(NASDAQ:CGBD)")

")

Introduction

Eagle Point Income (NYSE:EIC) is an investment company focusing on CLO debt, and as explained in a previous article, Steven Bavaria is an authority on this sector and I would strongly recommend you to re-read his October 2022 article which I think offers one of the best explanations how you should look at CLO debt. I have a long position in EIC’s common shares, but I have a much larger position in the 2026 term preferred shares (NYSE:EICA) where the yield to maturity is quite appealing given the additional layer of safety. I’m also looking to establish a long position in the other preferred securities of Eagle Income which all have a firm maturity date. This article follows up on previous coverage of Eagle Income as my previous article discussed the FY 2023 results.

A strong net investment income result means the preferred dividends are very well covered

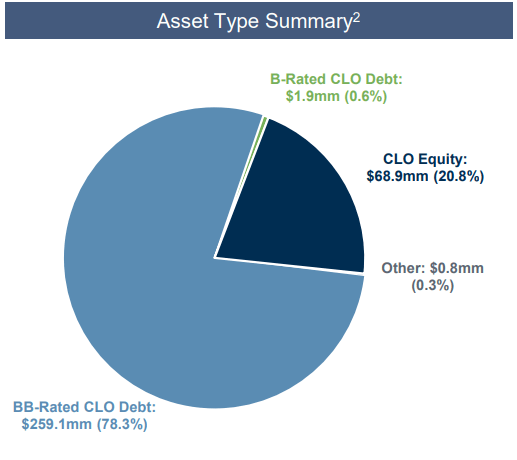

Unlike Eagle Point Income, which I discussed in another article a few weeks ago, the majority of Eagle Point Income’s portfolio consists of CLO debt. As you can see below almost 80% of Eagle Income’s portfolio consisted of CLO Debt with a BB rating and this obviously ranks senior to the positions in CLO Equity. Of course the risk/reward ratio takes this into consideration as EIC reports an effective yield of 11.9% on CLO debt and almost 17% on CLO Equity.

EIC Investor Relations

As I have a pretty sizable position in the preferred shares issued by Eagle Point Income, I will mainly focus on the performance from the perspective of a preferred investor. That being said, I also have a small long position in the common equity of Eagle Point Income, but my position in the preferred equity is about 20 times larger and thus more important in my decision-making process.

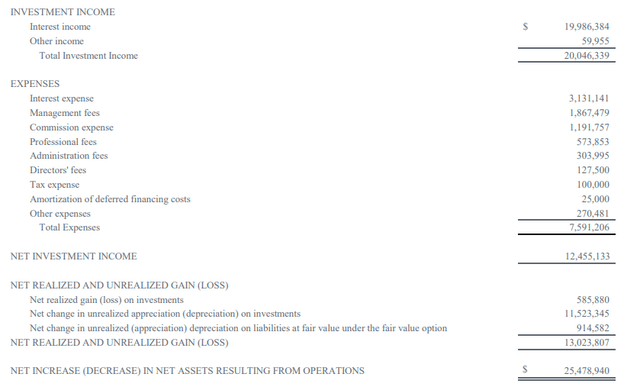

Looking at the financial results of Eagle Point Income in the first half of this year, the CEF reported total investment income of just over $20M. As you can see below, the total amount of operating expenses came in at $7.6M, resulting in a net investment income of $12.5M.

EIC Investor Relations

There are two elements I’d like to draw your attention to. First of all, all the “interest expenses” are related to the preferred equity. As Eagle Income has issued term preferred shares (with a firm maturity date), the term preferreds are considered a liability, and that also means the preferred dividend payments are seen as an “interest expense.” So looking at the $12.5M investment income, this already includes the $3.1M in preferred dividends based on the H1 result.

This means the net investment income excluding the preferred dividends was approximately $15.6M, and this indeed means the CEF only needed about 20% of its net investment income to cover the preferred dividend payments. That’s a good ratio. Keep in mind though that EIC issued the Series C preferred shares during the first semester which means that the full impact of those preferred dividends will be felt in the second half of the year (but of course, the interest income should increase as well as the proceeds of the offering were put to work throughout the second quarter).

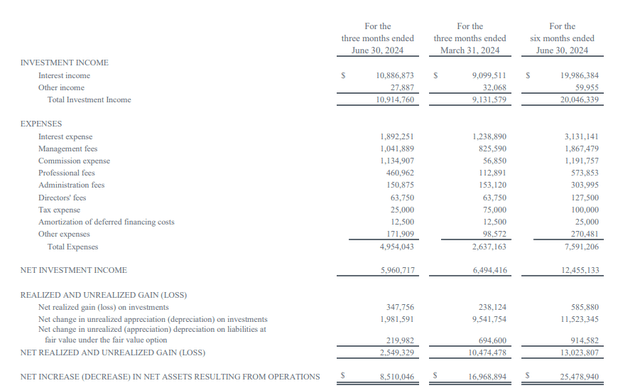

The impact will be noticeable but won’t be alarming. If we look at the Q2 results, we see a total investment income of almost $11M and a net investment income of almost $6M. While that’s lower than in the first quarter of this year, keep in mind there was a $1.1M additional commission expense related to the newly issued preferred shares. So, excluding the impact of those commission fees, the net investment income likely would have increased by almost 10% on a QoQ basis.

EIC Investor Relations

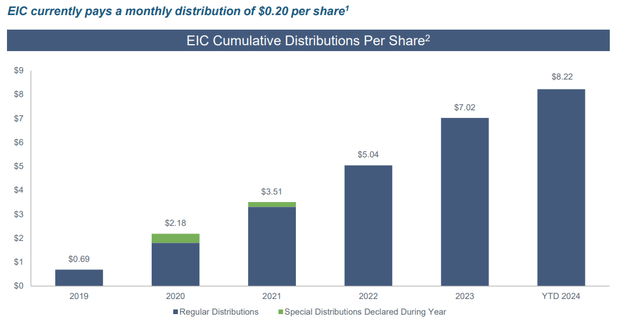

Meanwhile, adjusted for the commission expenses, the payout ratio for the preferred dividends remains fine, with about 27% of the net investment income required to cover the preferred dividend payments. The common stock currently yields about 15.4% as the CEF pays a monthly dividend of $0.20, but I expect the dividend payments to stagnate or even to decrease again as the interest rate on the financial markets is starting to decrease.

EIC Investor Relations

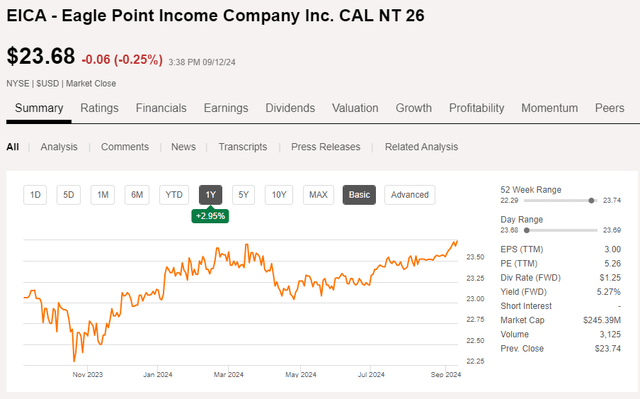

There currently are three series of term preferred shares outstanding, trading with (EICA), (EICB) and (EICC) as ticker symbols.

Stockwatch.com

All term preferred shares offer approximately the same 7.75%-8% yield, and even EICA offers a yield in the high 7% range, considering it’s trading at a discount to par.

Seeking Alpha

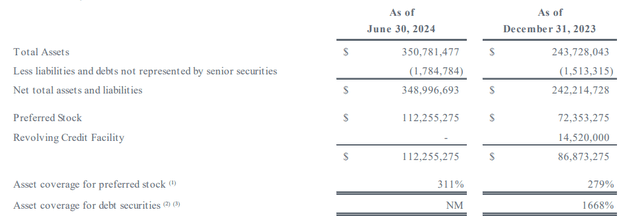

As EICA is the first series of preferred equity that will mature (in October 2026, to be precise), it offers the lowest risk due to the “seniority by maturity” rule. That being said, considering CEF rules require the CEF to offer a coverage ratio of at least 200% for the preferred shares, I’m quite confident Eagle Point Income will be able to meet its commitments. As you can see below, at the end of June, the coverage ratio stood at a very healthy 311%.

EIC Investor Relations

And as the CEF continues to issue common stock (it issued 4.6M shares for total proceeds of $71M during the first half of the year), I expect the asset coverage ratio to remain very robust.

Investment thesis

My focus on EICA is purely based on fiscal reasons, as my tax rate on capital gains is lower than on preferred dividend payments. That, of course, is a personal situation and won’t be applicable to all investors. That being said, as we’re getting close to the maturity date of EICA, I will (have to) start to add duration to my portfolio and I think EICC meets my criteria best. The preferred dividend is a bit higher than what EICB offers, while the maturity date is further down the road.

I currently have a very sizable position in EICA and a small position in EIC’s common stock. I will likely add EICC to my portfolio, but this likely won’t happen within the next 72 hours.

Read the full article here

")

")

")

")