Thesis

With the front end of the yield curve higher in the past year, short duration instruments have become appealing across asset classes. To that end, it is worth revisiting the Eaton Vance Short Duration Diversified Income Fund (NYSE:EVG), a fixed income CEF covered more than two years ago. At the time of the initial article on the name, we highlighted for readers why the fund did not make sense at the time, having a very high, unsupported yield, with a high ROC (‘return of capital’) distribution.

Higher yields have translated into higher cash flows for the EVG components, and while other multi-asset funds have rocketed at premiums to NAV, this fixed income CEF is still trading at a discount, despite a substantial improvement in its analytics and cash flows. In this article, we are going to re-visit the name and highlight for investors why today’s environment is a sensible one to take a long position in this CEF.

Low duration collateral composition

The fund has a very low 2.5 years duration achieved via holding floating-rate leveraged loans and low duration MBS bonds:

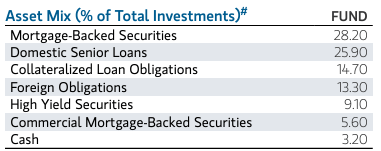

Asset Mix (Fund Fact Sheet)

Mortgage Backed Securities compose 28.2% of the portfolio, followed by leveraged loans at 25.9% and CLOs at 14.7%. To note EVG is a multi-asset fund via its composition, holding small sleeves of international bonds, U.S. high yield, and CMBS securities.

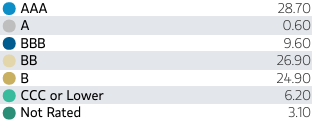

The majority of the MBS securities are AAA-rated, thus being mainly driven by rates:

Ratings (Fund Fact Sheet)

The fund manages to balance out its credit-risky names which fall in the double-BB and single-B buckets with AAA MBS bonds. Given the high current Fed Funds and improvement in yields at the front end of the curve, the vehicle runs very little leverage currently, leverage which stands at only 14%.

To note that the market is implying three Fed cuts this year, and we will finally have a balance between lower rates and higher credit spreads. We fully expect risk-off environments in the later half of the year to be marked by lower risk-free rates when credit spreads move higher, which will see the fund balance out via its composition.

Overdistribution was an issue in the past

In a low rates environment this fund was overdistributing, but things have improved tremendously:

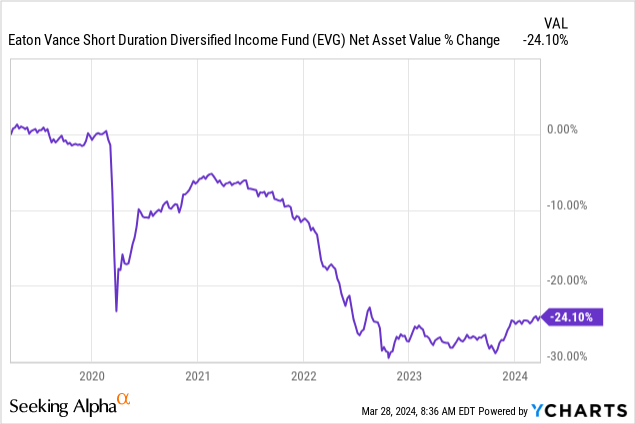

As exemplified by its NAV performance, the fund has finally found its footing in the past year. From a pure cash flow perspective, this makes sense since leveraged loans yield 8% to 9%, while MBS bonds with 14% leverage should provide for cash-flows in excess of, 6%.

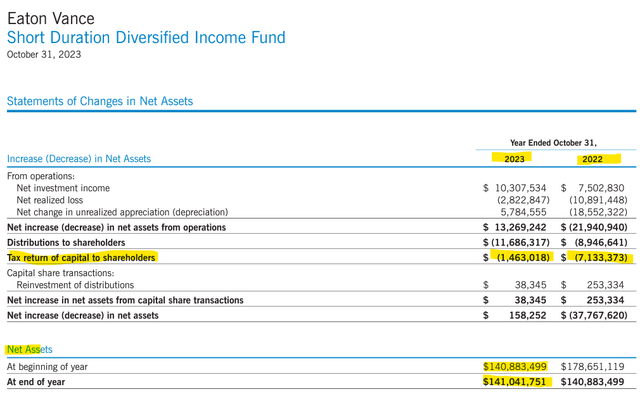

While the fund does not provide for a Section 19a notice publicly, we can look at its Annual Report to get the same information:

ROC (Annual Report)

We can see the CEF having decreased by 6x its ROC utilization in 2023 versus the prior year, with the respective line moving from $7.1 mm to $1.4 mm. More importantly, the low ROC utilization plus the correct asset management of the fund resulted in an accreting NAV for 2023. If we look at Net Assets at the beginning and end of 2023 we can see they are almost the same (with a slight positive accretion actually). This is the sign of a healthy CEF that distributes the cash it makes but keeps a steady NAV.

These are exactly the types of metrics you want to see as an investor. You want a stable NAV and a high yield with a low volatility metric.

No better time for EVG

Historically there is no better time to buy EVG. The fund is finally distributing what it is making thanks to the high interest rate environment, and via its composition, it will blunt some of the impact of lower Fed Funds later in the year. The CEF was plagued by overdistribution in the past but has moved to a stable NAV. We expect this state of affairs to persist for the next two years until Fed Funds move below 3% again.

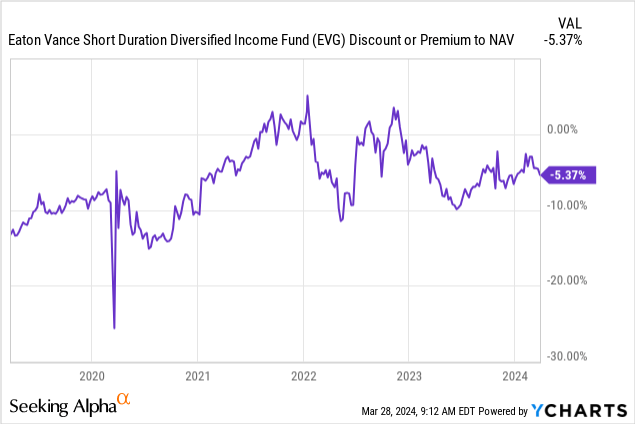

While the market has bid up other CEFs, EVG is still trading at a high discount due to its historic overdistribution:

We expect the name to move flat to NAV in the next twelve months, thus expect an additional +5% return from the discount narrowing. Buying this name at the current levels and using the Drip feature for CEFs is also a smart way to take advantage of the current fund analytics.

The above graph shows us how the fund historically traded at roughly -10% discount to NAV, with periods of premiums driven by intrinsic market technicals.

In today’s overbid market with stretched high yield, a retail investor needs to focus on relative value and the names which are still ‘cheap’. EVG falls in that category and historically has delivered in the year after Fed rate cuts, with a +16% total return in 2019 after the Fed cut rates.

Its low leverage is also an asset in the current environment, with many other names being dragged back by the high cost of funds for their floating rate leverage.

Risk factors

The main risk factor for this fund is a sudden and violent collapse in Fed Funds. If the economy goes south and the Fed cuts by 250 bps or more this year, the CEF will start seeing pressure on its cash flows towards the end of the year, with 2025 being possibly another year of ROC utilization. A smooth path of rate cuts in 2024/2025, consistent with the Fed ‘dot-plot’ and our base case scenario would not constitute a sudden loss of yield for the CEF.

The CEF’s low duration of only 2.5 years insulates it from more rate hikes, although we do not think there is any potential for such a move in a presidential election year.

Conclusion

EVG is a fixed income CEF. The fund has a low duration of only 2.5 years and a large AAA MBS bucket. The name used to overdistribute in a low interest rate environment, but is now utilizing very little ROC to sustain its 9% yield. The fund had a stable NAV in 2023 and will benefit from the Fed cutting rates as per the base case, as it did in 2019. Unlike some of its peers, the fund is still trading with a -5% discount to net asset value, which makes it an appealing choice in an otherwise stretched market.

Read the full article here

")

")

")

")

")