")

")

")

Unlike most investors, I find companies that focus on more traditional products and services to be the most interesting. The more ‘boring’ a company is from an operational perspective, the more I find it fascinating. Very little is as traditionally ‘boring’, I would argue, as businesses that produce and service machinery/equipment. One of the companies that I looked at last year that I became bullish about that is in this space is Alamo Group (NYSE:ALG). For those not familiar with the firm, it is a $2.11 billion enterprise that produces and sells not only vegetation management equipment, but also infrastructure maintenance equipment. Examples include tractor mounted and self-propelled mowers, tree and branch clippers, vacuum trucks, snow removal equipment, and more.

At the time that the article was published, which was in early February of 2023, I considered the company to be attractive. Leading up to that point, the firm was continuing to grow its revenue and its profits. Cash flows were also on the rise. The stock was not exactly cheap, but it was far from expensive. Ultimately, I ended up rating the company a ‘buy’ to reflect my view at the time that shares would likely outperform the broader market for the foreseeable future. To be clear, shares have risen, jumping by 11.2%. But that pales in comparison to the 32.8% move higher seen by the S&P 500. Fast forward to today, and I am more selective as an investor. I have become more cautious and I have a higher bar for what constitutes an undervalued opportunity. In addition to this, there is certain data about the firm that does look discouraging. Due to these factors, I think it’s an appropriate time to downgrade the firm to a ‘hold’.

The good and the bad

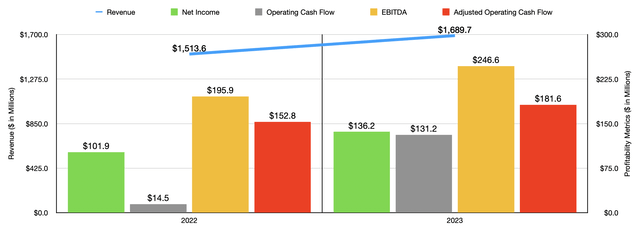

As I mentioned already, Alamo Group is a fairly decent sized firm. At present, the company has 29 global locations from which it does business. 17 of these are in the US. The others are split between Canada, Brazil, France, the UK, Netherlands, Australia, and China. From a financial perspective, this global reach has allowed the company to capture respectable growth. Take, as an example, how the company performed in 2023. Revenue came in that year at $1.69 billion. That’s 1.6% above the $1.51 billion the firm generated one year earlier. Both of the companies operating segments grew during this time. But that growth was not equal.

Author – SEC EDGAR Data

The Vegetation Management segment of the business, for instance, saw revenue expand by just 4.5% from $937.1 million to $979 million. Management attributed this to strong performance in the European agricultural and governmental mowing, forestry, and tree care spaces. Growth was also impressive in the North American governmental mowing equipment space. But the big driver, by far, was the Industrial Equipment segment. Revenue spiked 23.3% from $576.6 million to $710.6 million. Management attributed this to growth across the board, including in areas like excavator and vacuum trucks, sweepers and debris collection devices, and even snow removal equipment. An acquisition also helped to push revenue up.

With revenue rising, profitability also moved higher. Net income rose from $101.9 million to $136.2 million. This increase was driven not only by the higher revenue, but also by margin improvements. Most notably, the company’s gross profit margin expanded from 24.9% to 26.8%. Better operational performance, improved pricing, and higher sales volumes that spread fixed costs across more units shipped, ultimately were responsible for this. Other profitability metrics followed suit. Operating cash flow jumped by nearly a factor of 10 from $14.5 million to $131.2 million. If we adjust for changes in working capital, we get an increase from $152.8 million to $181.6 million. And finally, EBITDA for the business managed to rise from $195.9 million to $246.6 million.

Author – SEC EDGAR Data

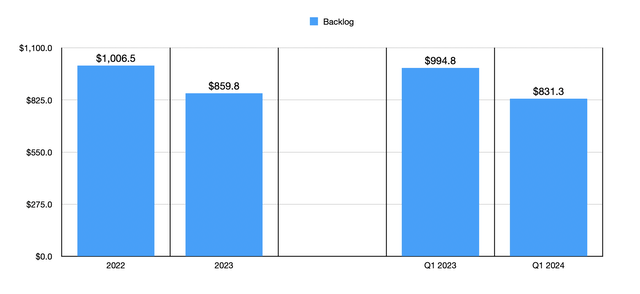

This is not to say that everything has been going great. The first big signs of weakness for the business actually occurred last year. By the end of 2023, backlog had fallen to $859.8 million. That’s down 14.6% over the $1.01 billion that the 2022 fiscal year ended at. According to management, this decline was driven largely by demand for vegetation management devices returning back to more normalized levels following the supply chain crunch that developed as a result of the COVID-19 pandemic. Unfortunately, backlog continues to decline. By the first quarter of this year, it had fallen to $831.3 million. That’s down 16.4% from the $994.8 million reported the same time last year. It’s also a drop of 3.3% from where it was at the end of last year.

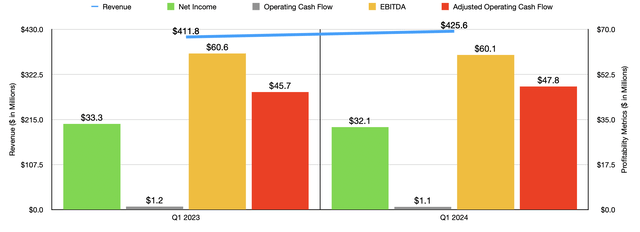

At some point, falling backlog will play a role in pushing revenue, profits, and cash flows, all lower. However, we haven’t really seen any sign of this coming into play just yet. In the first quarter of 2024, revenue for the business came in at $425.6 million. That’s up 3.4% from the $411.8 million reported the same time one year earlier. In this case, we saw a rather significant disparity from one segment to the next. The Vegetation Management segment actually saw sales drop by roughly 12.8% year over year, declining from $256.4 million to $223.7 million. A reduction in demand for forestry, tree care, and agricultural mowing products hit the business. By comparison, the Industrial Equipment segment of the business saw robust strength. Sales ended up spiking by 29.9% from $155.3 million to $201.8 million. Once again, management said that this was because of strong demand across the board. I have no doubt that this is at least partially because of major government investments in infrastructure. In fact, in another article recently, I touched on precisely that.

Author – SEC EDGAR Data

On the bottom line, things were a bit more mixed. Net income dipped from $33.3 million to $32.1 million. Even though sales increased, the company’s gross profit margin pulled back from 27% to 26%, largely because of lower margins associated with the company’s Industrial Equipment segment. During this window of time, operating cash flow dipped from $1.2 million to $1.1 million. But if we adjust for changes in working capital, we get an improvement from $45.7 million to $47.8 million. And lastly, EBITDA for the company dipped slightly from $60.6 million to $60.1 million.

Author – SEC EDGAR Data

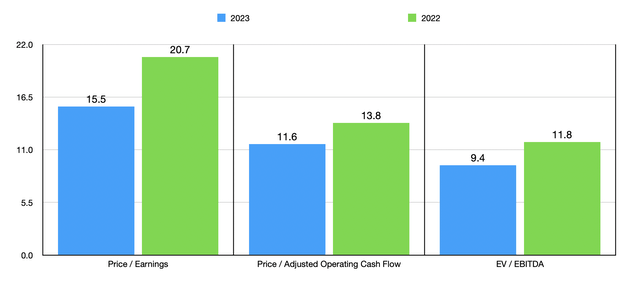

Given how close results are so far for 2024, I think it would be best to value the company just based on results from 2022 and 2023. In the chart above, you can see precisely that. Using the 2023 figures, shares definitely aren’t expensive. In fact, I would say that they tilt toward the cheap side. On an absolute basis, things are looking quite decent. But when we compare the firm to similar enterprises, the picture flips on its head. In the table below, you can see five similar companies stacked up against it. On both a price to earnings basis and on an EV to EBITDA basis, I found that four of the five companies ended up being cheaper than Alamo Group. And on a price to operating cash flow basis, our candidate ended up being the most expensive of the group.

| Company | Price / Earnings | Price / Operating Cash Flow | EV / EBITDA |

| Alamo Group | 15.5 | 11.6 | 9.4 |

| AGCO Corporation (AGCO) | 6.8 | 5.8 | 5.6 |

| Wabash National (WNC) | 5.0 | 4.2 | 3.8 |

| The Shyft Group (SHYF) | 65.4 | 9.0 | 25.8 |

| Terex Corporation (TEX) | 7.1 | 8.7 | 5.6 |

| Titan International (TWI) | 8.1 | 2.9 | 6.3 |

Takeaway

The way I see things, Alamo Group is still a solid company that, in the long run, will almost certainly create additional value for its investors. The stock is actually cheaper, in fact, than when I wrote about it previously. However, some things have gotten worse. Due largely to the weakness in the vegetation management space, the firm’s backlog has been declining. While shares are not expensive, they do look very pricey compared to similar enterprises. The uncertainty from the backlog, combined with the relative pricing of the business, is just enough for me to justify downgrading it from a ‘buy’ to a ‘hold’.

Read the full article here

")

")

")