")

")

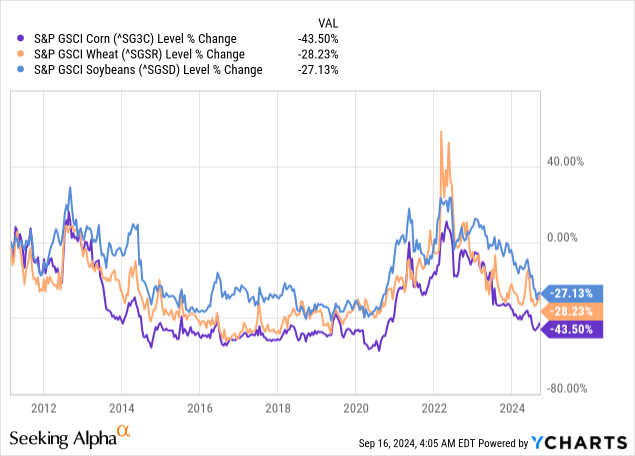

Bioceres (NASDAQ:BIOX) 4Q24 results disappointed the market, with the stock falling close to 15% after the release (and 30% since my last Hold article on the company). The main disappointment came from flattish profitability for the year, mostly caused by a decreasing business in crop nutrition in Q4. The generalized bear market in wheat, corn, and soybeans probably helped the pessimistic mood around Bioceres.

Although the company continues advancing its HB4 products (with an important permit gained in the US wheat market), the path for the rollout of this product continues to get extended. The company has recognized some challenges in its commercialization strategy for HB4 (inseparable from the bear market in commodities) and will try to address these challenges in FY25.

Because it is a growing company with a low earnings yield and high debt connected to the volatile commodities market, Bioceres should provide a high return from growth. Bioceres is advancing its genetics program but continues to bump into challenges. The current bear market in agricultural commodities is clearly not helping either. This makes me not very confident in the company’s future growth. For that reason, I continue to believe that Bioceres is not an opportunity, and I rate the stock as a Hold despite the lower stock prices after the 2Q24 results.

4Q24 results

Growing but not as needed: Bioceres top-line grew 11% in FY24 and 18% in 4Q24. These are not bad figures, but as generally happens with growth companies, good growth still does not meet expectations, leading to falling stock prices.

Bear market in grains, post-drought Argentina: The year was clearly marked by a reduction in prices for the crops to which Bioceres products serve. These prices are already close to the level of the previous bear market in crops between 2014 and 2020. In fact, during the call, management commented that soybean prices are already below average yields for Brazilian farmers (Brazil is the largest producer of soybeans). This means the crop is now uneconomical for half of the producers in Brazil.

Price pressure means that farmers are trying to manage their costs more consciously, putting pressure on the prices and volumes of inputs producers like Bioceres.

On the other hand, the year had a tailwind from a recovering Argentina, particularly in the first half of the year (the planting season in Argentina). The comparison from FY23 was terrible, as Argentina had suffered its worst drought in decades.

Profitability challenges: The topline growth posted by the company was not accompanied by gross profit nor EBITDA growth, which were flat to last year (implying falling margins). Operating income was actually down for the year. There were two reasons for the fall in margins: first, the company’s agreement with Syngenta for the commercialization of seed care solutions generated lower payments (these come at 100% margins), and second, the company sold more HB4 at low margins from its identity-protected program. For more details on the Syngenta agreement, see my article from January 2023, and for the identity-protected program, see my article from March 2024.

Debts up, change in working capital policy: The company’s debt continued to rise, particularly on its short-term side. Short-term debt rose from a level of $103 million in 2Q24 to $135 million in 4Q24. I had warned about short-term debt in my article from March 2024 as the company did not correctly disclose if these short-term debts were part of a working capital facility (and therefore lower maturity risk) or part of a maturing loan. This has not been clarified yet, and the company has not published its 20-F for FY24 so far.

However, the company commented that it would reduce the priority of its identity-protected program for HB4, which absorbs significant working capital, a measure probably related to the cost of maintaining short-term debt. The identity-protected program requires Bioceres to buy the production from the farmers and then resell it, which takes up a lot of cash.

Other business developments

Waiting for FY25 HB4 soy: The company had commented in 2Q24 that it expected to launch HB4 soy varieties commercially in Brazil and other markets in FY25 (currently in the seed multiplication phase). There were no comments on the 4Q24 call, but the planting season is starting in the Southern Hemisphere, so by 1H25, we should have more data on this important development.

Change of tactics for HB4: The company announced several tactical changes for its HB4 program.

As mentioned above, it will decrease the priority of the identity-protected program, meaning that it will try to sell to farmers (or multipliers actually) without guaranteeing to buy back the production. That means more risk for the downstream chain and, therefore, a slower rollout. The company did this to protect working capital.

As part of its commercial sales of HB4 wheat in Argentina, the company found that its royalty prices are too high, at close to $11/bag, without any adjustment for falling prices. The company will probably reduce this royalty in future quarters. It will probably also need to partner more strongly with more established seed breeders to insert HB4 into more accepted seed strains already used in the market. The same need for partners seems to be recognized for HB4 soy, even more than for wheat.

This delays the expected growth of HB4 in the important geographies of Argentina and Brazil. Management said that ‘despite the good performance we’re seeing in Brazil and the significant improvements in our Argentine portfolio varieties, we believe that it will take us one to two more years to have the portfolio depth and validation that is required to achieve our previous guidance under this new business approach.’

Wheat approvals in the US: On a more positive note, the HB4 wheat variety now has full non-regulated field activity in the US, which means Bioceres can start the process of partnering with seed multipliers to incorporate HB4 traits into other genetics. Management said that they will try to license HB4 to many partners and that they will focus on the Midwestern varieties, or about 1/4 of the US market (which are consumed domestically and, therefore, require fewer import permits). Still, this process is only starting, which means one to two years until we see commercialization in the US.

Bio gaining weight: Bioceres acquired Marrone Bio Innovations in 2022, and the bio side of its business now represents 25% of revenues and probably a little more in profits (given that the products carry higher margins, as commented by management during the call). The company is now considering giving more priority in terms of capital and managerial time to this sector than to HB4 (also as commented during the call). The bio solutions segment is interesting because of regulatory tailwinds (for example, chemical use limitations in Europe).

Valuation

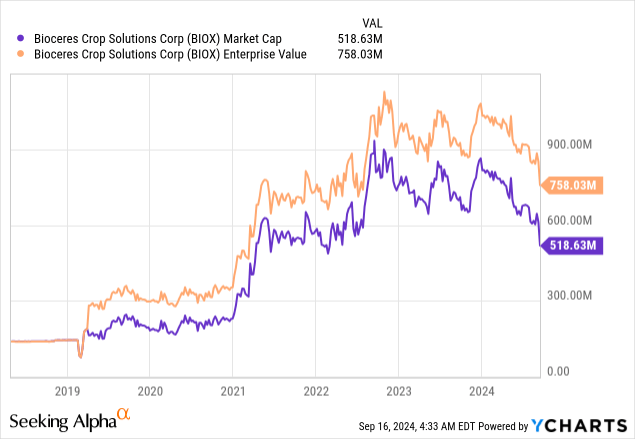

Since my last article, Bioceres’ stock price is down more than 30%, so the valuation deserves a review.

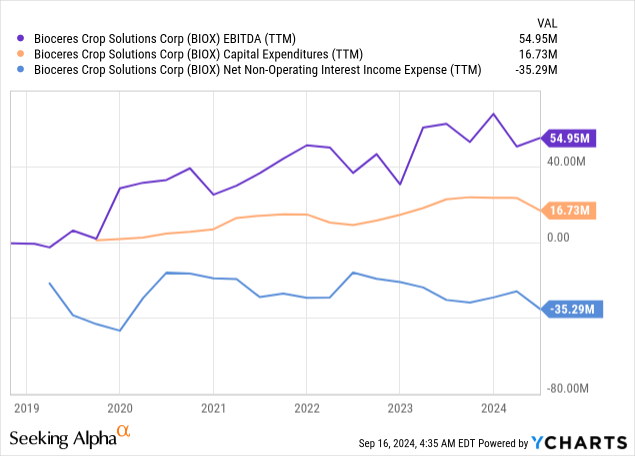

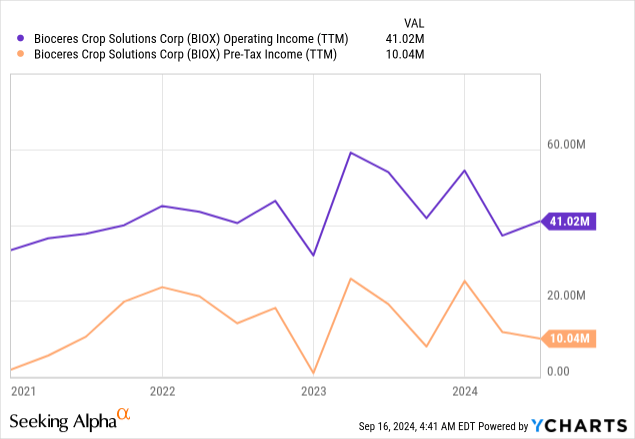

Low earnings yields: From a current profitability perspective, Bioceres offers a low earnings yield. The company’s market cap is about $520 million, and its EV is about $760 million. Against these, the company posts EBITDA of $55 million TTM, or $40 million cash operating income after CAPEX, or about $26 million NOPAT after taxes of 35%. From $40 million cash operating income, we only get $5 million in pre-tax income after interest.

This means the company basically trades at an EV/NOPAT of about 30x and a P/E of more than 100x. These are very low yields, of about 3% on the EV and 1% on the market cap.

Lower growth expectations: In the past six months, the company’s fundamentals have not changed meaningfully in the short term, although they have in the long term. Mainly, the low prices for agricultural commodities and the recognition of commercialization challenges for HB4 should moderate the expectations for growth ahead for the company.

Still lacking debt clarity: On the financial side, I am still concerned with the lack of clarity about maturities for short-term debt, which is not mentioned in the company’s press releases, earnings presentations, or quarterly financial statements. This puts significant risk on the name, as the debt may need to be repaid with dilution or refinanced at higher rates.

The risk from the debt position, plus the company’s volatility absorbed from the commodities market, implies that Bioceres requires a high return in order to be fairly valued. This depends on each reader’s considerations, but I believe a minimum return of 15% is needed.

If the current earnings yield is 1%, the remaining 14% has to come from earnings growth. The company seems to be able to post revenues growing at close to those figures. In addition, that rate of growth should multiply through the income statement via operational and financial leverage. However, the growth in operating and pre-tax income has been negligible for the past three years, and the company has just announced more challenges to its HB4 program. I believe projecting 14% profitability growth going forward is challenging when looking at the company’s performance so far.

Conclusions

Because it is a growing company with a low earnings yield and high debt connected to the volatile commodities market, Bioceres should provide a high return from growth. Bioceres is advancing its genetics program but continues to bump into challenges. The current bear market in agricultural commodities is clearly not helping either. This makes me not very confident in the company’s future growth.

For that reason, I continue to believe that Bioceres is not an opportunity, and I rate the stock as a Hold despite the lower stock prices after the 2Q24 results.

Read the full article here

Q3 2024 Earnings Call Transcript")

")

")

: Strong Read From Delta’s Earnings")