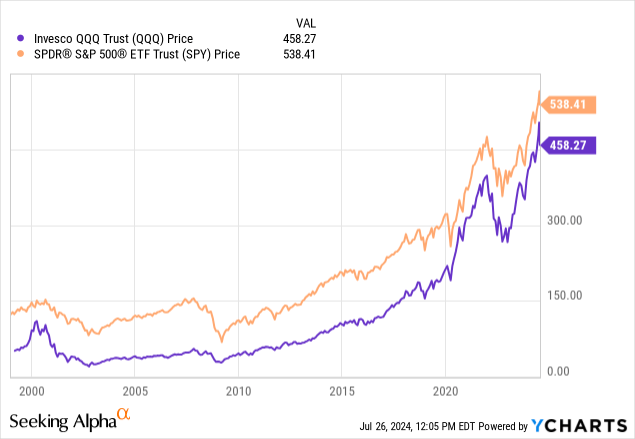

Of the three major market crashes discussed above the one which most resembles the present is the dot-com collapse which took place from 2000 to 2003. The dot.com stocks were absurdly expensive and the market was dominated by inexperienced speculators who thought they were savvy investors. The economy, on the other hand, continued to do well before finally succumbing to a brief and mild recession driven mainly by stock market losses. It’s a measure of the degree that tech stocks were overpriced that the Nasdaq 100 (QQQ) fell over 80% and did not break out to a new high for a decade and a half. The chart below compares the QQQ to the S&P 500 (SPY) which itself has many tech stocks (the value index not existing until later):

In the earlier section I discussed hedging the 2000-2003 crash. Appearing on Wall Street Week the Friday before the QQQ peaked Sir John Templeton, the greatest strategic investor of all time, recommended getting out of the market and buying intermediate term Treasuries yielding 6%. Although I owned a few Treasury Zero Coupon bonds with a couple of years left to maturity I thought about Sir John’s argument and bought Treasuries on Monday morning. I already owned a couple of small-cap value stocks. Berkshire Hathaway, which had been cut in half since 1998 (when Buffett told the world don’t buy, it’s overpriced), bottomed on exactly the same day the Nasdaq 100 peaked and a few days later I added to my position. Those were my hedges for the 2000 crash. I had never owned any of the high flying tech stocks because I found it unimaginable that they would ever justify their prices and couldn’t understand most of them anyway.

The major similarities between 2000 and today include the major divergence in valuation and performance between growth and value, the fact that growth is very expensive, the fact that many market participants are poorly informed and inexperienced newbies, and the fact the economy is in decent shape without any solid reason to worry about anything more than a modest recession. It’s important to recognize that many of the high flying tech oriented companies have solid fundamentals. It’s just that they’re very expensive. That 34 QQQ price earnings ratio means that their growth must continue for several decades without slowing. That’s a long period to bet on.

Recently value and growth have traded places quite a few times in large moves to the upside and downside. You can track this easily by looking daily at the percentage moves of Vanguard Growth ETF (VUG) and Vanguard Value ETF (VTV). A fact to keep in the back of your mind is that growth doesn’t worry much about recessions as it creates its own growth and generally prefers low rates because they provide a lower discounting denominator for future growth. Value is, well, value, and tends to come to the fore when growth is expensive. In most recent weeks value has been pulling net ground on growth. Will it continue? Always keep an open mind.

Most of the above observations are simple common sense backed up by knowing quite a bit of market history and having about six decades of market experience. I’m sure most readers have something to add and will welcome and reply to all comments. I should add that I will be leaving tomorrow for a couple of weeks in Spain with daughter and grandchildren and will be out of touch for some days.

Read the full article here

")

")

")