")

Please note all $ figures in $CAD, not $USD, unless otherwise stated.

Introduction

I last covered Enghouse Systems (OTCPK:EGHSF) (TSX:ENGH:CA) in March 2024. At the time, I issued a ‘buy’ rating on the company, noting that the market had reacted overly negatively towards a weak quarter, but a medium term trend of steadily improving financials and with an improving balance sheet.

With the company just having reported its Q3’24 results on Sept 5, I wanted to come back to my original investment thesis to see where things stand with respect to Enghouse Systems. In the latest quarter, management was incrementally positive with indications that organic growth weakness could be due to customers migrating to the cloud. Despite this, offering on-prem licenses is improving customer retention and winning customers from competitors. Management also hinted that they may be more aggressive with share repurchases in the near-term.

In this article, I’ll dissect the latest quarterly results in detail, provide my outlook for the company, and what I see as the key risks. I’ll also provide my thoughts on valuation and why I continue to view the company’s shares as attractive today.

Company Overview

I won’t spend too much time explaining Enghouse’s business model (as I already discussed much of this in my prior article in March). To recap, Enghouse is an enterprise software company that targets unique and specific verticals. Founded in 1984, the Enghouse of today specializes in providing advanced software solutions designed to improve customer interactions and streamline operations for businesses across various industries. Enghouse’s business model revolves around two core areas: communications solutions and public safety and government services.

In the communications sector, Enghouse offers software that helps businesses manage customer interactions across multiple channels, including phone, chat, and social media. Their solutions are particularly valuable for contact centers, enabling them to enhance customer service, increase efficiency, and integrate seamlessly with other business systems. On the other hand, Enghouse’s public safety and government software supports emergency response systems and governmental operations, including 911 call handling and other critical communication needs.

The company’s offerings include both cloud-based and on-premises solutions, catering to a wide range of organizations from small businesses to large enterprises. Enghouse’s growth has been bolstered by strategic acquisitions, allowing it to incorporate new technologies and expand its market presence. With a strong global footprint and a consistent track record of profitability, Enghouse Systems continues to be a key player in the technology sector, focusing on enhancing communication and operational efficiency.

Q3’24 Results and Outlook

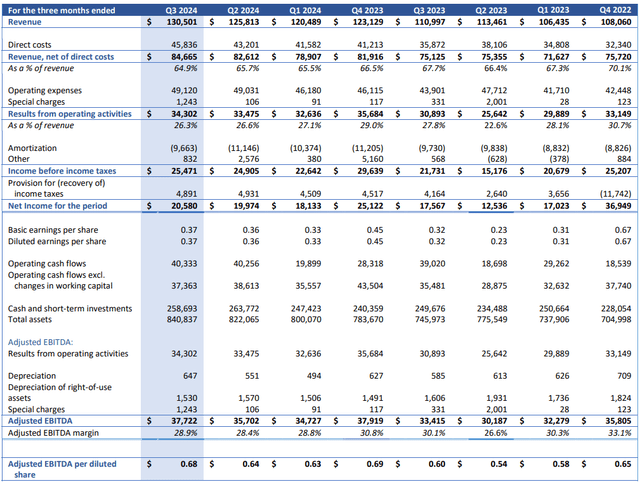

When looking at the latest quarterly results for Enghouse’s Q3’24 results, the company reported revenues of $130.5 million during the quarter, up 17.6% compared to last year. On the recurring revenue side (an important figure to look at for SaaS-based companies), sales increased 22.8% to $88.8 million.

Overall, my takeaway was that this was a strong quarter for Enghouse. On the top line, sales revenues beat analyst consensus estimates by $0.8 million. And on EPS, adjusted earnings per share came in 3 cents above estimates, clocking in at $0.39.

Q3’24 Results (Company Filings)

As was consistent with last quarter, adjusted EBITDA didn’t grow at the same pace as revenues, with adjusted EBITDA growing just 12.9%, coming in at $37.7 million. This was a direct result of EBITDA margin contraction, as EBITDA margins contracted 120bps to 28.9% this quarter. As I mentioned in my initial piece on Enghouse, this has been a concern for investors for sometime, and negative organic growth (perhaps due to cloud migration) certainly hasn’t helped.

On the company’s earnings call, management indicated that the decline in Software Licenses revenue was largely due to customers migrating to the cloud, which in my view might imply that investors’ estimates of IMG organic growth may be largely due to the cloud migration. To me, I see an angle to view this as a slight positive, as it may suggest that Enghouse’s SaaS solution is successfully retaining customers. Customer churn is consistent and there has been little pricing pressure so far. In addition, management also noted that declines in Vidyo are largely behind them.

Another important theme during the quarter was Enghouse benefiting from on-prem licenses. Despite the cloud success, management attributed the sequential growth this quarter partly to it offering perpetual license options to its customers. Enghouse also claims it has helped with customer retention and competitive wins. Nonetheless, I think a higher mix of recurring revenue is favorable given higher stability, visibility, and long-term economic value. Going forward, a higher mix of recurring revenue is positive for adjusted EBITDA margins, and therefore the company’s valuation.

With margins in the 28% range, I think it could be possible to get back to the low 30% level. Why? When we consider the integration of assets from the acquisition of SeaChange ($30.8 million transaction), and other operational levers the company can pull on through this transaction, margins are likely not where they could be. In addition, from an overall company perspective, Q3 is typically not Enghouse’s strongest quarter (Q4 generally sees more normal margins) and so some seasonal factors are at play. As we move into Q4, I think we might see improved performance and efficiency gains, especially with management commenting that they are focused on several key areas including cost management, operations, and demand generation, factors I think should be accretive to margins in the quarters ahead.

Historically, acquisitions (like SeaChange) have situated Enghouse as a serial acquirer with a track record of creating value for shareholders. Some of its acquisition criteria and strategy have typically been to look for positive cash flow generation businesses, a track record of recurring revenue (or some component of re-occuring sales), and mission critical solutions with high barriers to entry. From a financing perspective, the company targets a cash-on-cash payback within 5-7 years (implied IRRs above 15%) and Enghouse typically avoids diluting shareholders through new equity issuances.

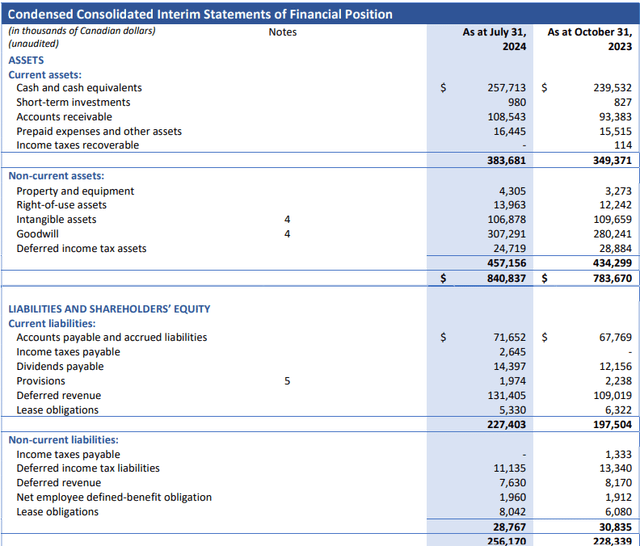

To fund its acquisition strategy going forward, I think Enghouse currently has the balance sheet in place to continue to accelerate the pace of M&A. For one thing, the company had a cash balance of $259 million after spending $30.8 million on the acquisition of SeaChange, $14.4 million on dividends, and $1.8 million on share buybacks.

With no debt on the company’s books, I think more share repurchases are possible. Right now, even though the company has cash to make deals (and a very flexible balance sheet), valuations in the M&A market remain above management’s preference, after considering high levels of leverage. Given the stock is trading at historically low valuations, management hinted that they may favor share repurchases. With free cash flow of $118 million over the next year, I suspect about half ($57.6 million) will be used for the dividend with the rest available for repurchase. Against the company’s market cap of $1.7 billion, the company could buy as much as 3% of its market cap per year, assuming management is willing and able to execute share repurchases at the current stock price. With shares where they are right now, I suspect this to be something the company is thinking about very strongly.

Balance Sheet (Company Filings)

Valuation and Wrap Up

I continue to think that Enghouse is one of the cheapest names in midcap/small cap software in Canada today. At 20.2x P/E and 12.0x EV/EBITDA, the company trades well below its historical ten-year multiple of 17.6x EV/EBITDA. While some of this warranted (a slow down in growth rate, a more uncertain outlook with respect to AI disruption and a potential slowdown in M&A), there’s a lot to like at Enghouse. Margin expansion and more share repurchases at a cheap multiple signify that shares could be due for a re-rating once fears blow over.

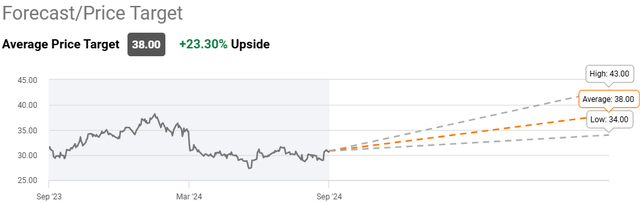

Analysts seem to agree. Based on the three sellside analysts who cover the stock, all have price targets substantially higher than the current price. The average price target of $38.00 implies about 23.3% upside potential, in addition to the company’s 3.4% dividend yield. With total return potential of 26.7%, analysts seem to be pretty bullish on the company. In addition, with just three analysts covering the stock, there’s certainly room for Enghouse to gain a wider following as it currently rather undercovered with a market capitalization of just $1.7 billion.

Seeking Alpha

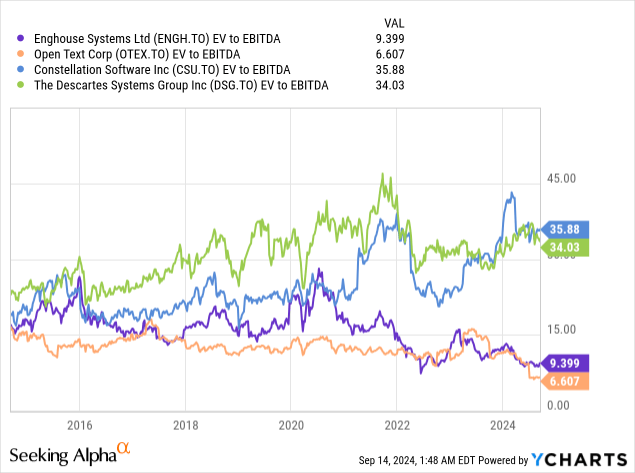

Compared to other Canadian software peers, Enghouse looks attractive on a relative basis when comparing its trailing twelve month and forward multiples. As shown below, compared to peers like Descartes (DSG:CA), Constellation Software (CSU:CA), and Open Text (OTEX:CA), Enghouse’s valuation is a mere fraction of what larger software company’s trade at. While Enghouse may not be of the same quality as some of these higher multiple stocks (shorter track record and lower margins), the discount has certainly widened since my initial piece and I think the gap has become far too wide. As such, shares of Enghouse seem compelling when stacking it up to peers.

In conclusion, I think Enghouse’ latest third quarter results were pretty good. Despite challenges such as margin contraction and some potential shifts in customer preferences towards cloud solutions, Enghouse has demonstrated its adaptability by leveraging on-premises licenses to enhance customer retention and fend off competition. The potential ramp up in share repurchases as indicated by management should be viewed positively, especially with a mounting cash position and non-existent debt. With shares currently trading at historically low valuations relative to its peers as well as its historical multiple, I think Enghouse presents an attractive investment opportunity. For investors looking for a combination of both growth and income, I think Enghouse makes for a compelling candidate.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here

")

(NASDAQ:CGBD)")

")

")