")

")

")

Investment Overview

The last – and also the first – time I covered Supernus Pharmaceuticals (NASDAQ:SUPN) for Seeking Alpha was in November 2023. I gave the company’s stock a “strong buy” rating – shares traded at $26 at the time – and at the time of writing they trade at a value of $30 – up ~15%. I own some stock in the company myself.

At the end of last week, shares actually traded at $35 per share – up 35% since my note – however the market has been selling off the stock today, apparently in response to a rating downgrade from analysts at Piper Sandler, from overweight, to neutral.

For a full history of Supernus and its business I’ll refer readers to my previous note which provides a fairly comprehensive overview, however let’s quickly remind ourselves of the nature of Rockville, Maryland based Supernus’ business – as per the company’s Q2 2024 quarterly report / 10Q submission:

Our diverse neuroscience portfolio includes approved treatments for epilepsy, migraine, attention-deficit hyperactivity disorder (ADHD), hypomobility in Parkinson’s Disease (PD), cervical dystonia, chronic sialorrhea, and dyskinesia in PD patients receiving levodopa-based therapy. We are developing a broad range of novel CNS product candidates including new potential treatments for hypomobility in PD, epilepsy, depression, and other CNS disorders.

Here is a quick overview of currently approved drugs:

- Qelbree (viloxazine) – novel non-stimulant product indicated for the treatment of ADHD in adults and pediatric patients;

- GOCOVRI (amantadine) – extended release capsules – first and only FDA approved medicine indicated for the treatment of dyskinesia in patients with PD receiving levodopa-based therapy;

- Oxtellar XR (oxcarbazepine) – therapy for the treatment of partial onset seizures in patients 6 years of age and older;

- Trokendi XR (topiramate) – extended-release topiramate product indicated for the treatment of epilepsy in patients 6 years of age and older;

- APOKYN (apomorphine hydrochloride injection) – indicated for the acute, intermittent treatment of hypomobility;

- XADAGO (safinamide) – adjunctive treatment to levodopa/carbidopa in patients with Parkinson’s Disease (“PD”);

- MYOBLOC (rimabotulinumtoxinB injection) – a product indicated for the treatment of cervical dystonia and chronic sialorrhea in adults. It is the only botulinum toxin type B available on the market.

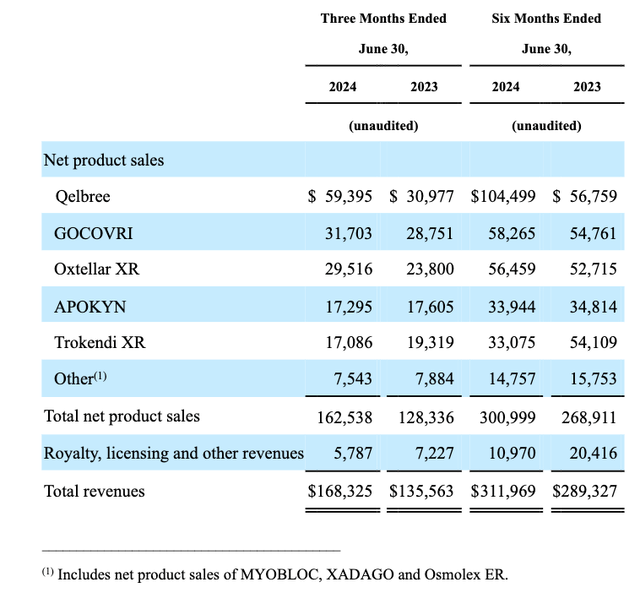

And, here is a quick overview of net product sales across Q2 2024, and 1H 2024:

Supernus product revenues overview (Q2 2024 10Q)

Piper’s analysts concerns related to Supernus’ best-selling asset, Qelbree – according to Seeking Alpha:

Analyst David Amsellem revised his projection for Qelbree’s peak sales potential to $400M from $500M, arguing that Piper’s expectations for an uptick in prescription ((Rx)) growth have yet to materialize.

Citing Iqvia (IQV) data, Amsellem pointed out that quarter-to-date Qelbree Rx growth has slowed, reaching ~1% in Q3 2024 from the corresponding period in Q2 2024.

Notably, Q2 2024 sequential growth for RX stood at ~4%, while the YTD Rxs for the drug showed ~25% YoY growth from a 91% YoY growth last year.

The suggestion is that Qelbree sales growth will be “less than aggressive going forward” – should Supernus shareholders be worried, or conversely, could this be the right time to add to your position, or open one?

Analysis – Is Slowing Growth Of Qelbree Revenues A Cause For Concern? I’m Not So Sure

Trokendi lost its patent protection in 2023, which explains why its revenues are falling – from $54m to $33m in 1H24 – and from $261m in 2022, to $94m in 2023. Oxtellar’s patents expire this year, and generic competition will enter the marketplace from September, it’s estimated, so the company is undoubtedly becoming more reliant on the success of Qelbree.

On its Q2 2024 earnings call with analysts, Supernus’ Chief Financial Officer (“CFO”) Tim dec provided the following full-year guidance for 2024:

We expect total revenue to range from $600 million to $625 million, up from the previous range of $580 million to $620 million, comprised of net product sales, royalties, licensing and other revenue.

For the full year 2024, we expect combined R&D and SG&A expenses to range from $430 million to $460 million. Overall, we expect full year 2024 GAAP operating earnings to range from breakeven to $20 million, and non-GAAP operating earnings to range from $100 million to $125 million.

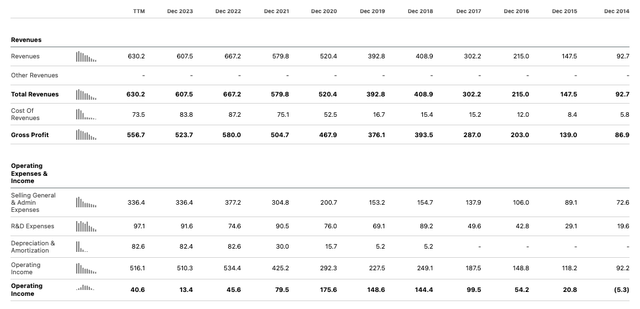

Let’s quickly compare these figure to previous years for Supernus:

Supernus – annual income statements (Seeking Alpha)

On a GAAP basis, at least, 2024 will continue the trend of falling net income – from $145m, $149m, and $176m between 2018 – 2020, to $46m, and then $13.4m in the past two years. Seeking Alpha suggests operating income will be $41m in 2024, but management’s guidance suggest it may be 50% lower.

Supernus reported cash and investments of $347m as of Q2, and no long term debt, so the company is in a reasonably strong position financially, but what about the future of Qelbree?

The majority of prescriptions for ADHD appear to be pediatric – 67% according to a recent corporate presentation – could it therefore be that prescriptions were slow in Q3 because children were out of school? This is only a thesis, however, on the recent earnings call Jack Khattar, Supernus’ long-time CEO did states, in response to an analyst’s question:

as far as the back-to-school programs, I mean, it’s fairly intense as far as the level of support that we will be going out with and the momentum that we will be building and are building actually as we speak right now in preparation for the back-to-school season. So we will put a lot of investment and effort behind this season, given the importance of the season for the whole year, for the brand in general.

Apparently, the consensus is that Qelbree will drive somewhere in the region of $200m – $220m revenues in 2024, and the CEO suggested “it all depends on the back-to-school season”.

He also admitted that the back-to-school period was “soft” in 2023, but the point is that sales of Qelbree may follow seasonal patterns, and therefore, one slow quarter of growth may be giving false impression.

Qelbree revenues in 2023 were $140m, so if Supernus hits $210m in 2024, the annual growth of 50% would hardly be a disappointment, and in fact, Piper’s revised peak revenue figure of ~$400m per annum is substantially higher than the peak sales achieved by former lead drug Trokendi.

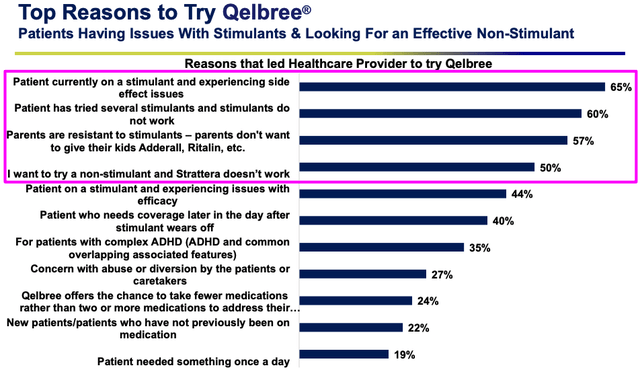

Supernus says it has a sales force of 245 dedicated to growing revenues for Qelbree, and as a non-stimulant, the drug has the ability to attract new patients for a variety of different reasons, as shown below:

Qelbree switching analysis (Supernus presentation)

Grand View Research estimates the global ADHD market to be worth nearly $15bn per annum, but to be conservative, let’s revise that figure down to $7.5bn for the US market only, which implies Qelbree needs a <7% market share in order to hit peak revenues of $500m per annum. In its 2023 annual report / 10K submission Supernus notes:

Competition in the U.S. ADHD market has increased with the commercial launch of several branded products in recent years, as well as the launch of generic versions of branded drugs, such as Adderall XR, Concerta, Vyvanse, Intuniv, Kapvay and Strattera.

Nevertheless, as a non-stimulant alternative to mainstream brands, a ~7% market share feels achievable.

Pipeline Opportunities May Be More Relevant To Future Valuation Than Qelbree Peak Revenue Figure

We should also note that Supernus has several mid-to-late-stage pipeline opportunities in attractive markets, which management believes can help the company “build a multi-billion dollar CNS franchise”, by unlocking multi-billion dollar markets.

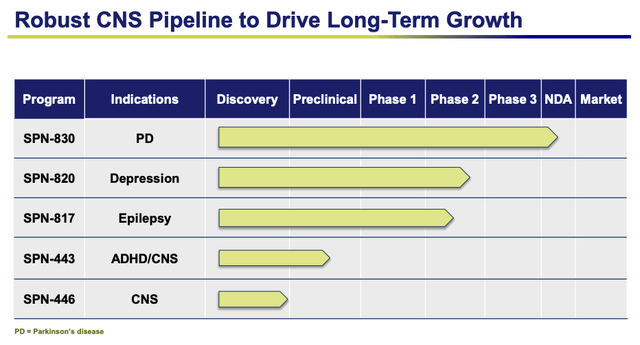

Here is an overview of the company’s pipeline:

Supernus – late stage pipeline (presentation)

I discussed these in my last note also, but let’s revisit the three later stage opportunities.

SPN-830 is an apomorphine infusion device for the continuous treatment of motor fluctuations in Parkinson’s Disease (“PD”).

The device has been rejected for commercial approval by the FDA on two previous occasions, most recently in April this year, in relation to “product quality issues, but on the Q2 earnings call, CEO Khattar advised that:

Regarding SPN-830, we resubmitted the NDA last week and expect to learn from the FDA in a few weeks, whether this submission will be considered as a Class 1 requiring a two month’s review or a Class 2 requiring a six month’s review. We remain committed to Parkinson’s patients who need this potential new treatment option.

Peak sales for SPN-830 have been estimated at $200 – $300m, so despite the frustrating delays, it’s ability to contribute to Supernus’ top-line going forward should not be dismissed yet.

SPN-820 targets a substantial market – Major Depressive Disorder, and it is an “orally active small molecule that increases the brain mechanistic target of rapamycin complex 1 (mTORC1) mediated synaptic function intracellularly”.

MDD is a crowded market with >60 approved therapies, but its also a 17m patient market. Supernus says it “expects to provide data from its Phase 2b study in adults with treatment-resistant depression in the first half of 2025”, which constitutes a major potential upside catalyst for shareholders.

Data was originally promised for 2024, and whether the study will meet its required efficacy bar is uncertain – conclusions from a prior study were that:

efficacy with HAM-D6 shows early, large effect size, sustained to 72 hours after single dose

However, on the negative side:

MADRS (Montgomery–Åsberg Depression Rating Scale) did not show efficacy with single dose but showed small effect on acute symptoms

CNS drugs often miss endpoints in my experience, as questionnaires can be subjective and deliver mixed results, so this is a tough outcome to call, but in my view, the impact of a study win is not being priced into Supernus ~$1.7bn market cap valuation at present, so I’d speculate there is more upside in play than downside.

Finally, Huperzine A, or SPN-817, is “a potent, selective and reversible acetylcholinesterase (AChE) inhibitor, an enzyme that metabolizes acetylcholine (ACh) after synaptic release”.

A Phase 2a open label (no placebo arm) study in patients with treatment-resistant seizures delivered mixed results in May, with a 22% discontinuation rate in the titration period, but only 2.4% in the maintenance period, and 58% median seizure reduction in the maintenance period, and 38% median seizure reduction in the open label extension period.

Concluding Thoughts – A Mixed Outlook For Supernus Is Typical Of CNS Focused Companies – I Remain Bullish

Shortly after the SPN-817 Phase 2a data were shared, Supernus sank to a share price low of ~$25 per share, but the company’s Q2 earnings and uplifted guidance drove a bull run that saw the share price achieve its highest value for over a year.

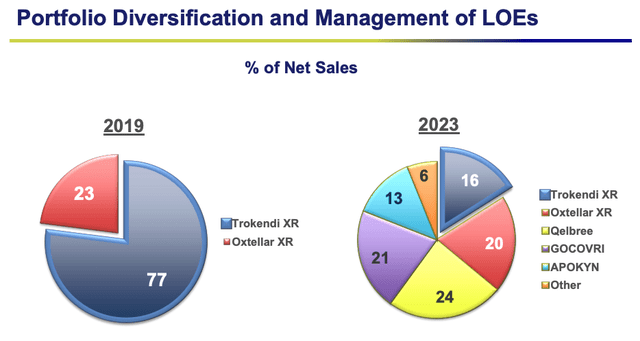

The reality is that developing drugs for CNS conditions can be an unforgiving and unpredictable industry, and Supernus has had to deal with patent expiries for its best-selling drugs to boot.

Supernus copes with LOEs (presentation)

Nevertheless, as we can see above, Supernus has coped with threats to its business exceptionally well, using strategic acquisitions and its own R&D to navigate patent expiries successfully, and emerge with, if anything, a stronger looking portfolio.

In my view, despite some evident risks to the bull thesis – potentially plateauing growth for Qelbree, doubts around the success of late-stage of pipeline products – the market seems to be valuing Supernus as if the negatives outweigh the positives, when my contention is the opposite may be true.

The MDD readout for SPN-820 due next year is a critical catalyst, and the fate of SPN-830 also important. It’s easy to forget Supernus is valued at just ~3x forward revenues, and will be profitable in 2024, by a triple-figure sum on a non-GAAP basis. Falling sales of Oxtellar and Trokendi will continue to weigh on the valuation, but the upside from a successful MDD data readout would likely be a far greater catalyst for upside, and an eventual approval SPN-830 would offset the lost revenues long-term.

Investing in any CNS company will inevitably be fraught with potential pitfalls, but I’m keeping the faith with Supernus – even if the late-stage pipeline does not succeed, management’s ability to make strategic M&A deals should not be ignored.

Read the full article here

")

")

")

")