")

")

")

")

When looking for value, investors should search beyond just the well-known names in order to find opportunities that reward their due diligence.

This can mean considering stocks that the average investor is not as familiar with.

One relatively unknown name that appears to offer good value at the current price is Maximus, Inc. (NYSE:MMS).

Maximus has returned just over 11% over the last year, about half of what the S&P 500 Index has generated, but the stock is trading well below its historical valuation. At the same time, the company has some tailwinds that could send its share price higher. This article will examine why Maximus could offer excellent value.

Company Background

First, a quick review of the company as it is one of the more under covered names in the market, with just three analysts following the stock.

Maximus is a provider of government health and human services programs, with operations primarily located in the United States. The company has three reportable business segments, including U.S. Federal Services, U.S. Services, and Outside the U.S.

- U.S. Federal Services delivers end-to-end solutions, such as process services, outreach, eligibility, and enrollment services, that are used to assist a multitude of various federal government agencies

- U.S. Services offers business process services, such as program administration, beneficiary outreach, and application assistance.

- The Outside the U.S. segment provides similar services to international and commercial clients.

Maximus has operations in 8 other countries outside the U.S., including the United Kingdom, Canada, Australia, and Saudi Arabia. The company generates annual revenue of nearly $5 billion and has a market capitalization of $5.3 billion.

Recent Earnings Results

Maximus reported excellent third quarter earnings results on August 7th, 2024.

MMS Investor Relations

Revenue for the period grew 10.1% to $1.31 billion, which was $20 million above estimates. Adjusted earnings-per-share of $1.74 compared extremely favorably to $1.04 and topped expectations by $0.22.

Growth was seen throughout the business, but especially for the U.S. Federal Services segment. Revenue grew 17% to $683.3, which represented 52% of total sales. Gains were driven by much higher volume for clinical programs.

Revenue for U.S. Services improved 5.2% to $472.3 as this business saw improved performance across its Medicaid-related portfolio.

Outside the U.S. experienced a 2.3% gain in revenue to $159.3 million, mostly due to better operations in the U.K. Organic growth for this segment was 6.8%.

Following a strong quarterly report, management raised much of its guidance for the full fiscal year.

MMS Investor Relations

The company now projects adjusted earnings-per-share in a range of $6.00 to $6.20, up from $5.65 to $5.85 previously. At the midpoint, this would be a 59% increase from FY 2023.

Takeaways From Recent Earnings Results

Maximus generated impressive results for the period, with organic growth coming in ahead of reported figures at 11.2% for the quarter. All three businesses contributed to this gain, with U.S. Federal Services being the top performer.

Revenue growth for the company has rarely been an issue, as the top-line has increased every year for the last decade except for 2018. This results in a CAGR of almost 12% for revenue for the period.

Much of this gain in revenue flowed to the bottom-line as well, as the operating margin of 10.8% was up meaningfully from 4.9% in Q3 2023. Compared to the prior year, the operating margin for U.S. Federal Services expanded 280 basis points to 15.5% while U.S. Services improved 250 basis points to 13.0%.

Outside the U.S., which has undergone divestitures in order to shrink its footprint, had an operating margin of -0.9%, which is an improvement from the -9.8% figure this business had last year.

Overall, the improvement in the operating margin was a welcomed development as Maximus has struggled to grow its margins over the last decade. For the 2014 to 2019 period, the operating margins were above at least 11% each year. Since then, margins have fallen every year except for 2021.

The company has benefited recently from demand for the company’s products, which has led to double-digit revenue growth. Maximus is a leader in its industry and has the expert knowledge to help it navigate complex government programs.

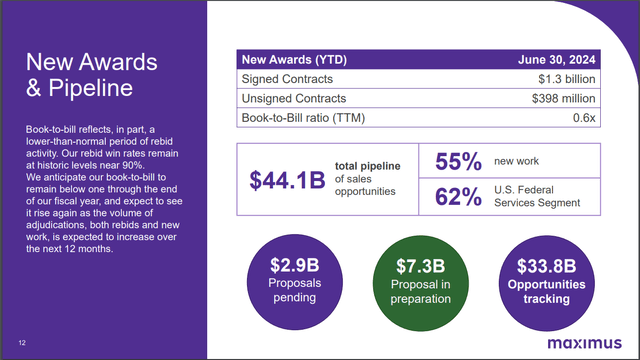

Because of this, they have been quite successful at landing government contracts. The company signed contracts in the amount of $1.25 billion year-to-date through the end of the most recent quarter. On a twelve-month basis, the book-to-bill ratio was 0.6.

It should be noted that this was down from a book-to-bill ratio for the last twelve months of 1.1 at the end of the second quarter. Management noted that the most recent period had fewer rebid opportunities than normal, but the company has a rebid win rate of almost 90%. This is a historic level for Maximus and shows that its customers view the company’s products as key to their business. The vast majority of customers continue to sign renewal contracts with the company, which will provide additional tailwinds for its business.

The company has an extensive pipeline that will help drive future growth.

MMS Investor Relations

Maximus has a massive adjustable market of close to $34 billion by the company’s estimation. It also has proposals pending of $2.9 billion and $7.3 billion of proposals in preparation. Maximus has no shortage of future work, which is highly encouraging considering its ability to retain customers.

This, in turn, should promote significant improvements in the company’s margins.

Despite past margins leaving much to be desired, Maximus anticipates that its two largest segments, U.S. Federal Services and U.S. Services, will have operating margins of 12.5% and 13%, respectively, for FY 2024. In both cases, this would represent an expansion of at least 210 basis points from FY 2023.

This helps to explain why management is so bullish on its fiscal year forecast.

Furthermore, the company is taking steps to improve its balance sheet. Maximus has repaid $1.18 billion worth of debt over the last year, including paying down $488 million in the third quarter. As of the end of the quarter, Maximus’ ratio of net debt to EBITDA on a trailing basis was 1.5x compared to 1.7x in the prior quarter. This was down from a ratio of 2.2 as of the end of FY 2023, so Maximus is making meaningful progress is reducing its debt obligations.

Nearly 60% earnings growth is not sustainable for Maximus, but the company’s leadership position in its industry allows it to win initial contracts and then win renewals at an extremely high rate. For these reasons, I believe that the company should see at least 7% earnings growth moving forward, which is slightly ahead of the company’s long-term CAGR of 6.8%.

Dividend Analysis

Admittedly, Maximus does not possess the dividend growth track record that I typically look for as the company has been known to pause its dividend for long periods of time, including from FY 2012 to FY 2018 and again from FY 2020 to FY 2022. Despite this, Maximus has distributed a dividend for 18 consecutive years.

Even so, the dividend growth rate has been exceptional with a CAGR of close to 23% per year over the last decade thanks to a massive increase in FY 2019 that brought the annualized dividend from $0.18 to $1.00 per share. Over the last five years, the growth rate is much lower at less than 4% per year.

The dividend yield is also low at 1.4%, though this is ahead of the stock’s average yield of 0.9% since FY 2014.

The dividend appears to be well covered. The expected earnings payout ratio for FY 2024 is just 20%, which is lower than the five-year average of 28%.

It is a similar story with free cash flow. Over the last year, the free cash flow payout ratio checks in at a very reasonable 19%, which compares favorably to the average payout ratio of 24% of the four prior years.

Shareholders can rest easy that the dividend, though it may have muted growth that results in a low yield, is safe and supported by the business model.

Valuation and Total Return Potential

Shares of Maximus are trading at 14.3 times expected adjusted earnings-per-share for the fiscal year. The sector median is 18.8. Maximus’ five-year average is slightly ahead of the industry median at 19.1 times adjusted earnings-per-share.

I prefer to use recent business performance in conjunction with historical valuations to arrive at target valuation range for a potential investment. I believe a price-to-earnings ratio of 16 to 18 times earnings is appropriate for Maximus as this offers some measure of safety if results become weaker and cause the business to suffer or margins to drop once again.

The stock is not likely to trade within my valuation range over night. But looking out over the next five years or so, multiple expansion could add a low to mid-single-digit figure to total returns in the range of 2% to 4% annually. Combined with 7% annual earnings growth and the 1.4% dividend yield, total returns could be, at a minimum, more than 10% per year.

Risks to Investment Thesis

The primary risk facing Maximus would be its inability to win new contracts or to maintain its renewal rate. Winning and then maintaining these contracts is the lifeblood for Maximus. Without this, the business model would surely struggle.

Fortunately, the company has largely had the opposite experience, though the book-to-bill ratio did decrease on a sequential basis. There is the opportunity for future work as the pipeline remains robust.

Maximus also has a stellar track record in being able to renew most of its contracts with its customers. Such relationships take immense time to cultivate and clients are unlikely to switch providers if they are satisfied with the work. The nearly 90% renewal rate signifies that customers are at least satisfied with their partnership with Maximus.

Another issue would be that the company has seen its margins decline over the last five years as it has struggled to correlate revenue growth with earnings growth. That, however, has changed over the past fiscal year and the more recent earnings reports.

Finally, if either of these factors were to materialize, then the valuation would likely proceed lower than its current level.

Final Thoughts

Maximus’ most recent quarter showed that the business is seeing growth in its most important business areas. The company is trusted by customers, which is why they sign renewal agreements at an incredibly high rate.

These factors should enable the company to see sizeable improvements in the margins following a long period of decline.

The market doesn’t appear to have caught up to the improving business model, which is why the forward price-to-earnings ratio sits at a 25% discount to the medium-term average.

Investors can use this mispriced valuation, along with high single-digit earnings growth potential and a market beating yield, to generate annual returns in the low double-digits. Because of this potential return, I view Maximus as a hidden gem and believe shares are a buy today.

Read the full article here

")

")

")

")

(OTCMKTS:HESAF)")