")

Business development companies (BDCs) are unique entities aiming to fill the financing gap for businesses struggling to acquire bank or public financing. Therefore, BDCs typically concentrate on the smaller and middle-market companies (often lower middle-market).

The business model is pretty simple to understand – gather financing sources (mainly equity) and deploy the capital to generate favourable investment spreads.

Most BDCs are externally managed. There aren’t many internally managed ones; they come with attractive features over externally managed BDCs. As one of the most popular BDCs among investors, internally managed MAIN Street Capital (MAIN) stated:

Because we are internally managed, we do not pay any external investment advisory fees, but instead directly incur the operating costs associated with employing investment and portfolio management professionals. We believe that our internally managed structure provides us with a better alignment of interests between our management team and our employees and our shareholders and a beneficial operating expense structure when compared to other publicly traded and privately held investment firms which are externally managed, and our internally managed structure allows us the opportunity to leverage our noninterest operating expenses as we grow…

If you are a fan of internally managed BDCs, you can diversify away from MAIN through another top-tier market player – Capital Southwest (NASDAQ:CSWC). CSWC typically invests in secured debt and equity of its portfolio companies that can generally be considered low middle-market entities with EBITDA ranging from $3m to $25m. CSWC’s tickets (investment size) typically range from $5m to $35m.

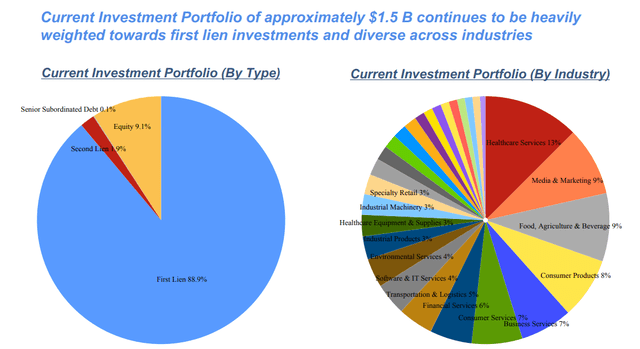

CSWC has a well-diversified portfolio across different sectors. Its ~$1.5B portfolio value is heavily influenced by relatively safe first-lien debt investments (88.9%), with another 9.1% invested in equity, 1.9% in second-lien debt, and 0.1% in senior subordinated debt.

CSWC Investor Presentation

Volatility Lurks Behind The Corner

Non-accruals already reflect a tough market environment

According to expectations, non-accruals have typically been rising across the BDC sector. However, CSWC recorded lower non-accruals at fair value as of June 2024 (1.9%) compared to March 2024 (2.3%) and the same level of 3.9% at cost.

While there are BDCs with more defensive portfolio structures and noticeably lower non-accruals (with Blackstone Secured Lending (BXSL) leading the way), such a stable performance still implies the high quality of CSWC’s investments, as many other players recorded rising non-accruals, according to expectations stated by Ares Capital’s (ARCC) management during its Q4 2023 Earnings Call:

We’ve said this in the past that we’re likely to see defaults in the industry just increased this year. It does take a little bit of time for that to manifest itself, right? So in the bottom quartile of our portfolio and probably everybody else is, you have some companies that are making interest payments but continue to live off revolver availability, cash, et cetera, but the liquidity is getting tighter and tighter.

And so my expectation is that the fall will go up this year, probably more towards the historical norm. We’ve had a little bit of amendment activity that’s elevated; I think others probably have two but nothing that’s causing us a whole lot of concern. I think it’s just a regular letting out as obviously rates are higher and companies have higher debt service costs and all that. But generally, I think we’ll see that as well others.

Given that precisely presented outlook, we may still expect higher non-accruals in the upcoming quarters.

Interest rate environment is a double-edged sword, but it will likely lead to higher volatility

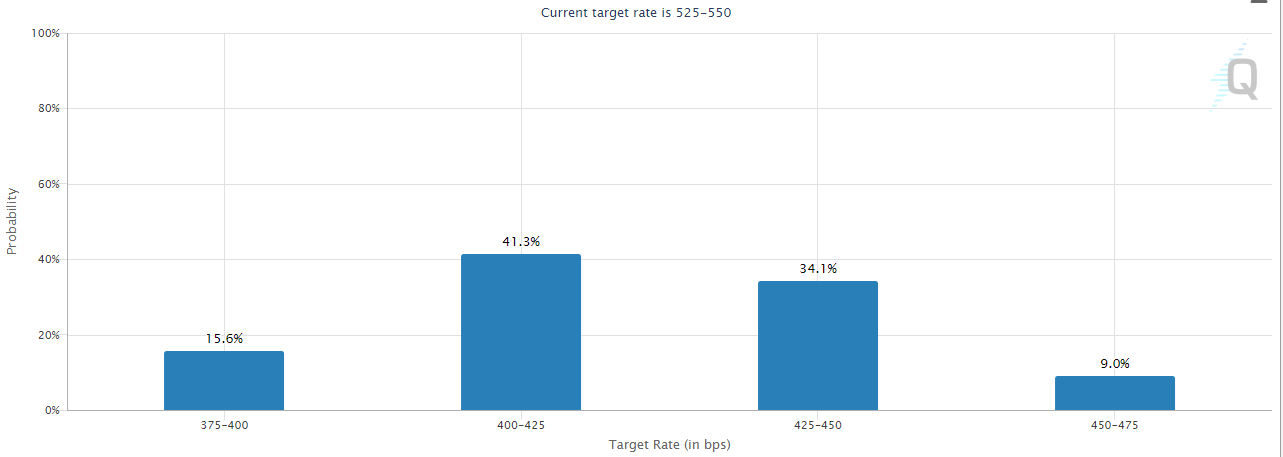

With the market currently expecting substantial interest rate cuts in the upcoming months, many investors are concerned with the performance of their BDC investments.

CME Group

There are a few aspects to consider while analysing the potential impact of interest rate cuts on CSWC’s performance.

Firstly, let’s start with the point that is hard to quantify. Rising interest rates led to a significant widening of the gap between buyers and sellers, as well as borrowers and lenders, expectations, resulting in a relatively dormant transactional market. With potential interest rate cuts, improving liquidity and access to capital, we may see a turnaround in this area, improving BDCs’ capabilities to source attractive capital deployment opportunities.

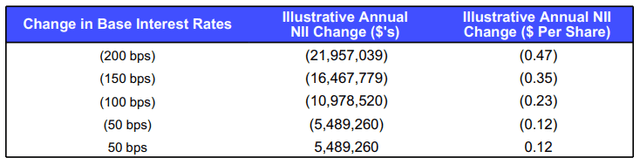

Secondly, while MAIN benefits from a significant portion of its debt investments structured with fixed rates, CSWC doesn’t have such an advantage, as 97.6% of its floating portfolio has a floating rate. Therefore, the Company may expect lower investment income with lower interest rates, and CSWC presented us with its estimation of the impact of the monetary policy on its financial stance.

CSWC Investor Presentation

On the other hand, the Company may secure more favourable equity exits/dividend proceeds due to higher liquidity and better valuations.

Lastly, a lower interest rate environment will positively impact CSWC’s debt cost, somewhat offsetting its negative impact on its investment income. That’s because some portion of CSWC’s debt is floating-rated.

CSWC Investor Presentation

Regardless of the above facts, I am a huge fan of Benjamin Graham’s Mr. Market metaphor, stating that the market is irrational and often presents us with opportunities for overvalued and undervalued businesses. Mr. Market is highly emotional and will likely react to the interest rate cuts, punishing already ‘weak’ BDCs and the top-tier players that CSWC undoubtedly is.

Therefore, I expect noticeably better entry levels to be possible for investors willing to build positions in CSWC in the upcoming quarters.

Valuation Outlook

As an M&A advisor, I usually rely on a multiple valuation method that is a leading tool in transaction processes, as it allows for accessible and market-driven benchmarking.

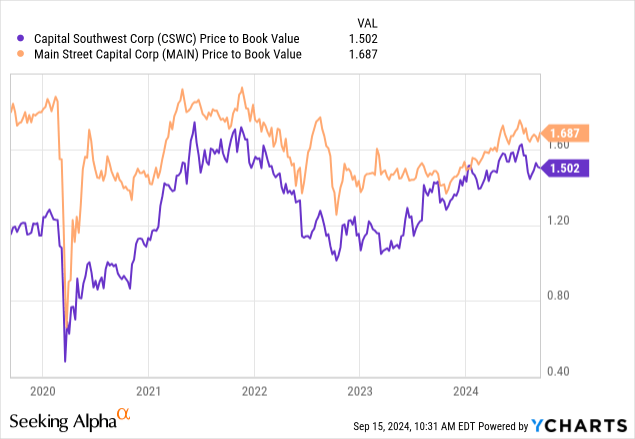

As we have a BDC on the table, let’s look at its P/BV ratio. For comparison, I’ve also included MAIN.

Both entities have a solid track record of trading with a premium to NAV. While MAIN’s premium is substantially more prominent, I can also see why it’s justified, as MAIN is better prepared for the upcoming interest rate cuts (through its high share of fixed-rated debt investments).

As mentioned before, I believe that CSWC will present us with better entry points in the upcoming quarter as Mr. Market is volatile due to a rapidly changing market environment, featuring monetary easing and potentially rising non-accruals.

Investment Thesis and Risk Factors

Each stock market investment is accompanied by market and company-specific risk factors, which in the case of CSWC include:

- Interest rate uncertainty

- Risk of rising non-accruals

- Upcoming stock price volatility

- Risk of upholding and further growing dividend payments

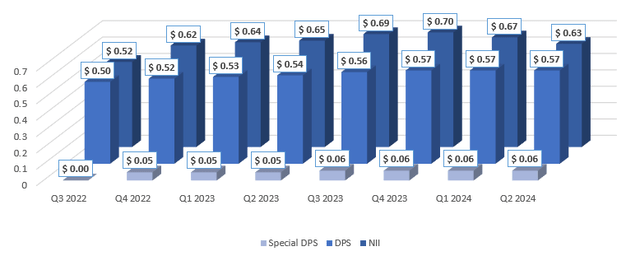

Regarding the last point, I believe CSWC showcases reasonable regular dividend coverage. The Company will likely uphold its regular dividend payments unless interest rate cuts are more rapid than everybody expected.

Please review the chart below for more details.

Author based on CSWC

To summarize, I consider CSWC one of the top-tier BDCs – let there be no doubt about that. So far, I’ve been able to build positions at a 20-30% premium to NAV at most, so I will take my chances and wait until I add more to my already existing CSWC position, as the 50% premium is well above my current average cost.

Don’t get me wrong, there’s nothing wrong with BDCs trading at a premium. On the contrary, the higher the premium, the lower their cost of equity, which facilitates their ability to gather proceeds in a more accretive manner.

However, the upcoming quarters should give investors many opportunities to establish positions at more favourable entry points, which I consider a strategy worth the patience. I’m a big advocate of Benjamin Graham’s margin of safety, so CSWC is a ‘hold’ for me. Thank you!

Read the full article here

Q4 2024 Earnings Call Transcript")

")

")

")