")

")

Introduction

Earlier this year, BGC Group (BGC) announced that it had received approval from regulators for FMX Futures Exchange to enter into the U.S. interest rate futures market. In a market that was essentially dominated by CME Group (NASDAQ:CME), which had a de-facto monopoly in the space, CME faces serious challenges ahead with respect to its competitive position and economic moat. In this article, I’ll analyze the latest quarter, discuss what I view as the key risks to CME, and share my outlook for the company. I’ll also share my thoughts on valuation and how I would play the stock today.

Company Overview

CME Group is a powerhouse in global financial markets, running some of the biggest exchanges worldwide. This includes the Chicago Mercantile Exchange (CME) and the New York Mercantile Exchange (NYMEX). CME Group offers all sorts of products (think futures and options) across things like commodities, energy, and currencies.

More broadly, what CME really does is provide a platform for investors to trade these contracts. Not just for buying and selling, but also for managing risk and figuring out fair prices crops, oil, metals, and more. Based out of Chicago, CME Group plays a part in keeping the wheels turning in global finance, helping businesses and investors hedge against risk and manage portfolios.

Background

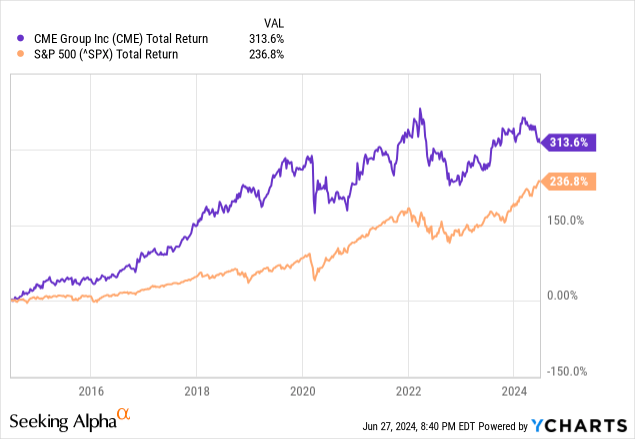

Shares of CME Group have rewarded long-term shareholders. When looking at the total return of CME Group over the last decade, shares have returned 314% compared to the S&P500’s return of just 237%. On a compounded annualized basis, this equates to a CAGR of 15.3%. This means that investors have more than doubled their money every five years.

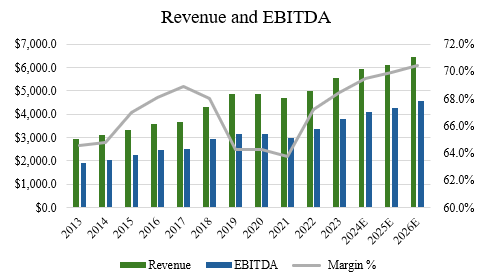

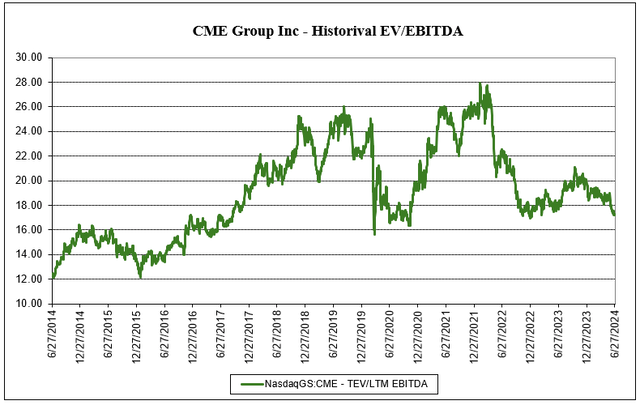

CME Group’s share price returns are backed up by its financials. Over the last decade, CME has grown its revenues at a CAGR of 7.3% and EBITDA at a CAGR of 6.6%. More recently, in the last 5 years, the company has grown revenues and EBITDA at CAGRs of 5.3% and 5.4%, respectively (source: S&P Capital IQ). While these numbers are not high growth, they’ve definitely been consistent, as evidenced by steady growth on the top line along with some margin expansion. At the same time, it should be pointed out that much of the share price out performance relative to the S&P500 is due to multiple expansion, where the company’s EV/EBITDA increased from 12.3x a decade ago to 17.3x today.

Author, based on data from S&P Capital IQ

Recent Results

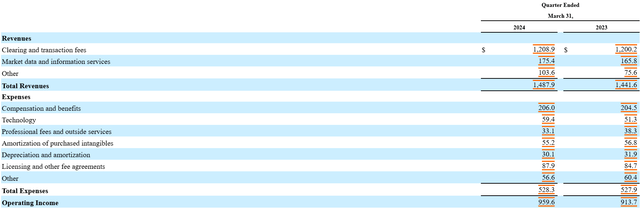

CME Group reported its Q1’24 on May 1st for the period ending March 31. During the quarter, the company reported revenue of $1.49 billion, which was 3% higher than last year. Compared to consensus estimates, revenue came in line with expectations, with a small beat of $13 million.

Company Filings

When looking at what drove the results, the core business only grew 1% to $1.21 billion, with the market data and information services segment growing 6%. Most of the core business growth didn’t come from volumes, total contract volume fell 3% on a year-over-year basis. So pricing and average rate per contract made up for the difference.

On the earnings call, management noted that trading volume into Q2 were strong so far, up about 4%. While this was a key highlight of the quarter, the fact that volumes were down concerns me. It’s difficult to quantify and assess the sustainability of volumes over the long-run, but unquestionably the last few quarters have marked a deceleration in the company’s growth rate.

In terms of the positives, Q1’24 had ADV of 26.4 million contracts, which was the third-highest quarterly ADV in the company’s history. On the call, management cited positive momentum across its six asset classes, including varied opinions regarding Fed actions and the increasing need for duration management that should be beneficial to rates volumes and commodities in different markets.

Another positive note on the call was that management cited several new and recently launched product initiatives. They also announced plans for a new U.S. credit futures based on Bloomberg corporate bond indexes that will be launched in June.

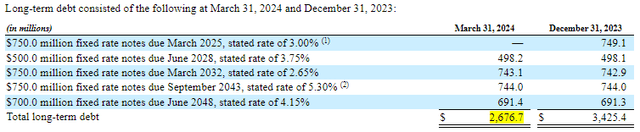

From a balance sheet perspective, CME Group looks to be in strong financial shape. Looking at the company’s bank debt, there are no maturities coming due until 2028, and most of the maturities are laddered. With an AA- rating my S&P, the company has an investment grade rating that allows it access to low cost debt, given the nature of the business model and clean financials. With $2.68 billion in long-term debt against $3.85 billion in LTM EBITDA, the company has a Debt to EBITDA ratio of 0.7x, or 0.3x on a Net Debt to EBITDA basis, given its $1.56 billion in cash.

Company Filings Company Filings

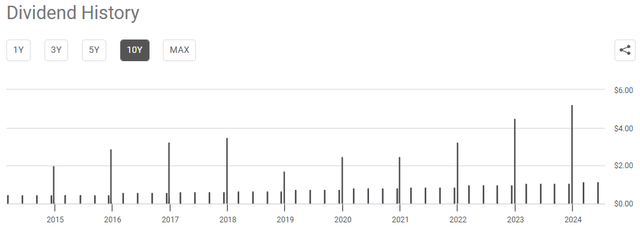

This robust balance sheet affords CME a way to return cash flow to shareholders. CME does this by repurchasing stock and paying a growing distribution. In the last four quarters, the company has repurchased $33.4 million worth of stock, an amount consistent year to year (source: S&P Capital IQ). On dividends, CME pays $1.15 each quarter, which equates to a 2.4% yield. It’s also periodically paid out special dividends, returning cash to shareholders when the cash pile gets large. As shown from the chart, these special dividends have become somewhat of a recurring feature about CME.

Seeking Alpha

Outlook

Overall, I think management has done a really good job in running CME. Capital allocation is shareholder-friendly and CME has a what looks to be a steady business. However, that could change with a new entrant into the market.

Earlier this year, BGC Group announced that it had received approval for FMX Futures Exchange to enter the U.S. interest rate futures market. Previously, CME essentially operated as a monopoly in the space, completely dominating the market. It’s one of the reasons why CME has been able to sustain 70% EBITDA margins, which is even higher than companies like Visa (V) and Mastercard (MA).

This presents CME with a few problems. Firstly, it’s clear that regulators are upset with CME’s monopoly in the rate market. As I highlighted in the recent results, most of the top-line growth comes from pricing increases, rather than volume increases. Another issue is that CME doesn’t invest in R&D to sustain its moat. This makes it hard for CME to fend off market entrants in the absence of regulatory protection. After all, a moat is only as defensible as the upkeep and innovation that fortifies it; neglect invites breaches.

Company Filings

With FMX entering the U.S. interest rate futures market, I expect they will compete head-to-head with CME in its flagship futures contracts. Aligned with several partners, including what are likely customers of CME, FMX should hit the ground running later this summer. Key partners include Bank of America, Barclays, Citadel Securities, Citi, Goldman Sachs, J.P. Morgan, Jump Trading Group, Morgan Stanley, Tower Research Capital, and Wells Fargo. All of them have become equity owners of FMX. None of them are small by any means, so this poses a real risk to CME.

In the announcement upon approval of FMX getting CFTC, Howard Lutnick, Chairman and CEO of BGC Group, had this to say:

Similar to U.S. interest rate futures, the wholesale U.S. Treasury market had historically been dominated by the CME until we launched Fenics UST. Since our launch, Fenics UST has grown rapidly, reaching 25 percent market share during the third quarter of 2023, up from 18 percent only a year ago2. We will execute the same playbook with our FMX Futures Exchange.”

Overall, I wouldn’t be surprised to see customers leave CME unless the company slashes prices. If they don’t, they risk losing volume to FMX. If they do, margins will erode hampering profitability. Either way, it’s a catch twenty-two for CME with respect to what happens on its bottom line.

Another issue is CME’s value proposition may not prove to be as strong as FMX. While CME group has credibility, a first-mover advantage, and is entrenched within the system, FMX has a very compelling offering with strong partners and state-of-the-art technology. FMX is likely to keep pricing competitive in order to win business from CME. If FMX can ultimately win over key asset manager participants (a very stick part of CME’s customer base), they’ll likely develop a sizable place in the market.

Valuation

Even if earnings don’t come down for CME, I do think that the multiple for CME could come down if their moat erodes. If FMX takes market share (volumes) away from CME, this weigh on long-term growth, given a smaller share of volume growth going forward.

In some respects, this has already happened in the payments space when new technology-enabled entrants like Toast (TOST), Ayden, and Stripe took share away from traditional global payments companies like Fidelity National (FIS) and Fiserv (FI). The risk isn’t imminent overnight, but it’s something to watch for as potential (or current) investors of CME.

When looking at the historical valuation for CME Group, the company has traded within a range of 12.1x to 27.9x. Compared to the historical average multiple of 19.1, CME trades below the ten-year average at 17.3x. In my view, this likely warranted, but there could still be downside in the multiple from here.

Author, based on data from S&P Capital IQ Author, based on data from S&P Capital IQ

Ultimately, one has to hand it to CME. It’s been in a strong position for a long-time operating in a niche that went without serious competition for decades. With a promising competitor coming for their lunch, I’d be cautious on CME going forward. The latest quarters have highlighted limited volume growth, and with pricing increases unlikely to continue at the rate they have been, I believe that CME deserves to trade at a discount to its historic multiple.

As one would probably guess from reading this, I wouldn’t be a buyer of CME shares and would like to wait and see how the next few quarters unfold and hear how CME plans to tackle the challenges that lie ahead for them. However, for those that own the stock, that doesn’t necessarily mean investors should sell.

At present, the December $200 calls are selling for $10.20. By selling covered calls against positions, investors can effectively get an 11.1% annualized yield on the stock, while collecting their dividends and participating in modest upside. So if I owned the stock today, I’d consider this options strategy to mitigate downside risk.

Read the full article here

")

")

")