")

")

")

Presidential elections in the U.S. are like grand slam tennis matches: strategic, competitive, and marked by long rallies of back-and-forth action. The ball ricochets back and forth across the net, with each candidate’s policy serve affecting different parts of the financial court. But how do these political volleys impact the critical world of securities lending and financing in the US? Let’s take a swing at it!

The Pre-Match Jitters: Uncertainty Breeds Opportunity

In the months leading up to an election, the market behaves like a nervous player waiting for the match point. Uncertainty surrounding potential policy shifts leads to higher demand for borrowing securities, as traders hedge their positions. This increase in borrowing drives up fees in the securities lending market. For example, if a candidate is perceived as unfriendly to a particular sector, say tech or healthcare, investors might borrow those securities more frequently to short them in anticipation of potential regulatory changes. It’s a little like preparing for an opponent’s signature serve – you brace for impact and adjust accordingly.

Service Ace: Tech and Healthcare as Top Targets

As seen during 2020, sectors like technology and healthcare have been major players on the election court. Much like in tennis, where certain players dominate certain surfaces, these industries may face policy changes depending on the administration. A pro-regulation president might introduce stricter antitrust rules or healthcare reforms, causing increased volatility. The resulting market moves drive short sellers to borrow stocks in these sectors, contributing to an uptick in revenue from lending fees. Think of it as a powerful service ace: the ball hits the ground hard, leaving traders scrambling to position themselves. A surge in short interest results in greater demand for securities borrowing, which in turn boosts the revenues of market participants involved in lending.

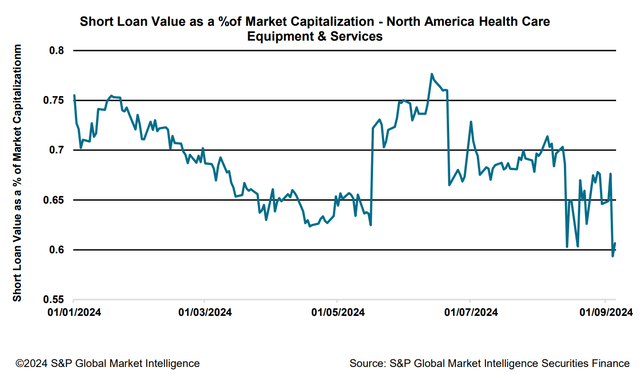

Across the Health Care Equipment and Services sector, in 2020, volume weighted average fees (VWAF) climbed from 40bps on November 1st to over 90bps by mid-December as a new President prepared to take office. A similar move was seen across Tech stocks, where volume weighted average fees started 2020 at 55bps and finished that year at 104bps.

So far during 2024, short loan value across the Healthcare Equipment and Services sector has been in decline, but the trend has started to show increased volatility moving into the second half of the year.

Volleying Back: Energy and Financials in Play

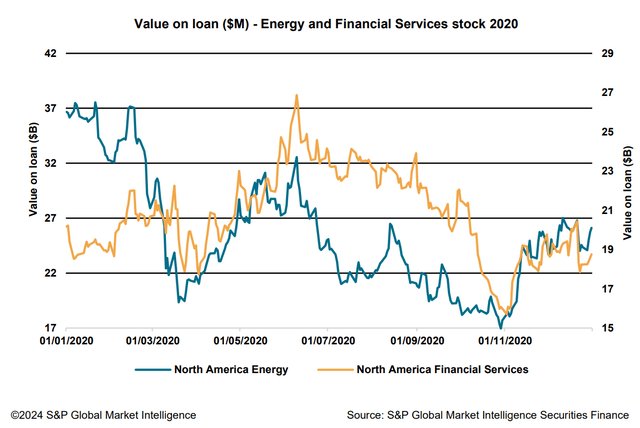

On the other side of the court, energy and financials often react like baseline players. A conservative, business-friendly administration tends to lift these sectors, with policies that support oil drilling or deregulate banking. These rallies in stock prices reduce short-selling activity in these areas. However, the flip side of this is an increased demand for borrowing securities to take long positions, particularly in options or futures markets. The energy and financial sectors may, therefore, experience their own unique surges in borrowing demand during election years, contributing to financing market revenues.

As seen in the graph, during 2020, sharp upticks in the value on loan for both sectors were seen after the result of the Presidential election was announced in November. Until that point in the year, value on loan across both sectors was in decline. So far during 2024, Energy and Financial Services stocks across North America have proved popular borrows. The Energy sector has remained within the top five most shorted sectors across the region, and Financial Services has remained within the top ten.

Second-Serve Opportunities: Rising Interest Rates

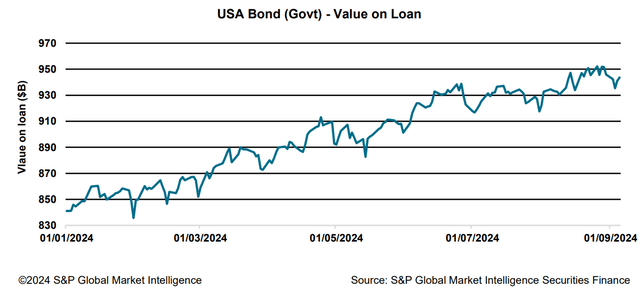

Interest rates are like the slow, deliberate second serve in tennis: they might not have the same speed as a first serve, but they’re just as crucial to winning the point. If an election results in a government that favours fiscal stimulus or infrastructure spending, bond yields might rise, increasing borrowing costs. As interest rates climb, the cost of financing goes up across the board. But here’s where it gets interesting: this tends to lead to higher revenues for securities lending desks, as the cost of borrowing assets is directly tied to interest rates.

It’s the ultimate double fault for some, but a winner for others in the lending space. As can be seen, the value on loan of US Treasuries has been increasing throughout 2024 and is expected to do so heading into the election months as future policy continues to be debated.

Drop Shots and Dives: The Impact on Microchip, and Semiconductor Stocks

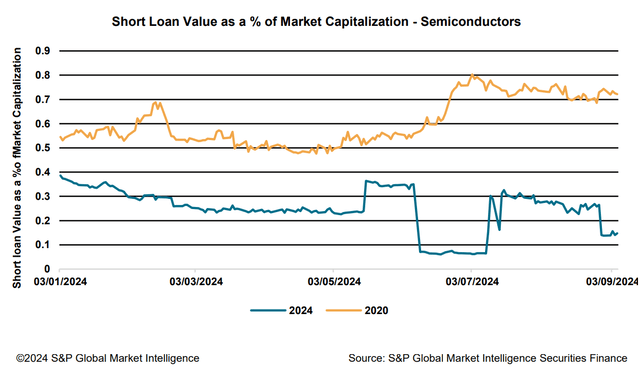

When it comes to tech stocks, particularly microchips and semiconductors, elections are like fast-paced drop shots – quick and often game-changing. These sectors are sensitive to policy shifts related to trade, intellectual property, and national security. A protectionist stance may impose tariffs or restrict trade with key manufacturing hubs, causing sharp drops in stock prices. This heightened volatility prompts more short-selling activity in tech, microchip, and semiconductor stocks, increasing borrowing demand and elevating lending fees. For instance, the 2020 election saw semiconductor stocks in the spotlight as trade tensions intensified, leading to substantial borrowing activity (as seen in the elevated level of short loan value in 2020 compared to 2024) as traders hedged their bets. Much like a well-placed drop shot, these sectors can experience sudden price swings, creating profitable opportunities for securities lenders and borrowers alike. The back-and-forth play in this space keeps the financing market on its toes, driving up revenues when uncertainty spikes.

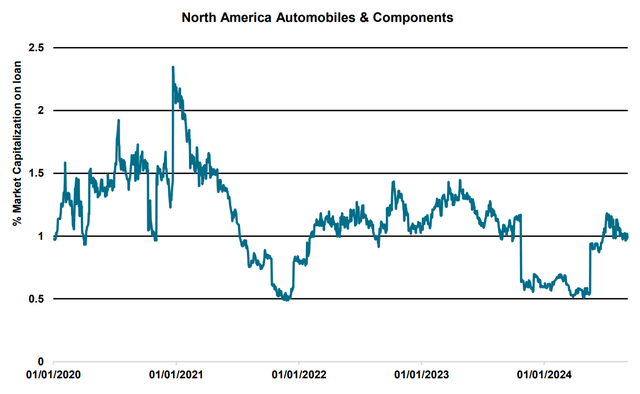

The Steady Baseline and Strategic Play: Utilities and Automobiles stocks

In the world of securities lending, the utilities and automobile sectors play their games a bit differently, akin to steady baseline players and strategic doubles teams. Utilities are like the reliable baseline players – consistent and less prone to wild swings, but still subject to strategic moves. Election outcomes can impact utilities through changes in regulatory policies or energy strategies. For example, a green-energy-focused administration might boost renewable energy stocks, causing a shift in borrowing patterns as investors adjust their positions. Conversely, a deregulatory stance could prompt more borrowing as traders anticipate changes in utility rates or infrastructure spending.

The automobile sector, on the other hand, is more like a doubles team, where strategic positioning and coordinated plays matter. Elections that favour increased infrastructure spending or incentives for electric vehicles can drive up borrowing demand in this sector as investors position for growth. However, any signs of trade restrictions or regulatory hurdles can lead to defensive borrowing strategies, with investors hedging against potential downturns. In both cases, the elections serve as a pivotal game-changer, with policy shifts influencing borrowing dynamics and revenue flows, much like how a well-placed lob or strategic volley can turn the tide in a tennis match.

The largest peak in the percentage of market capitalization on loan across the Automobile and Component sector over the last four years was seen following the previous Presidential election, during December 2020. Despite this metric falling since, it has started to climb again recently, and has remained above 1% since July. The sector remains within the top five most shorted sectors across North America as a result.

Tie-Breakers: Volatility’s Impact on Revenues

When the election match gets down to the wire, volatility shoots up like an intense tiebreaker. Sectors across the board see price swings as election day nears, further driving demand for securities borrowing. For investors, this volatility is like playing against a top-seeded opponent: you need every trick in the book, from shorts to derivatives, to manage risk. The result? Higher revenues and increased fees (which are now being seen across the region) as the financing market thrives on the uncertainty and volatility that elections can bring.

It’s Game, Set, Match – Until the Next Election

At the end of the day, the U.S. presidential elections are a key rally point for the securities lending and financing markets. Just like a fiercely contested tennis match, each volley of political developments can drastically change the momentum. Whether it’s healthcare facing a blistering return or energy benefiting from a well-placed lob, the game isn’t over until the final vote is counted – and the market has plenty of opportunities to score big points along the way.

In the securities lending arena, elections are more than just politics – they’re the championship match!

Original Post

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Read the full article here

")

")

")

")

(OTCMKTS:HESAF)")