")

The Q2 2024 results gave continuity to what was discussed in my previous article on East West Bancorp (NASDAQ:EWBC). In fact, the dividend continues to grow fast and CRE loans are struggling to increase. In contrast, C&I loans and Residential loans are getting an increasing share of the entire loan portfolio. These trends will presumably continue throughout 2024; perhaps even into the early 2025.

Loans and securities portfolio

For 2024 as a whole, loan growth is expected from 3-5%, thus quite low. The deteriorating economic environment, coupled with the desire to avoid exposure to risky CRE loans, has reduced growth expectations.

East West Bancorp, Inc. (EWBC) Q2 2024 Earnings Call

Compared to the previous quarter, loan growth was $775 million, driven mainly by C&I and Residential mortgage, +$525 million and +$217 million respectively; as mentioned, CRE (ex. Multifamily) experienced a decline of $57 million.

According to management’s expectations, we cannot expect much from CRE loans in the coming quarters. There will be a strong focus on long-standing customers, but for new ones, optimism does not filter through: EWBC has tightened its credit standards given the uncertain macroeconomic environment.

Different talk for Residential and C&I, where especially the former are expected to rise sharply as well as in the last quarter:

Residential growth will continue to be a consistent contributor to the growth at about the pace it’s been here over the first half of the year into the second half of the year. Our pipelines already here in the third quarter would support that. I don’t see that necessarily shifting much in our outlook. C&I will be, as was today, this quarter, is a prominent contributor to the quarter. It will moderate, but it could also still be a good contributor to the overall growth.

CFO Christopher Del Moral-Niles, EWBC conference call Q2 2024.

If the Fed reduced rates this could boost demand for loans, but management believes 2-3 cuts of 25 bps would not move the situation much.

We don’t think a rate cut or two will make too much difference to the outlook and those people that are coming to us pursuing the American dream of home ownership are not going to be turned away or more excited necessarily by give or take 25 basis points.

CFO Christopher Del Moral-Niles, EWBC conference call Q2 2024.

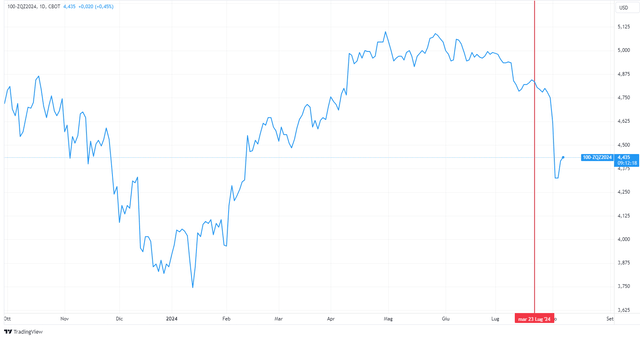

However, there is an important point to be made. These words are about 2 weeks old; they are quite recent but do not take into account what just happened because of the yen carry trade and the rising unemployment rate.

TradingView

Since then, the market has discounted about 2 more rate cuts, but there are those who expect as many as 5-6 total cuts by the end of 2024. In other words, if until a few months ago we were not even sure if the Fed cut rates in 2024, today market sentiment has changed completely.

So while management believes that a 50 bps reduction in the Fed Funds Rate in 2024 will not make a difference in terms of Residential loan growth, a 100-125 bps reduction would be a game changer. Anyway, at that point one would need to understand why the Fed is cutting rates so quickly; typically panic cutting is associated with a recession on the horizon.

Finally, the recent increase in the yield on the securities portfolio should be noted.

East West Bancorp, Inc. (EWBC) Q2 2024 Earnings Call

As you can see, it reached 3.93%, up sharply from previous quarters. This anomalous result stems mainly from management’s willingness to invest its liquidity in low-risk government bonds. In fact, cash decreased by $1.80 billion, while the securities portfolio increased by $1.70 billion.

Since low-risk securities have been added, this move will not have such a negative impact on capital ratios. Cash is always the safest and most important asset for increasing CET1, but 93% of the securities in the portfolio have risk coefficients between 0% and 20%, so they are very low risk.

This move will have little impact on capital ratios but will give a boost to the rise of NIM, which as we shall see is rather struggling.

Deposits and NIM

East West Bancorp, Inc. (EWBC) Q2 2024 Earnings Call

Non-interest-bearing deposits continue to fall, and this is a negative sign, since some peers have already experienced a reversal of the trend. They went from $15 billion to $14.70 billion in just three months, so they have not yet reached the bottom.

EWBC is still too dependent on time deposits and money market deposit accounts, both of which are quite expensive. Personally, I would have expected an improvement over the previous quarter, which there was not. As a result, the average cost of deposits soared again and reached l 2.96%, 12 bps higher than the previous quarter.

East West Bancorp, Inc. (EWBC) Q2 2024 Earnings Call

For the umpteenth time, NIM is declining, although it remains quite high. As mentioned earlier, the investment of some of the cash in government bonds will probably help the recovery of the NIM, but what matters most will be the decline in the average cost of deposits. Until there is a change in the trend, NIM cannot improve. By the second half of 2024, we can expect NIM to still contract, while NII may see light at the end of the tunnel. In any case, compared with FY2023, the NII in FY2024 is expected to decline between 2-4%.

Dividends and valuation

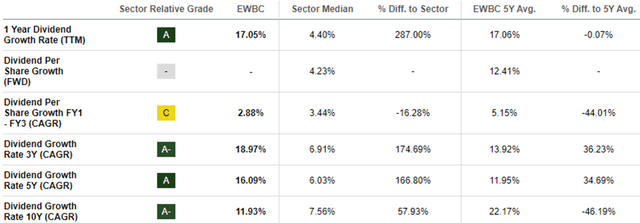

In my last article I mentioned EWBC’s ability to steadily increase the dividend, and this remains one of its strengths.

Seeking Alpha

Over multiple time frames, it has largely outperformed the growth of peers, proving to be a reliable dividend growth company. By the way, the dividend payout ratio is still low, about 25%, so the dividend has good sustainability.

The only negative note is the dividend yield, about 2.85%. This is not high enough to guarantee right away a sound passive income, which is why some investors may discard EWBC. For those who have a long-term horizon and rely on dividend growth, they could end up with a large dividend yield on cost in 10 years. Assuming the same growth rate over the next 10 years, by buying EWBC today, an investor would get a dividend yield on cost of 8.79%.

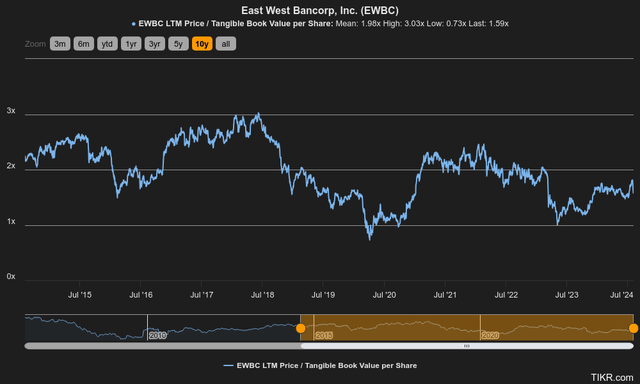

As for valuation, so far, I have considered EWBC as a buy, but I think it is more appropriate to consider it a hold after the increase in price per share in recent months.

TIKR

As you can see from this image, the Price/TBV per share is 1.59x, lower than the 10-year average of 1.98x, but not low enough to be a buy. After the recent collapse of the global stock markets, nervousness in the financial markets has become a hot topic of discussion and is generating quite a few doubts about global economic growth. After all, the unemployment rate is rising, the Sahm Rule Indicator has crossed the 0.50 threshold, and the spread between 10-2 year Treasury yields has turned positive for a few hours.

We are in a complicated phase and I would not buy EWBC unless at a fairly high margin of safety, which I don’t think is there at the moment.

Conclusion

EWBC is an excellent bank, well capitalized and with a positive dividend track record.

East West Bancorp, Inc. (EWBC) Q2 2024 Earnings Call

Although the expected growth for 2024 is not exciting, from a dividend perspective, EWBC may prove to be a good investment. In addition, management is also used to remunerate shareholders through buyback. In the last quarter, 560,000 shares were purchased and another $49 million remains available. In the last few days, the price per share has dropped about 12%, so management can take advantage of this drop to make the buyback more effective.

There is no shortage of remuneration for shareholders, but the prospects for capital gains could be subdued in the event of a major economic slowdown in the United States. Since EWBC does not have a high enough margin of safety, as well as still declining profitability, I believe that at the current price a hold rating is more appropriate.

Read the full article here

")

")

")

")

")

")