")

")

Almost a year ago, I published an article: ‘TPI Composites: A Spoon Is Dear When Lunchtime Is Near’ – an endeavor to defend a thesis that the worst was over for the business – it probably had to recover and resume growth slowly but surely. Alas, that did not go well. Two days after the publication, the price went down more than 30%, and in November 2023, it touched an absolute low of $1.63. This time, I ventured to refresh facts and figures on TPI Composites (NASDAQ:TPIC) to comprehend where the company is standing now, for readers and especially myself. The situation is far from being bright and risks are excessive, but is the end so obvious? Let us see.

The company is a cheap and close-to-the-site producer of wind blades for Vestas Wind Systems (OTCPK:VWSYF), GE Vernova Inc. (GEV), Nordex SE (OTCPK:NRDXF), and ENERCON. It must sell its blades for less than these companies could’ve produced themselves. The situation has always demanded that TPIC sacrifice its profitability for growth. However, when the growth started to fade in 2021-22, the business faced big problems, and bankruptcy in a couple of years is what investors fear now. It all depends now on the company’s ability to light up revenue growth back to its historical trend.

Reexamination of financials

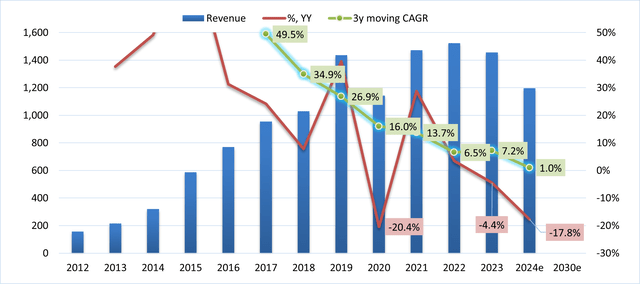

Revenue, YoY change, 3-year moving CAGR (Financial reporting and Author’s estimates)

As the chart above tells, the revenue peaked a couple of years ago at around $1.4+ billion, so the first leg down (excluding COVID-19 year) in 2023 looks logical now, coinciding with a killing cyclical downturn in the clean energy industry, especially in solar energy. The only but intensely bright spot is that TPI Composites still makes over 1 billion in sales, walking a long way from a sub-200-million business ten years ago. The new “windy” day may not be over the corner, but things in motion remain in motion.

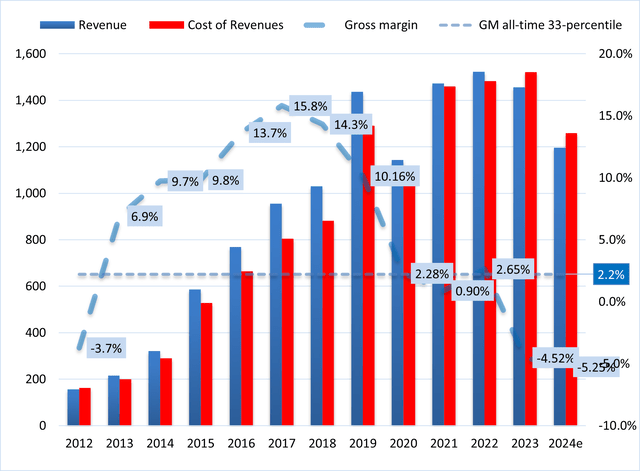

Gross margin (Financial reporting, Author’s estimates)

The bars and curve above indicate that at this scale of business and this economy, TPIC has been scrambling to make ends meet to cover the costs of goods sold. I thought 2023 would turn things around for the company. Well, not today. On the other side, purely statistically, the company might at least reach out for a low bar placed at the 33d-percentile of the gross margin at 2.2%. If that ever happens, then it won’t be so unusual, since economies and companies go through different phases of the cycle.

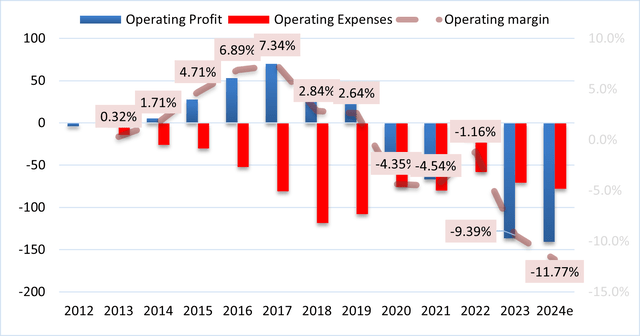

Operating margin (Financial reporting, Author’s estimates)

There is an even more horrific chart than the one above – ‘The profit margin curve.’ But let’s stop here because it suffices to admit that TPI Composites stopped showing positive operating profit in 2020. However, if we are somehow disabled from seeing the results for 2023 and my pessimistic estimation for 2024, one could have thought (as I did in yearly 2023) that the curve is slowly emerging. It’s hard to imagine that now.

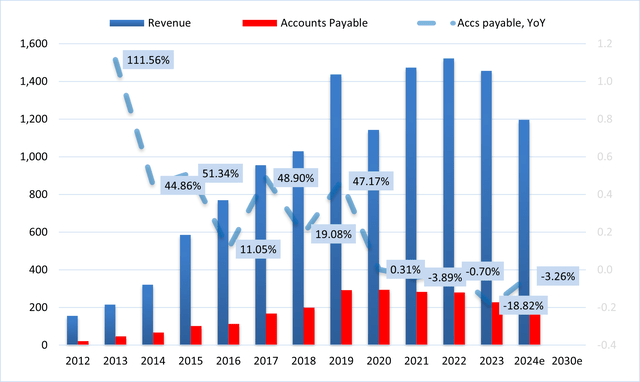

Accounts payable vs Revenue (Financial reporting, Author’s estimates)

The picture above explains the interconnection between the dynamics of the company’s sales and a balance sheet article. When TPI Composites sees amplified demand for wind blades, it sure orders more raw materials and other goods from suppliers to meet new demand, and it usually shows as a swell in the Accounts payable. The graph indicates, though, that since 2021, the business hasn’t ordered more and thus doesn’t expect a lift in demand. There are limitations, since the end-of-the-year figures do not show the intra-year volume of accounts payable. However, multi-year dynamics still offer the general connection between these two metrics, which is not very optimistic. The management promises better figures in 2025.

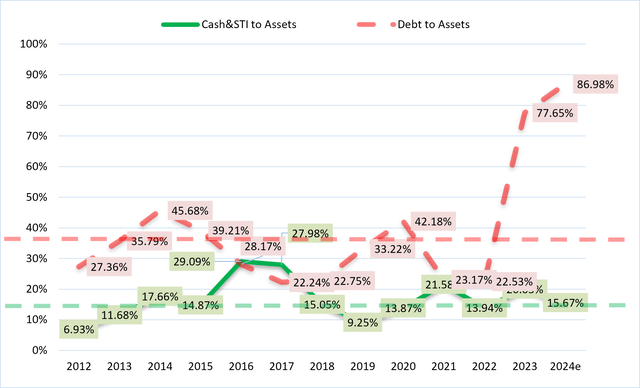

Debt and other adversities

As you can see on the following graph, the debt-to-assets ratio has skyrocketed above the all-time average at 41+% and the all-time peak at 45.7%. That is super-bad.

Debt to Assets (Financial reporting, Author’s estimates)

What happened? In December 2023, TPI Composites restructured its debt through preferred shares owned by Oaktree Capital Management. The deal’s terms were well-wrapped during the fourth quarter earnings call by Bill Siwek, CEO:

…we refinanced our Series A preferred shares by converting the $350 million of Series A, along with $86 million of accrued pay-in-kind of dividends through a cashless exchange for $393 million of senior secured term loan and the issuance of 3.9 million shares of common stock. This refinancing improved our liquidity by about $190 million over the term of the loan, and we permanently reduced our obligations to Oaktree by about $90 million. We can now pick up to 100% of interest payments through December 31, 2025, and up to 50% of interest payments from January 1, 2026, through the maturity on March 31, 2027. This agreement provides us with significantly greater financial flexibility and along with the $132.5 million convertible green bond we issued earlier in 2023 provides us with the liquidity we expect to need to fill our existing capacity, manage through the current market conditions and ultimately grow to serve our customers’ capacity…

So, on the one hand, they issued new debt at a junk bond’s interest rate of 11%, but on the other hand, they bought themselves two years of pay-in-kind, which means constant interest accrual but payment only in 2026, a window to turn things around. Nice. In 2026, even with a 50% discount, at least $393*0.11*2+$393*0.11*0.5= $108 million. That will be a big bite from a small pie of operating income; I’m wondering if they could pull this through.

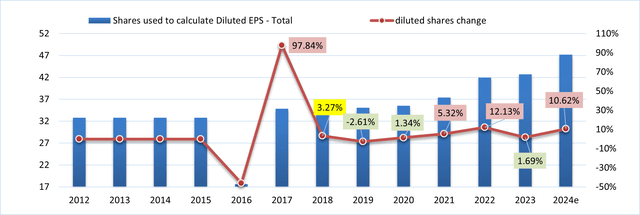

Given that the company has already crossed most of the lines of value investing, why wouldn’t it stop diluting current shareholders by double-digit figures!? So be it! However, that is a big deal for investors and the one stand-alone reason to stay away from having anything more than low single-digit exposure to this stock.

change of shares outstanding (Financial reporting, Author’s estimates)

Reasons to avoid depression having TPIC

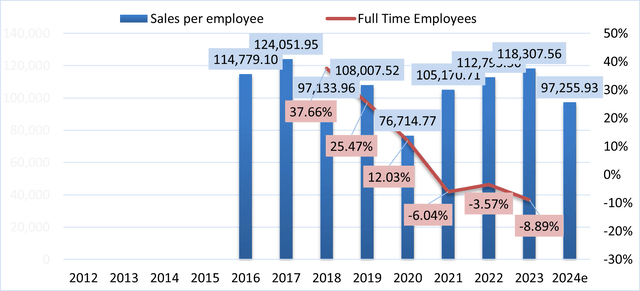

First. When times are tough – cut costs and headcount, this common maneuver has been employed to juice the maximum out of stumbling sales. That can help weather a challenging environment; since 2020, the Sales per employee ratio has improved for all fully reported fiscal years. And though $100K a year per associate is miserable for a manufacturing company, at least they are working on it.

Revenue per employee (Financial reporting, Author’s estimates)

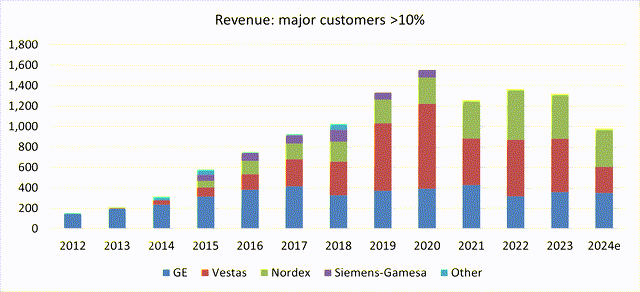

Second. One of the strongest and brightest feats of this business is that I can’t figure out how a company can go under in the long run having the following customers. Their relationships are certainly unhealthy for the TPIC now. Nevertheless, a better deal can be struck between them, eventually.

Major customers (Financial reporting, Author’s estimates)

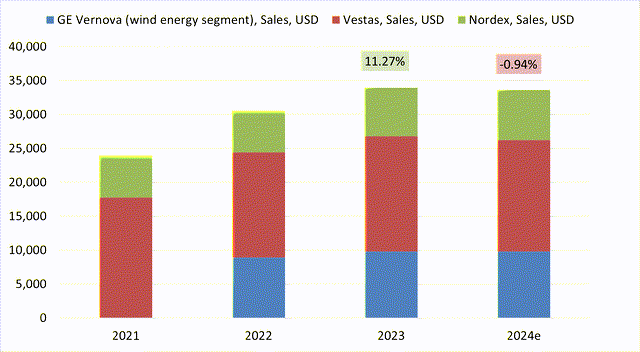

The graph below is roughly made by summing publicly available sales data figures, except for GE Vernova for 2021, which was unavailable. But it gives general information on scale. So, at almost $34 billion a year and pessimistically double the figure of backlog for the next several years, the environment for TPIC is nothing short of optimistic. If only the latter could play its cards right, the ongoing nightmare may be soon over, and brighter days lie ahead.

Major customers sales (Tikr.com, Author’s estimates)

Third. According to the “Key trends and recent developments” section of the 10Q report:

- Management is retooling some of the manufacturing lines for the next generation of wind blades as their customers anticipate stronger demand in early 2025;

- Later this year, TPIC thinks that retooled lines can start serial production and thus bring a positive FCF at the end of 2024.

Another small yet positive change is that the company gave up on its automotive segment, which was just 2% of the 2023 sales, but still, maybe it has never been in a good direction. Hopefully, they can truly focus on its primary market.

How to approach the stock

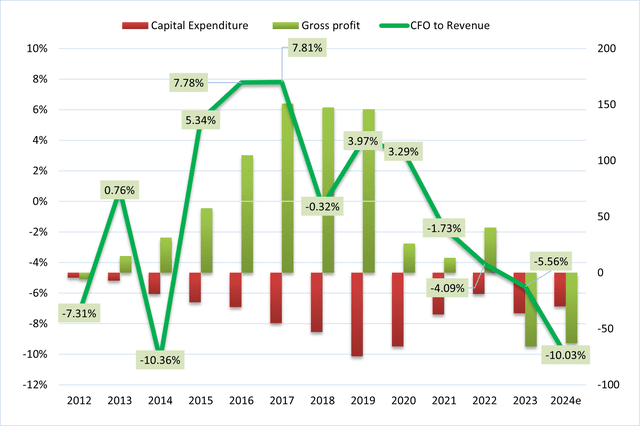

The company’s current state of cash flows and its historical performance are indefensible, so there is no way an investor can manage a DCF without stretching assumptions too wide. Be my guests and inspect the following chart.

Cash flows (Financial reporting, Author’s estimates)

No Free cash flow. Mounting net debt. The model is impossible for me. However, there is a price for everything under the moon in the market, and once traders believed that the company’s stock should be worth $50-70, as many believe that NVIDIA (NVDA) should cost as it costs now. If the recovery in wind energy in late 2024 or most probably in 2025 takes place, then the market’s assessment of TPIC is impossible to predict; the stock is quite speculative and can travel in a wide range.

I have witnessed at least three major cycles in the clean energy industry, and several fossil fuel crashes, to expect a pretty robust recovery eventually. So my recommendation for the stock will be:

- If you don’t own this stock – do not touch it even with a long stick at this price;

- If you have elevated compared to your average position size exposure (that is over 6% for me for this kind of risk) – try to decrease it to a level where you can accept total bankruptcy of the business;

- If you have a small position, bought back in the second half of 2023, try to keep it through 2025. Worth a shot.

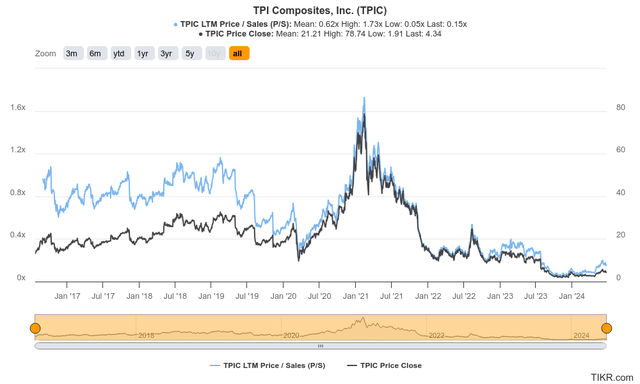

I came up with a simple way to assess a potential mean reversion but a pretty modest one: 25-percentile for the Price to Sales ratio since 2016 is 0.29, expected sales for 2024 are $1.3 billion, diluted shares outstanding are 48 million; thus, $1.3/0.048*0.29=$7.85 a share. That’s achievable in a moderate environment. If things start to look up in 2025, the range can return to double digits. However, truth be told now that sounds like a fantasy.

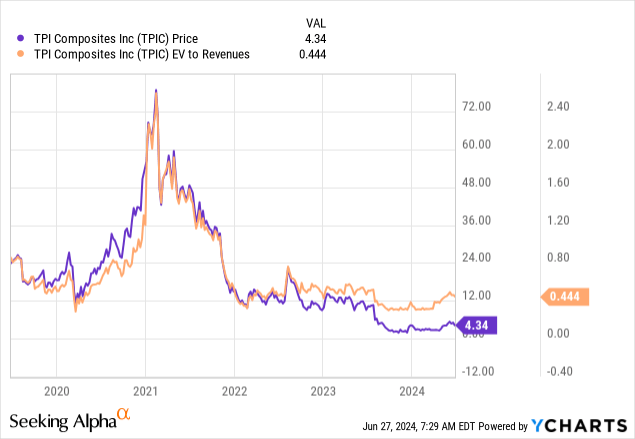

Price and P/S (Tikr.com)

Risk factors

1) Value investing metrics all say against this investment, the financial health of the company has been in terrible shape for a considerable amount of time;

2) The stock price went from low teens down to $1.63 and back to above $5, so the volatility has been extreme for the last couple of years. Any digress from the recovery plan will result in returning to the $2 price mark;

3) The poor shape of the company’s financials and the constant cash burn make this company vulnerable, and yet another debt restructuring can happen in the 4th quarter of this year.

Read the full article here

")

")