")

")

Amid recent market turmoil, the real estate industry has still been unable to claw back from several years of post-pandemic softness. High-interest rates continue to eat away at both buyers’ affordability and sellers’ willingness to move, creating a unique world in which very few homes are changing hands.

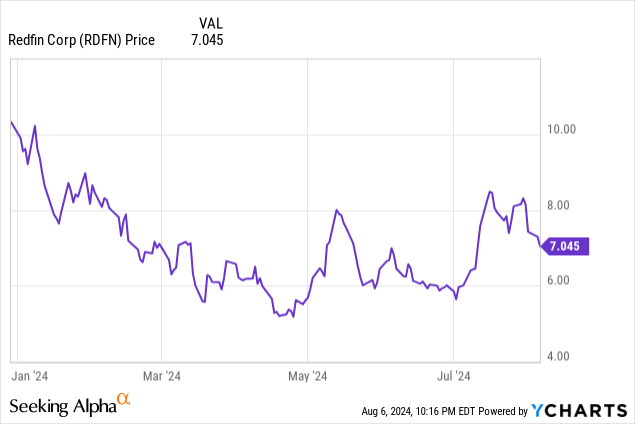

Against this backdrop, Redfin (NASDAQ:RDFN) has slashed costs and dramatically updated its business strategy. But so far, we have yet to see meaningful results. The brokerage company just reported Q2 results, and though it touted revenue growth, that growth is largely a function of easy prior-year comps, and the stock fell in response to the earnings news anyway, bringing YTD losses to over 30%.

I last wrote a bearish note on Redfin in May. Q2 results, and the upcoming changes to buyers’ contracts in the U.S. real estate industry, don’t inspire any additional confidence in me. I’m reiterating my sell rating on this stock.

Major change is coming in August to the real estate industry, and it’s unlikely that Redfin will benefit

Before we dive into Redfin’s latest quarterly woes, we’ll discuss the elephant in the room first: the upcoming changes to real estate rules that will start in August. As most industry-watchers are aware, the real estate industry is digesting major changes after a judicial ruling against the National Association of Realtors (NAR) that contended the association conspired to keep real estate fees high for consumers.

After months of speculation on what changes the ruling would have on the industry, we now have our answer. Starting in August, the two key changes that investors should be aware of are:

- Home listings can no longer advertise commission fees for buyers’ agents

- Home buyers will now be required to sign a buyers’ agency agreement, whereas previously, home buyers worked with buyers’ agents on a more loose basis

This means that the “old world” in which sellers paid up to 6% of their home’s value to both agents (usually evenly split between the sellers’ agent and the buyers’ agent) is gone, and fees will be fully negotiable on both sides. The intent of the ruling is to encourage buyers and sellers to negotiate their agents’ fees more aggressively, and bring down the 5-6% commission rate (in total) that has become the common benchmark for the industry.

Of course, these rules haven’t taken effect yet, and many are still speculating on the ultimate impact of these changes and how long they will take to truly change market norms. In my view, however, these rules will serve to A) lower overall brokerage commissions as more buyers and sellers negotiate fees, which is in the initial spirit of the NAR lawsuit, and B) fewer buyers will choose to work with buyers’ agents.

Redfin, Zillow (Z), and the world it created – in which buyers can shop an entire market of appealing listings on their own, without needing an agent to comb through the MLS – will in some ways be Redfin’s own downfall. I expect more buyers’ agents will shift to specializing in “private market” or “off-market” transactions, but discount brokerages like Redfin that doesn’t specialize in this kind of work will lose a good chunk of its buy-side work.

Poor Q2 trends

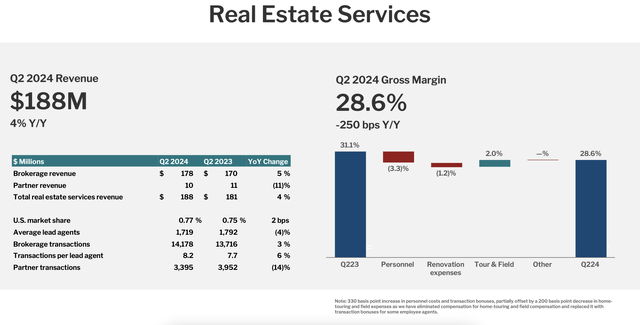

Even before any of these changes take effect, Redfin is already producing weak results. In Q2, total real estate services revenue grew only 4% y/y (with growth largely a factor of weak prior-year comps), decelerating from 5% y/y growth in Q1.

Redfin real estate results (Redfin Q2 shareholder deck)

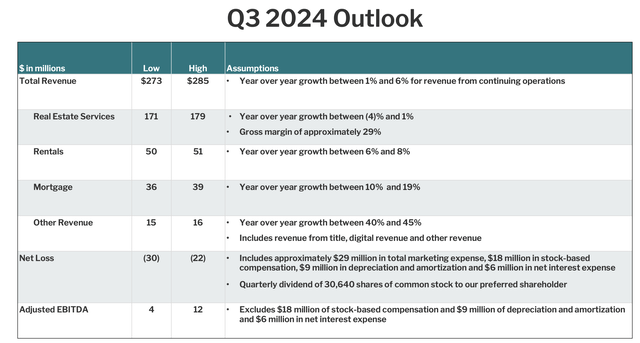

Making matters worse: Redfin expects conditions to get worse in the current quarter, Q3. Its outlook calls for real estate services revenue to decline up to -4% y/y, as shown in the chart below:

Redfin Q3 outlook (Redfin Q2 shareholder deck)

It’s still expecting growth in rentals and mortgage, but rentals – which has been a key offset to weaker transaction results – is expected to decelerate to single-digit growth, from 12% y/y growth in Q2.

Investors should also make note of the fact that Redfin’s real estate gross margins are sharply sinking, down 250bps y/y in Q2. The company has shifted its compensation structure to award more transaction closing bonuses to agents, instead of compensating for the number of tours. The net impact has been a sharp headwind to margins (and we note the real estate segment, which is Redfin’s core business, generates a negative adjusted EBITDA).

It’s worth calling out that at its outset, Redfin marketed itself as being different from competing brokerages by A) directly employing its brokers rather than paying them transaction commissions, which more closely aligns to clients’ incentives, and B) offering buyers’ agent rebates. With Redfin expanding its Redfin NEXT initiative (which is a standard brokerage commission split model), compensating more of its brokers on transactions, and eliminating buyers’ rebates, the company has lost virtually all distinction against traditional brokerages.

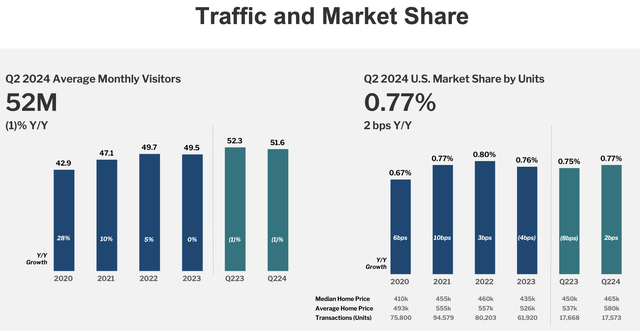

Perhaps as a result of this, the company has been unable to claw its way back to its historical 1%+ market share of U.S. real estate transactions. Its 0.77% share in Q2 was up 2bps y/y, but flat sequential versus Q1 and lower than where it was in 2022.

Redfin traffic and market share (Redfin Q2 shareholder deck)

Traffic as measured by average monthly visitors also declined -1% y/y.

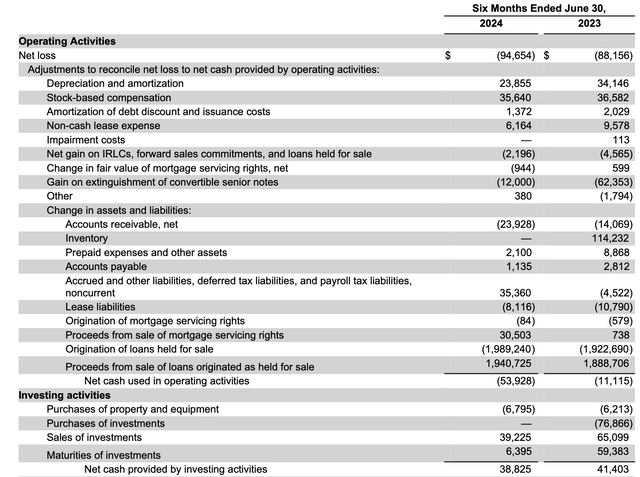

We note as well that Redfin’s operating cash flow in the first half of FY24 was negative, -$53.9 million; and after including $6.8 million spent on capex, total FCF was -$60.7 million:

Redfin cash flow (Redfin Q2 earnings release)

For a company that has only $201.8 million of cash left on its balance sheet (stacked against $1.02 billion of debt, for a net debt position of ~$816 million), these losses don’t point to a very stable future for Redfin.

Key takeaways

To me, Redfin is trapped with a declining brand that is no longer differentiated against local traditional brokerages, and to make matters worse, it’s pitted against changing industry rules that are likely to reduce commissions and buy-side work. Redfin’s historical reputation as a discount brokerage that offered buyers’ rebates makes it appeal far more to price-conscious customers, who are far more likely to forego buyers’ representation once they have to pay for it out of pocket. Continue to avoid this stock.

Read the full article here

")

")

")

")