")

")

Intro

We wrote about B&G Foods, Inc. (NYSE:BGS) in June of last year when we stated that all long-term associated investments should be off the table. Ongoing profitability woes, a sustained pattern of lower lows on the technical chart & growing interest expense were all clear risk factors at the time of writing our most recent commentary close to 13 months ago. Despite the dividend being kept over this period, shares have still lost approximately 35% in value after dividend proceeds have been allocated. Not only is this a significant negative return, but also a sizable opportunity cost, considering the S&P500 returned north of +27% over the same period.

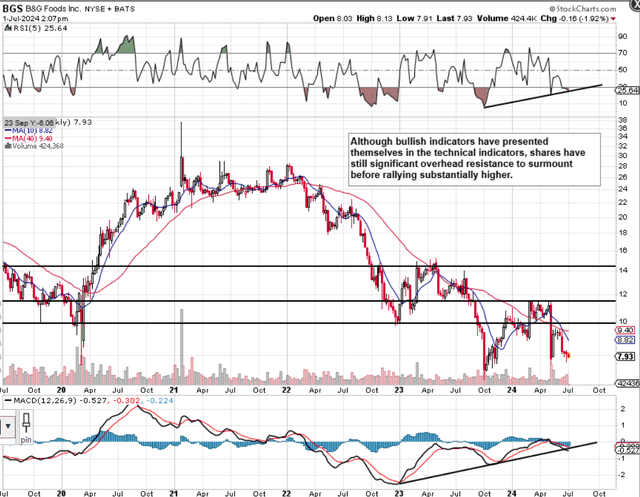

As we see however, from B&G’s technical chart below, shares may finally be closing in on a multi-year bottom. We state this because of the bullish divergences in both the RSI momentum technical indicator, as well as the MACD. Furthermore, given how low shares have stooped in recent months, it was refreshing to see Piper Sandler upgrade the stock this month. Some may state the upgrade announcement was premature given the prevailing bearish trend & the significant amount of technical resistance shares must overcome to get back to the types of levels we witnessed back in calendar 2021. Furthermore, the ongoing slowdown in traffic outside the home for B&G’s offerings does not look like it will end tomorrow.

Therefore, let’s go through the company’s key valuation multiples and point to what we look for before potentially putting capital to work in long-term plays.

B&G Intermediate Technical Chart (Stockcharts.com)

Growth Headwinds To Result In More Divestitures

Both net revenues and GAAP earnings missed consensus estimates in the recent first quarter earnings report this year (announced on the 8th of May). While net revenues came in at $475.22 million, GAAP earnings came in negative at -$0.51 per share or at -$40.2 million for the quarter. While a rolling quarter decline was expected (due to being up against a tough comparable concerning the sale of the ‘Green Giant U.S. shelf-stable’ business), it remains evident that food services remain soft which is why constructive change is called for at B&G.

Although negative bottom-line profitability many times is frowned upon by value investors, often it is beneficial to move up the income statement when a company is carrying a significant amount of debt (As B&G Foods is). Long-term debt at the end of Q1 came in at $2.014 billion, equating to a sizable trailing 12-month interest expense of $149.7 million.

However, with the possibility of all assets being sold in B&G’s ‘frozen and vegetable business unit’ before the end of the year, a sizable dent could be made in the company’s debt which the market may take as a stepping stone to improved results. Asset sales would ease some pressure somewhat from the recent notes offering & balance-sheet at large. Substantial divestitures in the frozen & vegetable unit would immediately increase profit margins significantly at B&G. We state this because the frozen and vegetable business segment made up only 7.5% of adjusted EBITDA in Q1 from a corresponding top-line take of 22% of gross quarterly sales.

To this point, the key going forward for B&G will be growing businesses (such as Spices & Flavor Solutions) which contributed almost one-third of B&G’s adjusted EBITDA off mere revenues of approximately 20%. Suffice it to say, it makes sense here by divesting what is NOT working (80-20 rule) & expanding (through acquisitions if needs be) into areas which are working for the company.

EBIT over the past 12 months comes in at $234.3 million, resulting in an EV / EBIT multiple of 11.53 (B&G 5 Year average of 14.85). Suffice it to say, although B&G remains unprofitable from a bottom-line GAAP standpoint, the company does not look expensive when compared to the company’s historic EBIT multiples as well as to what the sector is currently valued at (EV / EBIT multiple of 14.79).

Sales & Assets Trading On The Cheap

As we see from the table below, given the sustained downturn in the share price over the past 30 months, B&G’s assets & sales are trading well below their historic averages and the sector in general. Even if we include the ramifications of B&G’s leverage where refinancing initiatives remain ongoing, we still see that the company’s EV/ Sales multiple also considerably trails the averages.

| Valuation Multiple | BGS Trailing | Sector Median | BGS 5-Year Average |

| EV / Sales | 1.33 | 1.71 | 1.81 |

| Price To Sales | 0.30 | 1.21 | 0.70 |

| Price To Book | 0.80 | 2.35 | 1.63 |

Earnings & its associated growth are always the focal point when it comes to Wall Street interest. Nevertheless, there are two drivers of earnings, which are essentially B&G’s sales & assets. How sales result in earnings is obvious (demonstrated on the income statement), but many investors overlook the fact that assets also create earnings (which gives credence to the value of B&G’s multiple brands illustrated by the $1.6+ billion of intangible assets on the balance sheet).

Suffice it to say, a low P/B multiple combined with a low P/S multiple is probably the best combination when sizing up potential long-term value plays. What we now need to see is continued gross margin expansion, divestment of poorly performing assets & volumes to recover in the latter part of the year. If the above can be accomplished, then it should only be a matter of time before a final technical bottom can be confirmed.

Conclusion

To sum up, we are reiterating our ‘Hold’ in B&G Foods as we believe a firm multi-year bottom may be finally approaching. We state this because of how low the company’s book & sales multiple have fallen and the fact that poorly performing brands have been earmarked for sale this year. To this point, we also believe a temporary suspension of the dividend would help the technicals give us the bottom we are looking for. Let’s see what the second quarter brings. We look forward to continued coverage.

Read the full article here

")

")

")

")

")