")

Earnings of First BanCorp. (NYSE:FBP) will most probably continue on an uptrend on the back of low loan growth. This loan growth will likely undermine the negative effects of margin pressure next year. Overall, I’m expecting the company to report earnings of $1.83 per share for 2024, up 7%, and $1.89 per share for 2025, up 3% year-over-year. Compared to my last report on the company, I’ve raised my earnings estimate for this year because the expenses reported so far this year have been much better than expected. My valuation analysis shows that First BanCorp. is offering a small price upside and a modest dividend yield. Based on the updated total expected return, I’m upgrading First BanCorp. to a buy rating.

Loan Growth to be Lower This Year Compared to Last Year

First BanCorp’s loan portfolio grew by 0.7% during the second quarter (2.7% annualized), which is not too bad considering the company’s history. Moreover, the first half’s loan growth is not too far behind my estimates given in my last report on the company, which was issued back in December 2023.

The management appeared optimistic about loan growth in the latest conference call and mentioned that the pipelines were healthy. Further, there was some delay in construction funding during the first half, which the management expected to close in the second half of the year. Overall, the management is expecting mid-single-digit loan growth this year.

In my opinion, the management’s target is achievable, especially because of upcoming interest rate cuts which should propel credit demand, especially in the residential mortgage segment. Residential loans make up 23% of FBP’s total loans, so an uptick in this segment will have a material effect on the average loan balance.

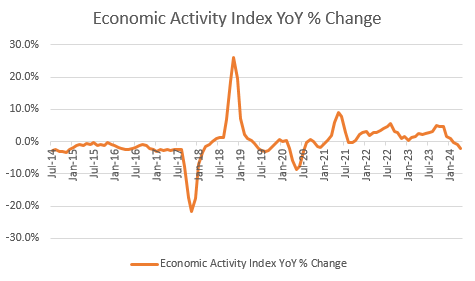

However, the current local economic environment is not as conducive to loan growth as it was last year. Puerto Rico’s economic activity has been on a downtrend so far this year, as shown below. (Data taken from the Economic Development Bank for Puerto Rico).

Economic Development Bank for Puerto Rico

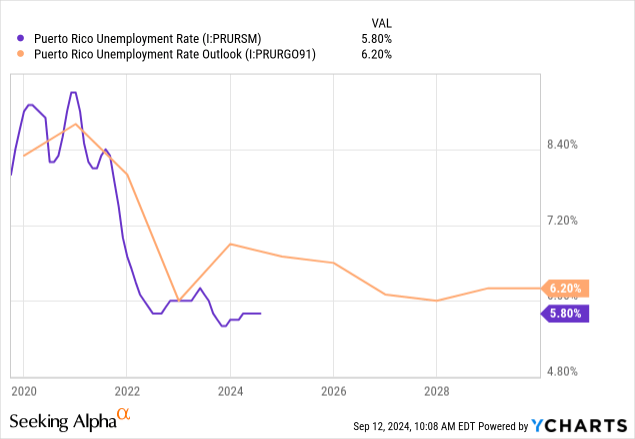

Further, the region’s unemployment has slightly worsened over the last few months.

Considering these factors, I’m expecting loan growth to remain below last year’s level. I’m expecting the loan portfolio to grow by 1% every quarter through the end of 2025. My loan balance estimate is not much changed from my previous estimate given in my last report on the company.

I’m expecting deposits to grow in tandem with loans. The following table shows my balance sheet estimates.

| Financial Position | FY19 | FY20 | FY21 | FY22 | FY23 | FY24E | FY25E |

| Net Loans | 8,887 | 11,442 | 10,827 | 11,305 | 11,931 | 12,385 | 12,888 |

| Growth of Net Loans | 2.1% | 28.8% | (5.4)% | 4.4% | 5.5% | 3.8% | 4.1% |

| Other Earning Assets | 2,398 | 4,926 | 6,658 | 6,086 | 5,633 | 5,410 | 5,519 |

| Deposits | 9,348 | 15,317 | 17,785 | 16,143 | 16,556 | 16,861 | 17,546 |

| Borrowings and Sub-Debt | 854 | 924 | 684 | 934 | 662 | 668 | 682 |

| Common equity | 2,192 | 2,239 | 2,102 | 1,326 | 1,498 | 1,693 | 1,900 |

| Book Value Per Share ($) | 10.1 | 10.3 | 9.9 | 6.9 | 8.5 | 10.2 | 11.5 |

| Tangible BVPS ($) | 9.9 | 9.9 | 9.6 | 6.6 | 8.2 | 9.9 | 11.2 |

Source: SEC Filings, Earnings Releases, Author’s Estimates (In USD million unless otherwise specified)

Margin to Rise Further Before Dropping Next Year

The net interest margin improved substantially in the second quarter of the year as it grew by six basis points. During the first quarter, it had grown by only two basis points, while last year it had actually declined by 23 basis points. The management believes that the margin reached an inflection point in the first quarter, and it should expand from now onwards, as mentioned in the conference call. The management’s confidence comes from re-pricing opportunities available in the balance sheet as low-yielding securities will be maturing soon.

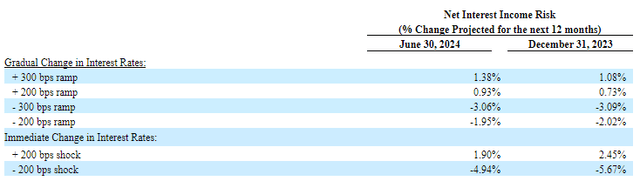

However, once these opportunities are over, I’m expecting the margin to face downward pressure from interest rate cuts. The results of the rate sensitivity simulation model given in the 10-Q filing show that 200-basis points gradual decline in interest rates could decrease the net interest income by 1.95%.

2Q 2024 10-Q Filing

Considering these factors, I’m expecting the margin to rise by eight basis points in the second half of this year and then drop by four basis points next year.

Lifting My Earnings Estimate

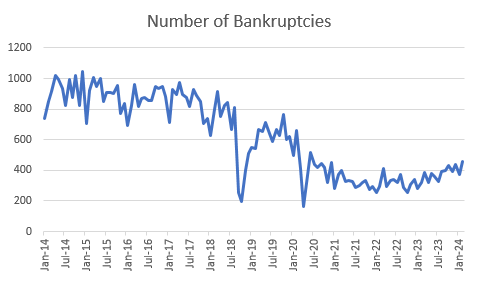

First BanCorp’s expenses have been much below my expectations so far this year. Therefore, I’ve decided to reduce my estimates for both non-interest expenses and provision expenses for loan losses. I’m assuming that the future provision expense to total loan ratio will be near the last five-year average. There has been an uptick in bankruptcies in Puerto Rico since last year. Nevertheless, they are still quite low compared to previous years, as shown below.

Economic Development Bank for Puerto Rico

Further, I’m expecting the efficiency ratio to remain mostly unchanged from the second quarter’s level. The efficiency ratio is calculated by dividing the non-interest expenses by total revenue.

In addition, I’m assuming non-interest income will remain stable at the first half’s level. Based on these assumptions and outlook, I’m estimating earnings of $1.83 per share for 2024, up 7% year-over-year, and earnings of $1.89 per share for 2025, up 3% year-over-year.

In my last report on the company, I forecast earnings of $1.58 per share for 2024. I’ve raised my earnings estimate mostly because I’ve reduced my estimates for provision and operating expenses. The following table shows my income statement estimates.

| Income Statement | FY19 | FY20 | FY21 | FY22 | FY23 | FY24E | FY25E |

| Net interest income | 567 | 600 | 730 | 795 | 797 | 804 | 834 |

| Provision for loan losses | 40 | 171 | (66) | 28 | 61 | 50 | 52 |

| Non-interest income | 91 | 111 | 121 | 123 | 133 | 131 | 132 |

| Non-interest expense | 378 | 424 | 489 | 443 | 471 | 481 | 496 |

| Net income – Common Sh. | 164 | 100 | 277 | 305 | 303 | 304 | 313 |

| EPS – Diluted ($) | 0.76 | 0.46 | 1.31 | 1.59 | 1.71 | 1.83 | 1.89 |

Source: SEC Filings, Earnings Releases, Author’s Estimates (In USD million unless otherwise specified)

Hurricanes Remain the Only Major Risk Factor

Due to its location in Puerto Rico, the biggest source of risk for First BanCorp. is natural disasters. As we’re in the midst of the hurricane season, this risk is currently elevated. Another material source of risk is the securities portfolio, which has a sizable amount of unrealized losses. As mentioned in the 10-Q filing, these unrealized losses on the Available-for-Sale securities portfolio amounted to $637.49 million, which is around 43% of the total equity book value. Nevertheless, I’m not worried about the securities portfolio because the upcoming interest rate cuts will reverse most of these unrealized losses.

Apart from the above, the company’s riskiness is muted. The loan portfolio’s credit risk is low. Non-accrual loans made up just 0.78% of total loans at the end of June. Further, the deposit book is low risk. As mentioned in the earnings presentation, First BanCorp. had a total available liquidity of approximately $6.0 billion, which is around 1.3 times the uninsured deposits.

Upgrading to a Buy Rating

First BanCorp. is offering a dividend yield of 3.2% at the current quarterly dividend rate of $0.16 per share. The earnings and dividend estimates suggest payout ratios of 35% for 2024 and 34% for 2025, which are slightly higher than the last five-year average of 30%. Therefore, I’m not expecting an increase in the dividend level.

I’m using the peer average price-to-tangible book (“P/TB”) and price-to-earnings (“P/E”) multiples to value First BanCorp. Peers are trading at an average P/TB ratio of 1.41x and an average P/E ratio of 15.59, as shown below.

| Symbol | Selection Criteria | P/E (“ttm”) | P/TB (“ttm”) |

| FBP | 10.78 | 2.23 | |

| EBC | Market Cap | 16.10 | 1.08 |

| FULT | Market Cap | 10.30 | 1.39 |

| ASB | Market Cap | 17.53 | 1.05 |

| TCBI | Market Cap | 24.45 | 1.09 |

| AUB | Market Cap | 16.65 | 1.90 |

| BPOP | Location | 13.55 | 1.57 |

| OFG | Location | 10.56 | 1.78 |

| Peer Average | 15.59 | 1.41 | |

Source: Seeking Alpha

Multiplying the average P/TB multiple with the forecast tangible book value per share of $9.9 gives a target price of $14.0 for the end of 2024. This price target implies a 29.1% downside from the September 11 closing price. The following table shows the sensitivity of the target price to the P/TB ratio.

| P/TB Multiple | 1.21x | 1.31x | 1.41x | 1.51x | 1.61x |

| TBVPS – Dec 2024 ($) | 9.9 | 9.9 | 9.9 | 9.9 | 9.9 |

| Target Price ($) | 12.0 | 13.0 | 14.0 | 15.0 | 16.0 |

| Market Price ($) | 19.7 | 19.7 | 19.7 | 19.7 | 19.7 |

| Upside/(Downside) | (39.2)% | (34.1)% | (29.1)% | (24.1)% | (19.1)% |

Source: Author’s Estimates

Multiplying the average P/E multiple with the forecast earnings per share of $1.83 gives a target price of $28.6 for the end of 2024. This price target implies a 44.9% upside from the September 11 closing price. The following table shows the sensitivity of the target price to the P/E ratio.

| P/E Multiple | 13.6x | 14.6x | 15.6x | 16.6x | 17.6x |

| EPS – 2024 ($) | 1.83 | 1.83 | 1.83 | 1.83 | 1.83 |

| Target Price ($) | 24.9 | 26.8 | 28.6 | 30.4 | 32.3 |

| Market Price ($) | 19.7 | 19.7 | 19.7 | 19.7 | 19.7 |

| Upside/(Downside) | 26.3% | 35.6% | 44.9% | 54.2% | 63.5% |

Source: Author’s Estimates

Equally weighting the target prices from the two valuation methods gives a combined target price of $21.3, which implies a 7.9% upside from the current market price. Adding the forward dividend yield gives a total expected return of 11.1%.

I last issued a report on FBP in Dec 2023, wherein I adopted a hold rating with a December 2024 target price of $16.7. I’ve raised my target price because I’ve increased my earnings estimate, and consequently the tangible book value estimate. Moreover, the peer multiples are higher now. Based on the updated total expected return, I’ve decided to upgrade First BanCorp. to a buy rating.

Read the full article here

")

")

")

")