")

")

It has been nearly a year and a half since we last looked at medical diagnostic concern OraSure Technologies, Inc. (OSUR). At that time, the company had seen a massive surge of COVID-19 test-related revenues. We concluded the initial article on the diagnostic firm by stating the stock was an “avoid.” It was difficult to ascertain how the company would fare in a post-COVID future. 18 months later, it is time to circle back to OraSure Technologies. An updated analysis follows below.

Seeking Alpha

OraSure Technologies is headquartered in Bethlehem, PA. The company provides point-of-care and home diagnostic tests, specimen collection devices, and microbiome laboratory and analytical services. During the pandemic and its aftermath, OraSure’s saw large demand for its various COVID tests, including the InteliSwab COVID-19 rapid test and the rapid test pro. OraSure also has tests for HIV, a saliva alcohol test, immunology, drug testing and other diagnostic services. The company’s core business (non-COVID) is broken down to two business segments: Diagnostics and Molecular Sample Management. The stock currently trades around $4.25 a share and sports an approximate market capitalization of just north of $310 million.

Recent Results:

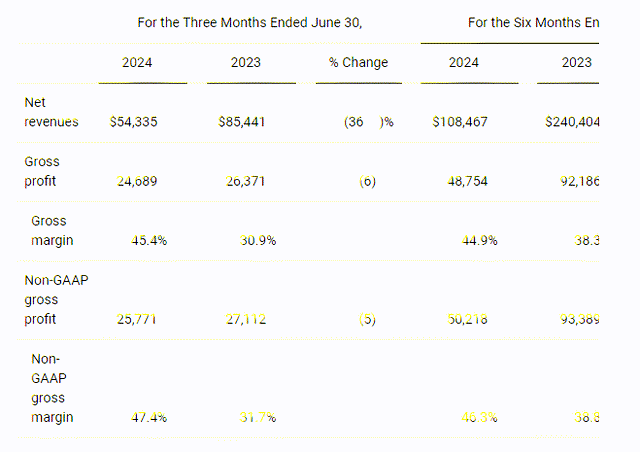

The company posted its Q2 numbers on August 6th. OraSure delivered a non-GAAP profit of 7 cents a share, four pennies a share above expectations. OraSure had non-GAAP net income of $3.3 million for the quarter, compared to a non-GAAP loss of $2 million. As can be seen below, the best part of the quarter was the margin improvement that OraSure delivered. Margins benefited from operational efficiency initiatives and lower manufacturing scrap expense.

Q2 Press Release – Courtesy of Seeking Alpha

Revenues did fall just over 36% on a year-over-year basis to just over $54.3 million. However, this was some $2 million above the consensus. That said, sales numbers were hardly encouraging for longer-term shareholders.

Q2 Press Release – Courtesy of Seeking Alpha

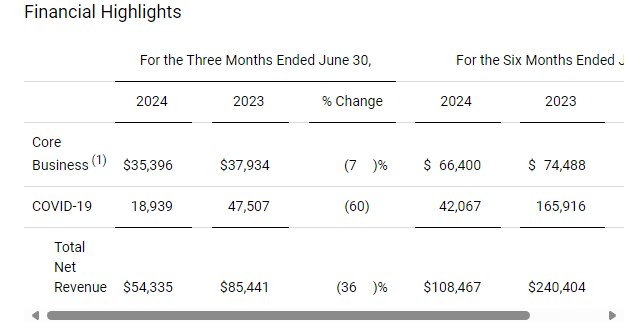

As can be seen above, COVID related testing sales fell 60% to just under $19 million as contracts expired. That was largely expected. However, the company is not seeing any growth in non-COVID or “core” testing revenues. In fact, they fell seven percent from the same period a year ago to $35.4 million. Diagnostic revenues were off five percent from Q2 2023 while Molecular Sample Management were off three percent. The company is also exiting a small business that was part of the latter.

Analyst Commentary & Balance Sheet:

The analyst community is still not positive about OraSure’s post COVID future. Since mid-May, Jefferies ($6 price target, down from $7 previously), Evercore ISI ($4.50 price target, down from $5.50 previously) and JPMorgan ($5 price target) have reissued Hold ratings on the stock. I can find no analyst firm Buy ratings on OraSure so far, here in 2024.

OraSure Technologies ended the first half of 2024 with just over $265 million worth of cash and marketable securities on its balance sheet. The company had positive operating cash flow of $7.8 million during the second quarter. Management has stated the core part of the business will be breakeven on an operating cash flow basis by year-end as well. The company listed no long-term debt on the 10-Q it filed for the second quarter. There has been no insider activity in the shares so far in 2024. Approximately three percent of the outstanding float in the shares is currently held short.

Conclusion:

OraSure made 72 cents a share in FY2023 on $405 million in revenues. The current analyst firm consensus has OraSure moving into the red to a tune of a 19 cent a share loss in FY2024 as sales get cut by more than half to just over $186 million. They project losses of 21 cents a share in FY2025 on a continued sales decline of 15%.

The good news is that OraSure has plenty of cash on its balance sheet. It is probably the most attractive part of this company’s investment thesis currently, accounting for nearly 90% of its market cap. The bad news is OraSure looks like it will be unprofitable for many years as the company is currently constituted. COVID-related sales will eventually fall to near nil, unless there is another pandemic. In addition, core sales growth is non-existent at the moment. Management has done a commendable job of lowering operational expenses and improving margins. This should mean minimal losses while overall sales continue to decline at least through FY2025.

However, until OraSure Technologies, Inc. can start delivering core sales growth again either organically or via “bolt on” acquisitions, the stock is probably range bound at best. Therefore, there is no reason to take a position in OSUR until those dynamics change.

Fulgent Genetics (FLGT) is a diagnostic concern with a similar post COVID dilemma and is also sitting on a huge cash balance. I wrote this name up in June and have a small position in it. The main differences are; core sales growth is returning at Fulgent and the options against the equity offer decent liquidity. This means I can hold FLGT within a covered call position. Therefore, it is a superior investment proposition in my opinion.

Read the full article here

")

")

(OTCMKTS:HESAF)")

")

")

Game Recap")