")

After reviewing the first half of 2024 financial results for Givaudan SA (OTCPK:GVDBF)(OTCPK:GVDNY) our opinion of the business remains relatively unchanged. Perhaps the two biggest developments since our last article are a healthy recovery in its sales after a weak period caused by inventory destocking, and a further increase in the share price.

While confirmation that the sales weakness was temporary is a welcomed development, the valuation increase is not, especially when we were already worried about overvaluation six months ago. We are reluctant to rate shares of very high-quality businesses as a “Sell”, but we would not buy shares at the current valuation. We are therefore maintaining a “Hold” rating, but believe that at current prices shares will probably offer below average returns to long-term investors.

While the company touts a target of doubling its business by 2030, it is important to note the small print where it says that it is compared to a 2018 baseline of CHF 5.5 billion. While this represents real growth, it is not much different from nominal global GDP growth. On the positive side, the company does have high and stable profit margins, generates significant free cash flow, and we believe it has a strong competitive moat derived from its significant intellectual property assets and high customer switching costs.

Givaudan Investor Presentation

R&D and New Innovations

One thing we certainly appreciate about Givaudan is that it is continuously innovating in ways that improve the value of the products of its end customers. Whether to make them more sustainable, longer lasting, having a better taste, being more nutritious, or making them more healthy. Below is a slide of recent innovations the company has launched that include examples that go from beauty to alternative dairy ingredients.

Givaudan Investor Presentation

First Half 2024 Financial Results

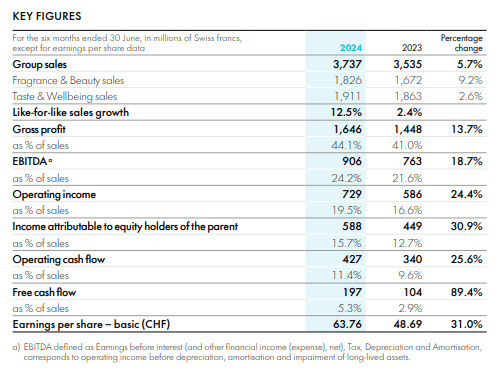

At first glance results for H1 2024 might appear very strong, with the company reporting like-for-like sales growth of 12.5%. However, investors should remember that the increase is compared to a period of significant weakness due to inventory de-stocking last year.

The increase is also significantly lower when measured in Swiss francs (CHF) given the appreciation of its reporting currency. This lowers growth to only 5.7% when measured in CHF. The recovery in sales did result in meaningfully higher profit margins, with the company reporting net income of CHF 588 million, which represents an increase of 30.9% compared to the previous year. Free cash flow was up considerably compared to the previous year, but still far from the company’s 12% target, as the CHF 197 million it generated in the first half of 2024 represent only 5.3% of sales.

Givaudan Investor Presentation

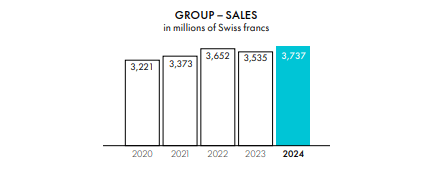

In the last four years group sales have only increased at a compound annual growth rate (OTC:CAGR) of ~3.7%, which is actually below the 4% floor in the company’s target. Adjusting for Swiss franc appreciation, organic growth has usually been above the company’s sales growth target, but we still find it too low to justify the elevated valuation levels.

Givaudan Investor Presentation

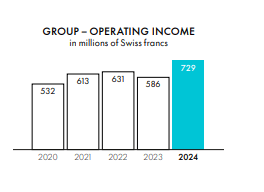

Similarly, in the last four years the company’s operating income has increased slightly faster, at a compound annual growth rate (OTC:CAGR) of ~8.7%. The strengthening Swiss franc has been a headwind the last few years which will not necessarily continue and might even reverse to a certain degree. For this reason, in our valuation model we assume slightly faster earnings growth going forward.

Givaudan Investor Presentation

Industry Developments

We believe that Givaudan’s industry has attractive characteristics for a variety of reasons. These include the fact that the ingredients they sell tend to represent a small percentage of the total cost of the end products but have a significant impact on their perceived functionality and quality. For their customers changing suppliers can be difficult, given that companies like Givaudan tend to own the intellectual property even when co-developed with the customer, and replacements might result in noticeable changes to the end product. There is also a scale benefit, as international companies like Givaudan can quickly ramp-up a new product given their wide sales and distribution networks.

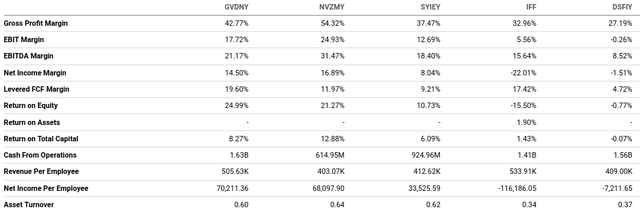

Compared to competitors like Germany’s Symrise (OTCPK:SYIEY) and International Flavors & Fragrances (IFF), Givaudan and Novonesis (OTCPK:NVZMY) have better profit margins. There has been significant consolidation in the sector, with Novonesis being the result of the combination of Novozymes and Chr. Hansen Holdings A/S, and DSM-Firmenich resulting from the combination of DSM with Firmenich. It is worth noting that several of these companies, including Givaudan, have been accused of allegedly participating in a pricing cartel. If true, this could mean profit margins for the industry are artificially higher and they could be potentially fined large sums in addition to whatever remedies authorities consider to be appropriate.

Givaudan Investor Presentation

Balance Sheet

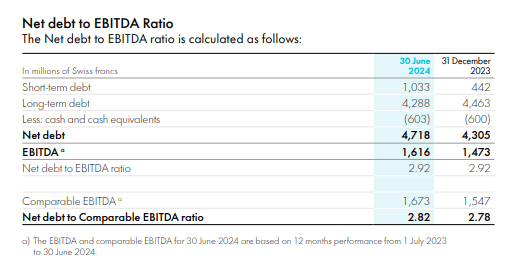

Givaudan’s balance sheet remains quite strong, with net debt to EBITDA only slightly higher than last year, and at a relatively low ratio of ~2.9x.

Givaudan Investor Presentation

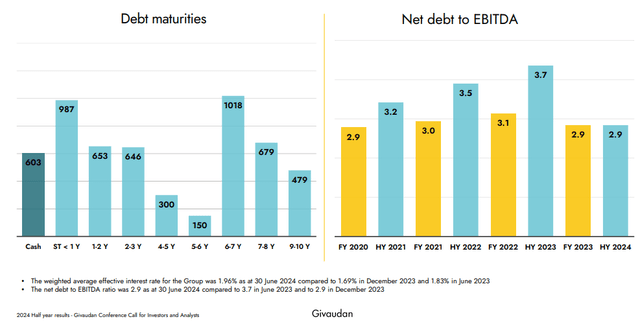

Givaudan also has a very well spread debt maturity schedule, which will help mitigate the headwinds of refinancing at higher interest rates, should they remain higher for longer.

Givaudan Investor Presentation

Decelerating Dividends

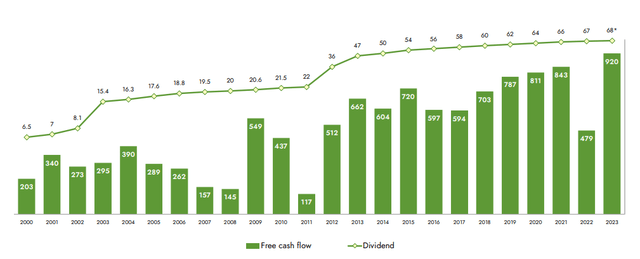

It has been some time since Givaudan shareholders saw a meaningful dividend increase, with the most recent one being a tiny 1.5% bump. The good news is that it is denominated in Swiss francs, which is considered a very solid currency and tends to particularly appreciate during times of economic or market stress. The bad news is that at current prices the dividend yield is only about 1.6%.

Givaudan Investor Presentation

Valuation

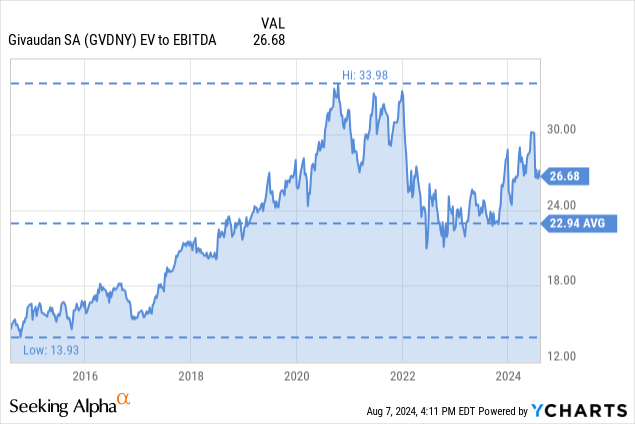

Givaudan is currently trading above its ten-year EV/EBITDA ratio, and it is difficult to get excited about a company with an EV/EBITDA above 20x and which is growing revenue barely above global GDP rates. Even if there is some operating leverage that could allow earnings per share (EPS) to grow in the high single digits.

Based on our estimated future earnings we calculate a net present value for the ADR shares of $96 when using a 4% discount rate. If we use a 10% discount rate we get ~$56. In other words, we believe that long-term investors are looking at potential returns barely above those offered by high-quality bonds in Europe.

| EPS | Discounted @ 4% | |

| FY 24E | $2.75 | $2.64 |

| FY 25E | $2.81 | $2.60 |

| FY 26E | $3.08 | $2.74 |

| FY 27E | $3.37 | $2.88 |

| FY 28E | $3.69 | $3.03 |

| FY 29E | $4.04 | $3.19 |

| FY 30E | $4.42 | $3.36 |

| FY 31E | $4.84 | $3.54 |

| FY 32E | $5.30 | $3.73 |

| FY 33E | $5.81 | $3.92 |

| FY 34E | $6.36 | $4.13 |

| Terminal Value @ 4% terminal growth | $96.80 | 60.46 |

| NPV | $96.22 |

Risks

The two main risks we see with Givaudan are the stretched valuation and the alleged participation in the price fixing cartel. With respect to the valuation, it is possible that the company continues to trade at a significant premium, with long-term investors generating low but positive returns. There is also the possibility that even a minor disappointment in future financial results could prompt a significant valuation readjustment. With respect to the legal issues, it is difficult to tell at this point what the financial impact could be, but investors should monitor this risk closely.

Conclusion

Despite a significant improvement in the financial results for the first half of 2024 compared to the first half of last year, it is very difficult to get excited about the shares at the current valuation. The legal risks add even more potential downside, with the upside being relatively limited in our opinion. On the positive side, the company continues to innovate and bring new products to market that offer attractive characteristics for customers. We also continue to believe that the company has a strong competitive moat, which should help maintain above average profit margins over the long-term and high returns on incremental investments. Given the improvement in the financial results, we are maintaining our “Hold” rating, but see limited upside at the current valuation.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here

")

")

")

")

")