")

Investment Overview

This is my first time providing coverage for Amphastar Pharmaceuticals (NASDAQ:AMPH), based in Rancho Cucamonga, California. The company completed its initial public offering (“IPO”) in 2014, raising ~$41m via the issuance of ~5.84m shares priced at $7 per share.

Amphastar stock trades at $45 per share at the time of writing, up >500% since IPO. In December 2023, the stock reached its highest value of >$60 per share.

According to the company’s Q2 2024 quarterly report / 10Q submission:

We are a bio-pharmaceutical company focusing primarily on developing, manufacturing, marketing and selling technically challenging generic and proprietary injectable, inhalation, and intranasal products, as well as insulin API products. We currently manufacture and sell over 25 products.

Our largest products by net revenues currently include BAQSIMI®, Primatene MIST®, glucagon, epinephrine, lidocaine, enoxaparin sodium, and phytonadione.

We are currently developing a portfolio of generic abbreviated new drug applications, or ANDAs, biosimilar insulin product candidates and proprietary product candidates, which are in various stages of development and target a variety of indications. Three of the ANDAs are currently on file with the FDA.

Firstly, let’s consider the company’s financial history:

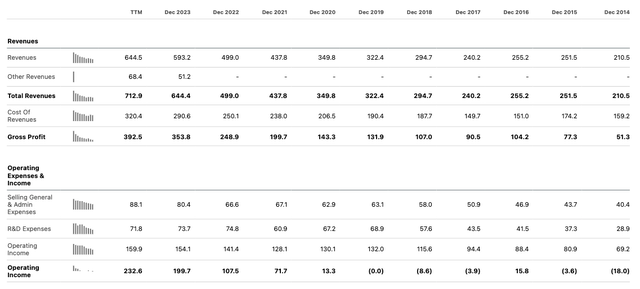

Amphastar – annual income statements (Seeking Alpha)

As we can see, Amphastar has grown revenues in almost every year since listing, and has become increasingly profitable. In Q2 2024, the company outperformed analyst’s estimates, reporting net revenue of $182.4m, and GAAP net income of $37.9m, or $0.73 per share, and adjusted net income of $48.7m, or $0.94 per share.

Portfolio Overview – Is Baqsimi Impact On Revenue A Genuine Positive?

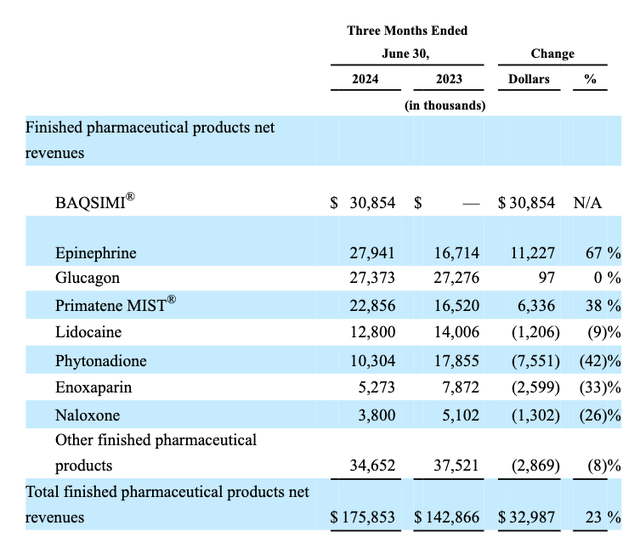

In Q2, management reported product-by-product sales as follows:

Amphastar product revenues Q2 (10Q submission)

As we can see, Baqsimi was the main product revenue driver during the quarter. In June last year, Amphastar completed the acquisition of Baqsimi – “the first and only nasally administered glucagon for the treatment of severe hypoglycemia in people with diabetes” – from Pharma giant Eli Lilly (LLY). In a press release issued at the time, the deal terms were disclosed as follows:

Amphastar paid $500 million at the closing of the Acquisition and is required to pay an additional $125 million at the one-year anniversary of the closing of the Acquisition. Amphastar may also be required to pay additional contingent consideration of up to $450 million to Lilly based on the achievement of certain milestones.

In order to finance its purchase of Baqsimi, Amphastar entered into a credit agreement with Wells Fargo (WFC) bank, the terms of which are shared in the company 2023 annual report / 10K submission as follows:

On June 30, 2023, in conjunction with the Company’s acquisition of BAQSIMI®, the Company entered into a $700.0 million syndicated credit agreement, or the Credit Agreement, by and among the Company, certain subsidiaries of the Company, as guarantors, certain lenders, and Wells Fargo Bank.

The Credit Agreement provides for a senior secured term loan, or the Wells Fargo Term Loan in an aggregate principal amount of $500.0 million. The Wells Fargo Term Loan matures on the June 30, 2028.

The Credit Agreement also provides a senior secured revolving credit facility, or the Revolving Credit Facility, in an aggregate principal amount of $200.0 million. The Revolving Credit Facility matures on June 30, 2028. As of December 31, 2023, the Company had no borrowings outstanding under the Revolving Credit Facility.

Amphastar has already paid back $250m of the term loan (primarily due to its issuance of $345m of convertible notes due 2029) while paying an interest rate of 2% per annum, and has also paid back the additional $125m due on the one-year anniversary of the deal.

A recent, very detailed Seeking Alpha post on Amphastar offering a “Strong Sell” recommendation has contended that, with up to $450m still due to Lilly in milestones, and the drug looking like it will earn ~$120 – $150m of revenues per annum, Amphastar will end up paying back most of the revenues earned from Baqsimi to Lilly, whilst also cannibalising revenues from its other glucagon based products.

I agree that this is a valid point – in the short term at least, but it is worth noting that we don’t – so far as I am aware – know the precise nature of the milestones, and it seems doubtful that Amphastar would agree to a deal in which, the SA post speculates, 90% of EBITDA generated by Baqsimi is returned to Lilly each year.

Equally, Baqsimi’s patents are not due to expire until 2036, so in theory at least, Amphastar may generate perhaps $150m per annum for the next 12 years, or >$1.8bn, and if we speculate that ~50% of the Lilly milestone only kicks in after the product achieves $1bn in total revenues, and the other when revenues >$2bn, then the outlook for the drug would be a profitable one and the deal justified. I’d say the jury remains out on the deal.

Epinephrine / Primatene – Can Recent Revenue Growth Be Sustained?

The other two products that drove major year-on-year growth in Q2 were epinephrine and Primatene Mist. Epinephrine is an injection indicated for emergency treatment of allergic reactions, including anaphylaxis, and there is plenty of competition in this market.

The current biggest selling competition in this market is Viatris’ EpiPen, which earned revenues of $442m in 2023, and there is more competition incoming in the form of Ars Pharmaceuticals recently approved nasal spray neffy, and potentially, Aquestive Therapeutics buccal film product Libervant, which may be approved next year.

The annual increase in Q2 revenues was apparently due to supply shortages at other firms – a phenomenon that is not likely to repeat every year, so the growth potential of this product does not feel exciting, although it could be a ~$75m per annum selling product for some years to come, in my view, due to its established market presence.

Primatene Mist is an over the counter (“OTC”) nasal spray for asthma whose impressive gains in Q2 were down to “an increase in unit volumes”, management says. The approval of the product is apparently somewhat controversial, but it is the only product of its kind, therefore we might speculate this could a $150m – $200m per annum peak selling product.

Reviewing the remainder of the product portfolio, however, we can see multiple products experiencing falling revenues, and it seems clear that, if Amphastar wants to continue its impressive top line and bottom line growth trajectory, and keep rewarding shareholders, new product approvals are a must.

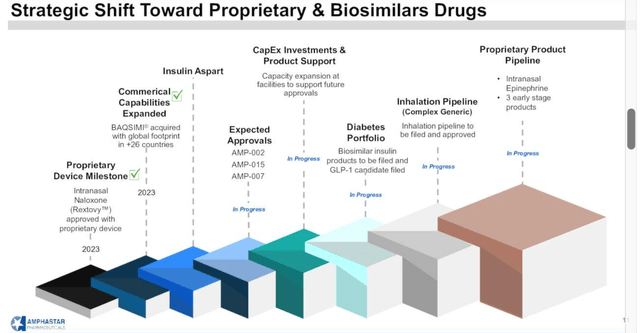

Amphastar Pipeline Overview – Transition To Proprietary Products

In 2021, Amphastar’s pipeline was comprised of 63% generic products, 16% biosimilars, and 21% proprietary – by 2025, the company hopes to have 50% proprietary products, 15% generic, and 35% biosimilar. (A biosimilar is essentially a generic for a biologic drug, such as AbbVie’s (ABBV) Humira for example.)

Amphastar planned strategic shift (Q2 earnings presentation)

Reviewing the slide above from Amphastar’s Q2 earnings presentation, we can point to numerous intriguing developments. The recent approval of Rextovy could be one, however management tempered expectations on the recent earnings call, stating that “we don’t really anticipate it being a big product for us just because of the competitive nature of that environment there.”

Besides AMP-004, three further products are pending approval, and a biosimilar GLP-1 agonist – the same class of drug as Eli Lilly (LLY) and Novo Nordisk’s (NVO) “miracle” weight loss drugs Zepbound and Wegovy (which have >$100bn peak revenue expectations), is certainly of interest.

Intranasal epinephrine has already been launched by Ars Pharmaceuticals (SPRY), as mentioned above, but there is nothing stopping Amphastar launching a competing product so long as it does not infringe patents.

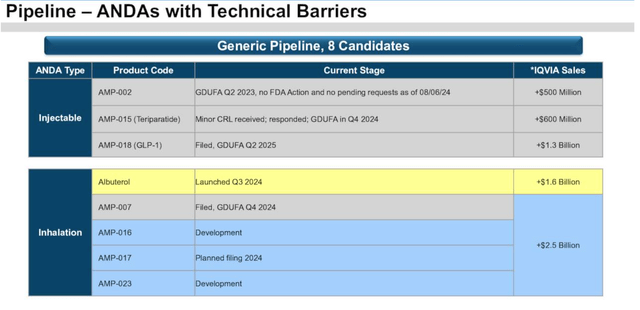

Amphastar – pipeline expectations (Presentation)

As we can see above, Amphastar appears to be sharing some lofty expectations for its pipeline products. AMP-002 was recently rejected for approval, and my research has been unable to uncover precisely what its indication is, while AMP-015 has also received the dreaded “Complete Response Letter” from the FDA, making Amphastar 0 for 2 so far, which is somewhat discouraging.

The GLP-1 generic could be a version of liraglutide, which may not possess the same weight loss qualities as semaglutide – Wegovy, or tirzepatide – Zepbound, but could be a triple-digit-million selling product, while there is no reference made to AMP-016, or AMP-007, or AMP-017, in any of Amphastar’s recent filings, so its impossible to estimate what a realistic market opportunity may be.

Regarding the insulin aspart generic AMP-004, management advised on the Q2 earnings call, “the product is expected to be refiled in the third quarter of 2024”. The diabetes portfolio the company is building appears comprehensive – provided all products are approved, which seems doubtful, but I’d stop short of calling it lucrative as insulin prices have been slashed and there is nothing differentiating the products from other generic competitors.

AMP-015, a generic for teriparatide, or Lilly’s Forteo, which long since lost patent protection, is not a product launch I’d be overly excited about.

Concluding Thoughts – Lumpy Revenue Generation & Perplexing Pipeline Keeps Me On Sidelines

Amphastar stock has delivered excellent returns for shareholders – up >110% across a five year period, and its ability to grow revenues and income, as I have discussed, is impressive.

I have to say however that reviewing recent earnings – we might note no guidance has been provided for 2024, or 2025 – and taking a closer look at the pipeline, it is hard to see how Amphastar is going to maintain its momentum.

It seems the company’s requests for commercial approval are being consistently knocked back by the FDA, and it’s hard to find a standout product in the pipeline to get excited about especially when the competition is so fierce. Here is a list of competitors provided by Amphastar itself in its 2023 10K:

Pfizer, Inc. (PFE), Sagent Pharmaceuticals, Inc., Akorn, Inc., Sandoz Inc., Viatris Inc. (VTRS), Fresenius Kabi USA (FMS), Nexus Pharmaceuticals, Apotex Corp, Amneal Biosciences (OTC:AMNL), American Regent Inc., Hikma Pharmaceuticals USA, Inc., Par Pharmaceuticals, Cipla USA Inc., Meitheal Pharmaceuticals, Dr. Reddy’s Laboratories, Inc. (RDY), Sun Pharmaceuticals, Inc., Xeris, Pharmaceuticals, Novo Nordisk (NVO), Medefil Inc., Accord Healthcare, Eugia Pharma, Amring Pharmaceuticals, Bausch Health (BHC), Zydus Pharmaceuticals USA Inc., AuroMedics Pharma LLC, and Teva Pharmaceutical Industries Ltd. (TEVA).

Additionally, when I look to see what proprietary products the company might launch in the coming years, I am also perplexed – other than the nasal spray for epinephrine, which as mentioned, a version of which has already been launched by ARS, it’s unclear what these new products may be.

It’s hard to deny Amphastar has been successful, but on the basis that it is not a good idea to invest in a company whose business you don’t understand, I am firmly on the sideline with Amphastar. I don’t understand where the next >$100m, or even >$50m product is coming from, and therefore, with so many products revenues falling in Q2, and the performance of epinephrine potentially a one-off, I am initiating my coverage of Amphastar with a “Hold” call.

Read the full article here

")

")

")

")

")