")

Brendan Fraser yeets Peter Dinklage across a bathroom before water boarding him while demanding some emeralds. Then it gets weird")

")

Note:

Noble Corporation plc (NYSE:NE) or “Noble” has been covered by me previously, so investors should view this as an update to my earlier articles on the company.

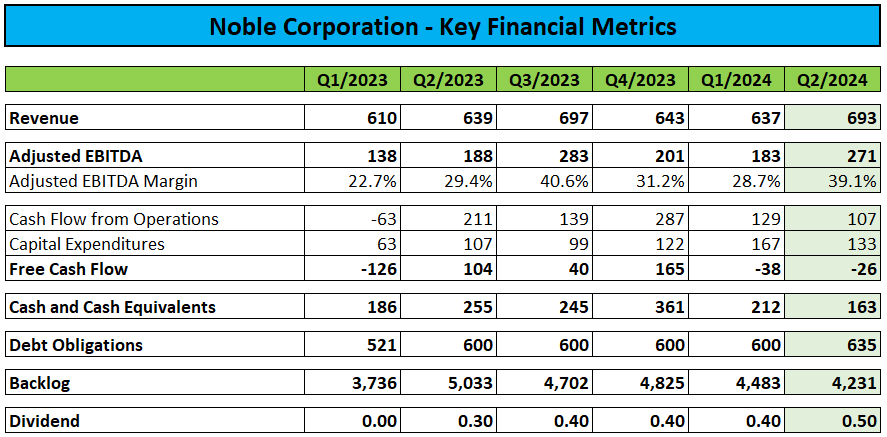

Earlier this month, leading offshore driller Noble Corporation reported strong Q2/2024 results with both top- and bottom line results coming in well ahead of consensus expectations:

Company Press Releases / Regulatory Filings

Adjusted for low-margin customer reimbursables, contract drilling revenues were $661 million with the outperformance seemingly due to a number of rigs working longer than originally expected.

Adjusted EBITDA of $271 million and Adjusted EBITDA margin of 39.1% represented strong sequential improvement.

However, cash generation for the quarter was impacted by higher working capital levels and elevated capital expenditures. As a result, free cash flow was slightly negative for the quarter.

Noble ended Q2 with $163 million in cash and cash equivalents and $635 million in debt. Net debt of $472 million was up by $84 million sequentially due to negative free cash flow in combination with the quarterly dividend payment.

Backlog was down by approximately 6% quarter-over-quarter to $4.2 billion as contracting activity remains muted. In fact, the only material backlog addition was the exercise of a priced option for the seventh generation drillship Noble Stanley Lafosse in the U.S. Gulf of Mexico.

The company declared a quarterly cash dividend of $0.50 per share, unchanged from Q1.

On the conference call, management provided its take on the rather disappointing deepwater contracting activity witnessed in recent quarters:

We recognize that there’s a growing need in curiosity about what’s causing the slower pace of awards of late. And while there’s not a single uniform answer, we believe that there are a few contributing factors at play with various parts of the customer base, including, first, capital discipline and stakeholder alignment complexities that are causing contracts to take longer to execute, including partner approvals, permits, et cetera.

Second, field development supply chain pinch points, resulting from the sharp rise in global project backlogs over the past few years; and third, short-term after effects resulting from upstream consolidation transactions, which has definitely been a factor at play in the Gulf of Mexico recently.

With these headwinds likely to persist for several quarters, management now expects the market to remain more or less flat “at least through the first half of 2025” with particularly weak demand for lower-specification units.

As a result, dayrates for high-specification assets are projected to remain steady in the near term while rates for lower-specification floaters might soften.

On the conference call, management appeared less concerned about the jackup market despite some recent distractions resulting from Saudi Aramco’s surprise decision to suspend the contracts of more than 20 jackup rigs on short notice:

(…) the global jackup market is quite strong, and it has stayed steady. It moved healthily straight through the more significant Saudi announcement from a few months ago. And we’ve seen a number of those rigs be redeployed elsewhere in the globe already. And so I think that market is generally pretty consistently strong.

However, commentary with regard to Noble’s stronghold in the jackup space was mixed:

The Northern Europe jackup market is characterized by moderately improving demand visibility in Norway for 2025, contrasted with a more cautious near-term outlook in the southern North Sea arising from policy and permitting uncertainty in the U.K.

With the vast majority of backlog tied to the floater segment, the protracted weakness in contracting activity will impact fleet utilization in the near term.

Even a high-specification drillship like the Noble Voyager is now expected to sit idle well into 2025. In addition, management expects near-term idle time for the lower-specification drillships Noble Globetrotter I and Noble Globetrotter II.

While the company is pursuing well-intervention work opportunities for these units, near-term contract awards are highly unlikely at this point.

However, the negative impact of increased idle time will be largely offset by the recent commencement of new high-margin contracts for a number of floaters.

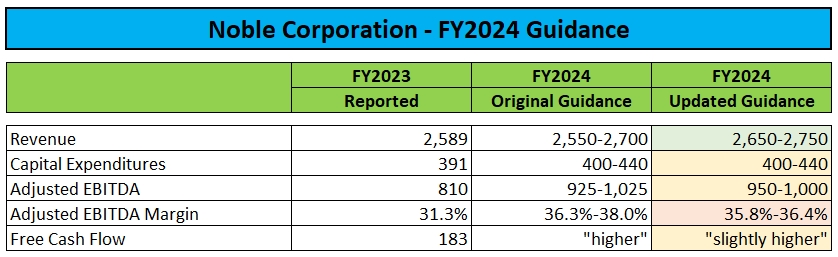

Consequently, the company tweaked full-year expectations. While the revenue range was raised slightly as a result of higher reimbursables and ancillary services, Adjusted EBITDA projections have been refined to a new range of $950 million of $1,000 million with the mid-point unchanged from the company’s previous guidance:

Company Press Release / Conference Call Transcript

Cash flow will be impacted by an insurance payment related to the late 2022 leg failure on the Noble Regina Allen likely pushing out into 2025.

With an estimated free cash flow of approximately $250 million in the second half of the year, management expects to resume share buybacks soon.

Subsequent to quarter-end, Noble raised $800 million in an upsized add-on offering of the company’s 2030 8% Senior Notes. As the deal was priced at 103% of face value, I would estimate net proceeds of slightly above $800 million. As a result, Noble will not require bridge financing for the cash component of the proposed acquisition of Diamond Offshore Drilling, Inc. (DO) which is expected to close in Q1/2025. In addition, the company added approximately $125 million in incremental liquidity.

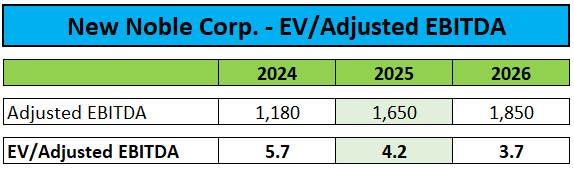

Following management’s cautious market outlook, I have reduced my Adjusted EBITDA estimates for 2025 and 2026. Please note that estimates include assumed contributions from Diamond Offshore Drilling:

Author’s Estimates

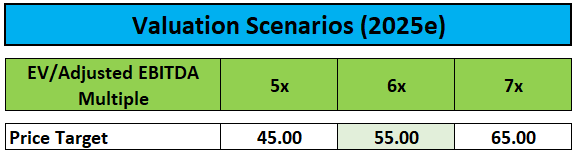

As a result, the price target for the shares which is based on an assigned valuation of 6x estimated 2025 EV/Adjusted EBITDA moves down from $58 to $55:

Author’s Estimates

Following the recent selloff in oil service stocks, the company’s shares are now providing for almost 50% upside to my revised price target. Please note also that Noble’s annualized dividend yield has increased to 5.4%.

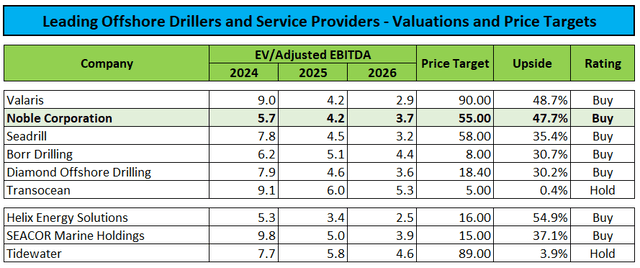

With the exception of Transocean Ltd. (RIG) and Tidewater Inc. (TDW), industry stocks have reached bargain levels in recent weeks:

Author’s Estimates

Bottom Line

While Noble Corporation reported better-than-expected second quarter results, management now anticipates muted deepwater contracting activity to extend well into next year.

Consequently, I have reduced my forward Adjusted EBITDA estimates and price target for the company.

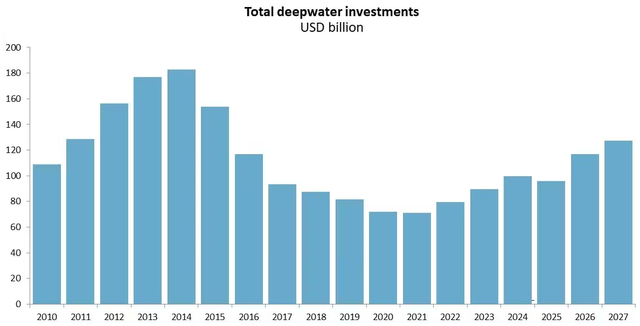

While 2025 might not play out as previously expected, long-term industry prospects remain solid with deepwater investments projected to pick up quite meaningfully in 2026 and 2027:

Rystad Energy

With share buybacks likely to resume in H2/2024 and the potential for higher quarterly payouts next year, I remain constructive on Noble Corporation’s prospects.

Following the recent selloff in oil and gas service stocks, the company’s shares now offer almost 50% upside to my decreased price target of $55.

Read the full article here

Q3 2024 Earnings Call Transcript")

")

")

")