")

")

Thesis

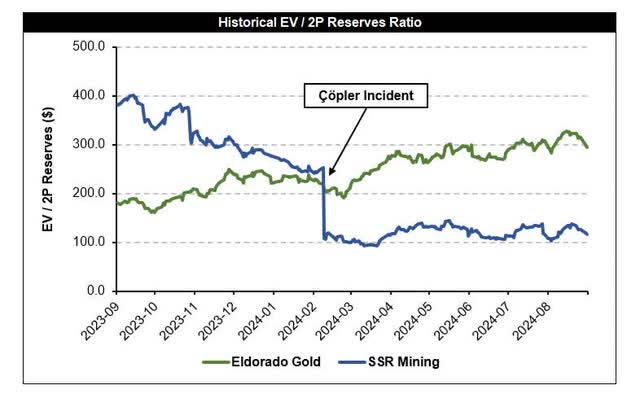

In February 2024, SSR Mining (NASDAQ:SSRM) suspended all operations at Çöpler following a significant slip on the oxide leach pad which accounted for roughly 11.0% of Çöpler’s total production in 2023. The share price fell by 53.5% on the announcement date and has been languishing since. The company’s enterprise value is now around $900 million or roughly equal to $122.6 per proven and probable gold ounce and that excludes the silver reserves located at Puna and other resources like those at Hod Maden for example. At the current valuation, I see Çöpler as a cheap call option and any positive news about processing the 706,000 ounces of gold contained in the sulphide stockpiles could act as an important catalyst.

As discussed in my latest article ”Eldorado Gold: All Eyes On Skouries”, Eldorado Gold (EGO) has proven and probable reserves of 11.7 million ounces of gold at an average grade of 1.04 g/t. Based on its current enterprise value of $3.4 billion, we are talking about a valuation of $300 per proven and probable ounce in the ground which is almost 150% higher than SSR’s valuation. Just prior to the Çöpler incident, both companies were trading roughly in line and if we go back to 2023, SSR was actually trading at a pretty large premium versus Eldorado. Both companies are mid-tier gold producers with four operating assets and with a significant proportion of their net asset value in Turkey. When it comes to grade, both portfolios are in the same ballpark at around 1.0 g/t.

After all, the 3.3 million ounces of proven and probable gold at Çöpler are still in the ground and the infrastructure is not only still in place, but the sulphide processing circuit that accounts for most of Çöpler’s production was undamaged. On top, SSR’s balance sheet was in a net cash position of $128.4 million at the end of Q2-24.

Historical EV/2P Reserves Ratio (Yahoo Finance, Author’s Calculations)

Description

SSR Mining is an intermediate gold producer with assets located in four jurisdictions consisting of the United States, Turkey, Canada and Argentina. Before 2017, the company was known as Silver Standard Resources, hence the name SSR today. The name change was introduced to better reflect the company’s evolution from a silver-focused explorer to a mid-tier precious metals’ producer.

SSR’s portfolio includes four producing assets including the Çöpler mine in Turkey, the Marigold mine in Nevada, the Seabee mine in Saskatchewan and the Puna mine in Argentina. SSR also announced in May 2023 the acquisition of operatorship and an up to 40% interest in the Hod Maden project which is a world-class gold and copper deposit with one of the lowest capital intensity in the industry. In a sense, Hod Maden is for SSR what Skouries is for Eldorado. The key difference is that Hod Maden is still early in its development schedule with Skouries is expected to declare first production in Q3-25.

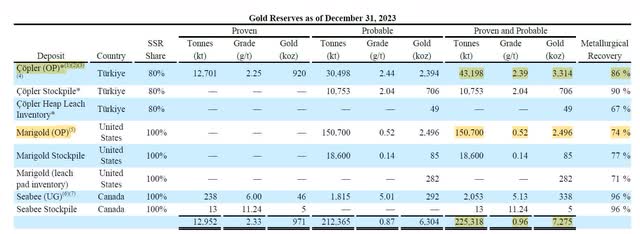

SSR’s portfolio is estimated to contain 7.3 million ounces of gold at an average grade of 0.96 g/t and 18.4 million ounces of silver at an average grade of 161.79 g/t. As indicated in the table below, Çöpler has been the cornerstone asset with proven and probable reserves of 3.3 million ounces of gold at an average grade of 2.39 g/t. As it has been the case for Çöpler, grades above 2.0 g/t for an open-pit mine are generally harbingers of success when it comes to free cash flow generation.

SSR Mining Reserves Estimate (2023 10-K)

Çöpler Heap Leach Pad Failure

Çöpler contains oxide and sulphide ores that were mined concurrently and processed through two separate processing circuits. Gold contained in oxide ore was recovered through heap leach processing to produce gold doré with a minor by-product of copper concentrate. Gold sulphide mineralization was subjected to pressure oxidation and carbon-in-leach processing to produce gold doré. SSR Mining owns 80% of Çöpler through a joint venture.

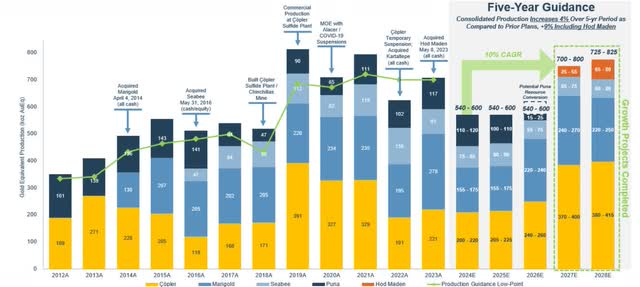

Before the leach pad failure, SSR Mining released long-term production guidance including the contribution from Çöpler. As indicated in the chart below, Çöpler was expected to produce 210,000 ounces of gold equivalent or 36.8% of the company’s total production of 570,000 ounces of gold equivalent.

According to the latest mineral reserves estimate, Çöpler also represented 45.5% of total proven and probable gold reserves. With all-in sustaining costs per ounce that were estimated at $1,570 for 2024 and low sustaining capital requirements, Çöpler has been the key free cash flow producing asset in SSR’s portfolio. Since the incident, all production activities have been stopped and no revenues have been recorded since.

Historical Çöpler Contribution (February 13, 2024 Press Release)

The first element to note is that the sulphide process plant was not impacted by the incident and that it would not require any major repair work before resuming operations.

Second, as indicated in the most recent reserves estimate, there are approximately 706,000 ounces of gold contained in the sulphide stockpiles. While the containment and remediation activities are expected to last over a period of 24 to 36 months, the company could potentially process the sulphide stockpile and generate some cash to offset the remediation costs estimated between $250.0 and $300.0 million.

The sulfide process plant commenced commissioning in the fourth quarter of 2018. The sulfide process plant was not impacted by the Çöpler Incident. The facilities are operational, but have been suspended. If the Company is permitted to resume operations at Çöpler, it does not appear at this time that the sulfide plant would require repair work to be operational. 2023 Annual Report

Third, although the company confirmed that the leach pad will be permanently closed and that heap leach processing will no longer take place at Çöpler, the oxide heap leach pad represented only 11.0% of Çöpler’s production in 2023.

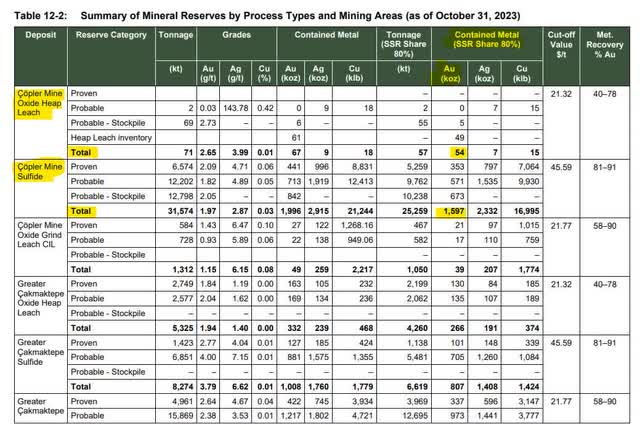

As indicated in the table below, most of Çöpler’s economic value resides in the sulphide ore and in the Çakmaktepe extension. Closing permanently the heap leach pad used to process oxide ores does not mean that it is game over for the mine.

The detailed mineralogical analysis confirms that the gold is primarily carried by sulfide minerals. In the calculated head, 83% of all gold is in sulfides and only 2.4% was held in rock. The remainder of the gold was present as free gold, and this correlates well with a direct cyanidation recovery of only 17% when the ore was ground to a P80 of 90 µm. Technical Report Summary on the Çöpler Property

Çöpler Mineral Reserves by Process Types (Technical Report Summary on the Çöpler Property)

Balance Sheet

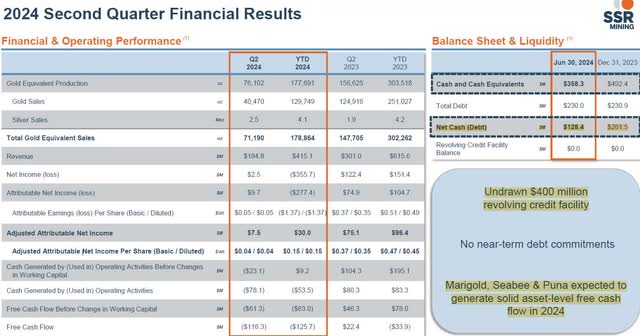

With $358.3 million of cash sitting on the balance sheet at the end of the second quarter of 2024 and total debt of $230.0 million, SSR Mining currently has a net cash position of $128.4 million. On top, the company has access to an undrawn revolving credit facility of $400.0 million. Although Çöpler is not generating any revenue at the moment, Marigold, Seabee and Puna will continue to generate healthy free cash flow in the years to come.

With a balance sheet in a net cash position and more than 700,000 ounces of gold sitting in the sulphide stockpile at Çöpler, the company should be able to meet the upcoming remediation and reclamation costs.

Balance Sheet (Q2-24 Presentation)

Valuation

The Marigold, Seabee and Puna mines are not dependent on cash flows or operational synergies associated with Çöpler. Consequently, the worst-case scenario is the permanent closure of Çöpler and the loss of the associated 3.3 million ounces of proven and probable reserves. When it comes to the remediation costs estimated between $250.0 and $300.0 million, I believe they could be offset by processing the sulphide stockpile as the material has been mined already.

Without Çöpler, SSR Mining would have proven and probable reserves of approximately 4.0 million ounces. Based on the current enterprise value of approximately $900 million, we would be talking about a valuation of $223.0 per proven and probable ounce or roughly in line with the valuation of other mid-tier gold producers including Eldorado Gold.

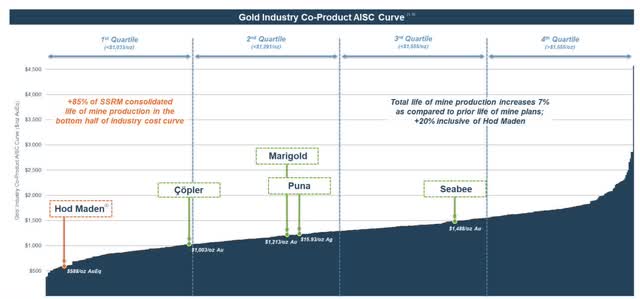

Although the all-in sustaining costs at Marigold, Seabee and Puna are a little bit higher than those at Çöpler, they still are in the bottom half of the industry cost curve. Moreover, Hod Maden is a world-class gold and copper deposit representing one of the highest margin and lowest capital intensity development assets in the industry. The company aims for a full construction decision in 2024 with the goal of reaching first production in 2027.

In my view, the probability of the worst-case scenario materializing is low. Although some challenges may arise with permitting and environmental licences, I do not believe that Turkey will decide to leave 3.3 million ounces of proven and probable ounces in the ground especially with the infrastructure already in place and an undamaged sulphide processing plant.

Gold Industry AISC Versus SSR Assets (February 2024 Presentation)

With a share price of around $5.00, SSR is trading at $122.57 per proven and probable ounce which is by far the lowest among the intermediate gold producers that I follow. On top, the company has ample liquidity with $128.4 million of net cash on the balance sheet and an undrawn revolving credit facility of $400.0 million. Even if we completely exclude the proven and probable reserves at Çöpler, SSR would still be trading at only $222.93 per proven and probable ounce, so just above Equinox Gold (EQX) and below IAMGOLD (IAG).

EV/2P Reserves Ratio – Intermediate Gold Producers (Author’s Calculation)

Risk Factors

Similar to Eldorado, one key risk to keep in mind when it comes to SSR is Turkey. On top of the operational risks at Çöpler, there is another layer of jurisdictional risks especially since Turkey applied for membership in the BRICS last week. Moreover, President Tayyip Erdogan said on Saturday that Islamic countries should form an alliance against Israel. The relationship between Turkey and other Western countries could be taking a turn for the worse and Western investors could be caught in the middle.

Çöpler is obviously the company’s biggest exposure to Turkey, but Hod Madden, which is SSR’s key development project, is also exposed. One key difference between those two assets is that Hod Madden is located in the eastern portion of the country and close to the border with Iran while Çöpler is more insulated as the mine is in the middle portion of the country. In short, geopolitical risks are real when it comes to SSR and investors should include this factor in their valuation work.

Moreover, there is also the risk of a certain contagion between Çöpler and Hod Madden, and by contagion, I mean delays or difficulties in obtaining construction permits or environmental licenses. If there is any indication in the future that it might indeed be the case, the market could then apply an additional discount to Hod Madden’s net asset value.

Conclusion

The opportunity resides in the fact that market participants have basically written-off Çöpler’s net asset value while a few elements indicate that the game might not be over and that the mine could recover in the medium to long-term.

Most of the economic value at Çöpler is located in the sulphide ore and in the Çakmaktepe extension. The sulphide processing plant did not suffer damage and could be restarted without major repair work. Moreover, there are more than 700,000 ounces of gold in the sulphide stockpile that is waiting to be processed. The cash flow generated from the stockpile could be used to meet the reclamation costs estimated at $300.0 million in the upper range. The situation at Çöpler does not have any impact on the other producing assets and it does not change the fact that Hod Maden is a world-class gold and copper project.

Çöpler should be seen as a call option as the issues with the leach pad are well-known and are reflected in the valuation multiples. Although the leach pad failure at Çöpler is serious in nature, I believe that SSR will be able to recover from it. Any major development when it comes to processing the sulphide stockpile could act as an important catalyst.

I will continue to monitor the situation at Çöpler closely and assuming that it does not worsen any further, I may press the trigger if the share price retests the important support line at $4.00 per share. Despite the compelling valuation, patience is a virtue and I am now on the lookout for a technical window of opportunity.

SSR Mining Share Price (Author’s Graph)

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here

")

")

")

")

(OTCMKTS:HESAF)")

")

")