")

")

Assertio Holdings, Inc. (NASDAQ:ASRT) shares provide one of the most asymmetric bets we’ve seen in the markets over the last few months. This company is ongoing a deep turnaround that will reshape its operations forever, and the market is likely assigning a significant discount to this plan. However, we believe that their proven strategy of monetizing underappreciated pharma assets will again prove successful, leaving plenty of upside for shareholders.

The story: a lucky merger left Assertio with more value than expected

The business model of Assertio is a risky one: drugs distributor. The company buys the rights to some drugs that have been on the market for several years. These are proven drugs that may still lack competition (i.e. there is no approved and marketed generic), and there is an opportunity to profit from price increases. The company’s golden goose was a drug called INDOCIN, which was a nonsteroidal anti-inflammatory drug (NSAID) that decreases inflammation. This asset was doing close to $100 million in annualized sales at its peak in H1 2023.

However, their luck ended last summer when news came out that there was a generic ready to be approved. The approval of a generic means that the gains from holding the rights to the original drug will virtually zero out immediately, as a more price-competitive product enters the market.

Luckily for Assertio, they had entered into an agreement to merger with another pharma company in an all-stock transaction that valued the two entities at more than $400 million at peak, with $248 million paid for the target. The target was a company called Spectrum Pharmaceuticals, and their flagship product is Rolvedon, which is used to reduce the incidence of infection due to chemotherapy-induced neutropenia. The timing of this transaction was simply perfect: the deal closed around a month before the generic approval news crashed Assertio’s stock price, leaving Spectrum shareholders with only a fraction of the total consideration they expected to get. Today’s market cap of around $100 million suggests that the value of Assertio without the merger would likely be close to zero.

The opportunity is called Rolvedon: another INDOCIN?

The key to understanding the thesis behind Assertio is to look at what exactly the company does. They are expert in monetizing pharma assets that have been poorly performing. Other companies may not have the resources (sales force) or the expertise (sales know-how) to effectively market these drugs successfully, and this is where Assertio comes in. These companies are happy to sell the rights or themselves (like the Spectrum deal).

In this case, ASRT lost its golden goose (INDOCIN), but it likely got a new one, called Rolvedon. This drug is expected to be the major driver of the new pro forma company, and its success will determine the shareholder’s well-being. So our thesis is basic: the company will be able to work its magic on this asset like it did with INDOCIN, and it will eventually outperform the market expectations on sales and cash flows. Let’s look at the numbers so far. This is from the latest earnings call transcript:

We are off to a good start this year. Our first quarter is tracking with our full-year guidance, calling for sales of $110 million to $125 million and EBITDA of $20 million to $30 million. There is demonstrated execution across several fronts. Rolvedon Q1 sales are up 32% quarter-over-quarter. This is Rolvedon’s fifth consecutive quarter of demand growth, a critical success measure in the intensely competitive long-acting G-CSF category.

We extract two key points: (1) Assertio is on track for $25 million of EBITDA as per 2024 midpoint guidance, and (2) Rolvedon is over-performing in terms of growing and sustained demand. Sales of this drug are up more than 30% YoY, which is likely driven by the company’s sales efforts and know-how after picking up this asset from Spectrum. Just for comparison, at its peak in 2022, ASRT was doing close to $80 million in FCF, which today would correspond to around 80% of its market cap and twice its EV! Management also provided this commentary:

We are also looking to expand into new hospital customers as we continually work towards building Rolvedon into greater than a $100 million asset in the years ahead. […] I also want to be clear, we are not satisfied with where our stock price is, but we believe that driving sustainable long-term shareholder value is best achieved by growing sales and profitability by diversifying our revenue streams and by generating more predictable cash flows.

These are two other important points. The target for Rolvedon is more than $100 million in sales, which would make it an INDOCIN-like success story. The TAM for Neutropenia, which is the main condition targeted by Rolvedon, is around $15 billion and is expected to grow at around 5% CAGR through 2030. So realistically, we are talking here of capturing a 0.6% market share.

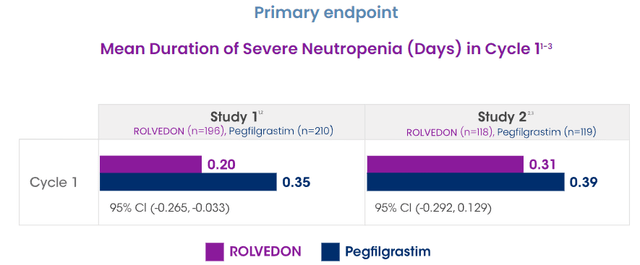

The idea behind marketing Rolvedon is, in fact, not to compete with the best-in-class treatments like Neulasta ($1 billion in sales), or Neupogen, but to go after those few patients that cannot access these treatments. Indeed, many of them either have side effects or are not covered and need a less expensive alternative, which would be Rolvedon. This drug has also demonstrated its efficacy over pegfilgrastim, and thus presents a compelling choice for these patients.

Rolvedon Efficacy Profile (Rolvedon.com)

And they are focused on accretive acquisitions that can expand the share price faster than buybacks. This is an important point as they have around $40 million of net cash and $80 million of total cash, which can be used for acquisitions.

The focus on valuation: a DCF model approach

To evaluate the company, we will employ a discounted cash flow (“DCF”) model, given the lack of proper comparables. In fact, after the transformation of the company in 2023, it is a true challenge to find competitors that are at the same stage as Assertio. We will make some basic assumptions:

-

Revenue growth at around 20% for the next 2 years based on Rolvedon expansion and strategic M&A, followed by a period of milder growth at 8% which rapidly slows down to 4% after 2027. Terminal growth at 3%.

-

The discount factor is the WACC, computed at around 12% to reflect the high risk embedded in the business. The debt of the company is also convertible, so all WACC can be actually seen as the cost of equity alone.

-

EBITDA margins are expected to be stable and close to historical levels of around 30% once the sales are mature.

These expectations are then embedded into a larger picture: we think the company will spend the $80 million of cash on hand to pursue some bolt-on strategic acquisitions. These transactions will likely aim at diversifying the business and moving away from the large black-swan risks that risked destroying the company in 2023.

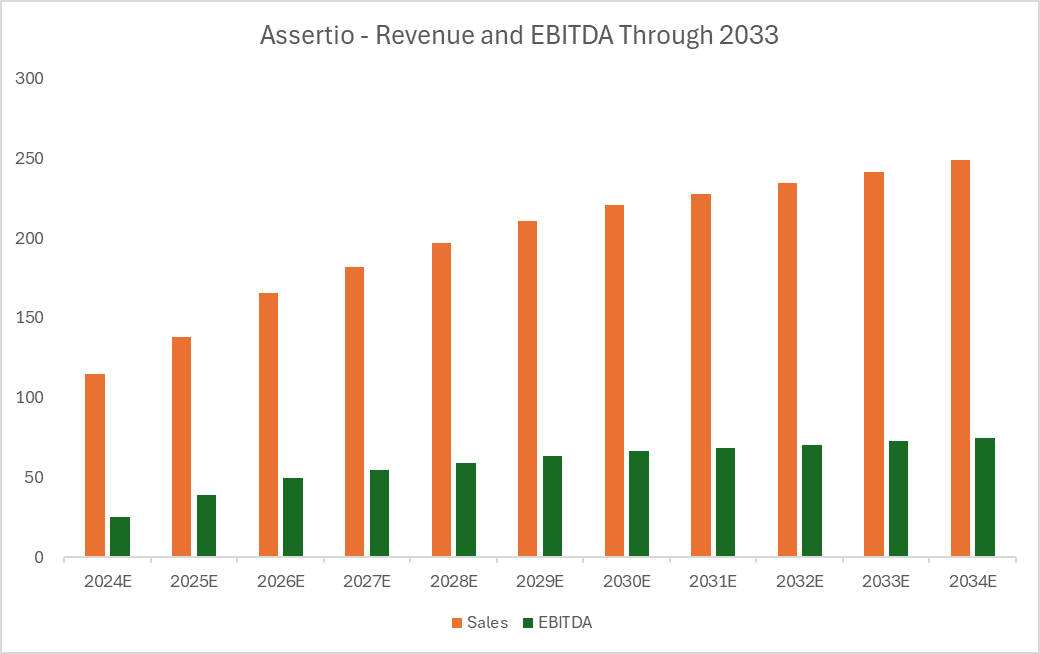

Forecasted Financials (Author’s DCF)

Basically, this is the outcome of our assumptions: revenue growth spurred by M&A and organic Rolvedon expansion and growing EBITDA after 2025. This brings a total fair EV of $300 million, which after adding $40 million of net cash means $340 million of fair equity value, or $4.00 per share. This translates into an upside potential of around 300% from the current share price.

Risks: the high reward comes with also high risks

As it is often the case in the market, there is no free lunch. In this case, the 300% upside potential is coupled with significant idiosyncratic risks that are inherited from the business model itself. This goes back to how the company makes money: marketing drugs that have no approved generic competition. However, were any generics approved – as it was the case with INDOCIN – their rights would immediately become worthless and their sales significantly affected. This is still true also for Rolvedon and could materialize at any moment. This is why shareholders are generously compensated in terms of FCF yield and returns.

There are also some systemic risks as always, but in the case of Assertio, the idiosyncratic ones are so large – as it is the upside opportunity – that they are negligible. All in all, we believe that investors are more than compensated for all these risks (after all, 300% is a lot), but they should be aware of the price they are paying for these returns: risk.

Conclusion

Assertio Holdings, Inc. is a high-risk, high-return opportunity that is wildly understated by the market. The company was entirely transformed last year as a generic was approved and directly competed with its flagship drug. However, a lucky merger saved the company’s future prospects. Today, Assertio has the opportunity to prove to the market that cash flows have not stopped, and the new asset Rolvedon may become the next golden goose.

Read the full article here

")

")

")