")

Dear readers/followers,

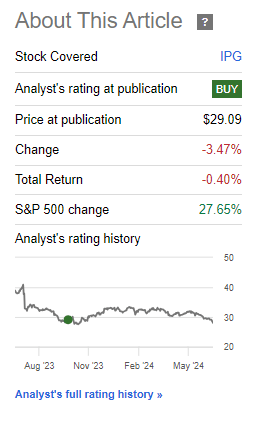

I’ve been covering Interpublic Group (NYSE:IPG) for a number of years, and also currently hold a small stake in the company from my last article in October of 2023. You can find that particular article here. I thought that I did pretty well in finding a valuation that shows some upside, and my proof for this is what the company has done since that time. This is despite the company, since that time, actually going “down” a little bit with a current total RoR of negative 0.4%.

Seeking Alpha IPG RoR (Seeking Alpha IPG RoR)

In this article, I intend to update my thesis for IGP, a strong advertising business with good fundamentals. While the company has solid fundamentals, including high operating margins and stable performance, it does face uncertainties in the rapidly evolving advertising landscape.

It’s these trends and these forecasts that I intend to look at in this article, and discuss and determine whether this company warrants another “BUY” rating, or if the time despite the lower price, has come to adjust it downward to a “HOLD” here.

Advertising has not been in a good spot for large parts of 2023 and some parts of 2024 either. This has especially impacted your traditional advertising businesses.

In this context, I’m talking about companies I’ve covered for a long time, like this one but also large companies like Omnicom (OMC) and Publicis Groupe (OTCQX:PUBGY). I cover more than just these, including some other European ones, but in this case, I’m going to be looking at Interpublic Group to see what’s happened and what we can expect going forward.

Looking at Interpublic Group and what upside remains.

I’ve previously been up for this company at a quite attractive amount/rate. Since selling back in early 2023, when I was up 25%, I bought back in October during the slump and have held my position since then.

IPG, to remind you of just what this company is and does, is a leading advertising company. It’s in fact one of the world’s largest advertising businesses, with almost 57,000 employees, BBB credit, and one of the longest operating histories in the entire sector. I’ve covered prior how the company is one of the most solid businesses in terms of margins, where it’s in the upper 85th percentile in the entire industry, delivering consistent ROIC net of cost of capital. It has not been negative in ROIC for over 10 years at this point (Paywalled GuruFocus link).

Advertising remains very COGS-heavy, and IPG generates a net profit margin of between 7-9%, rarely ever hitting that double-digit margin level.

However, despite this, the company is an industry outperformed with a tradition of outperforming. The company’s PR agencies and global creative networks continue to score “points” and awards here, winning 10 Grand Prix and 1 Titanium at the recent Cannes Lion Festival (Source).

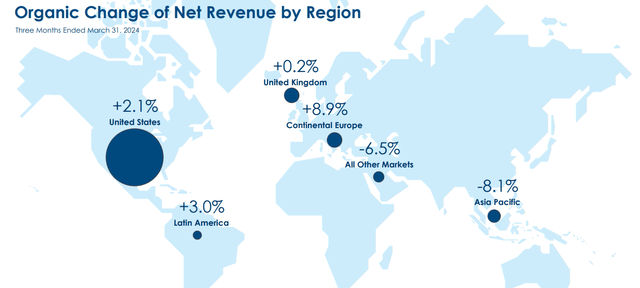

The latest set of results we have are the 1Q24. Despite challenges in the overall advertising industry, the company reported organic growth of 1.3%, with US-specific growth of 2.1% and international organic growth of around negative 0.5% – so the US segment was the primary positive contributor, with a net income of $110M and overall adjusted EBITDA margin of 9.4% with EBITDA at around $205M.

This was a positive result, all things considered, given the current trends in the overall market, even if net margin trends were actually down here.

Net revenue changes are as follows on a geographic basis.

IPG IR (IPG IR)

Again, some fairly clear trends in how things are developing here. What’s weighing the company down here?

We’re primarily talking SG&A. The company has both salaries as well as office costs under control, but general SG&A is up significantly, from 0.6% of the total to 1.7% of the total – this is an increase of almost 300%, with everything else being either stable or “down”. More on that later on.

The company’s debts are very solid and well-laddered. Nothing matures in 2024-2027 except a single senior note and some short-term debt, with over 90% of company debt with interest rates between 2.4% to 5.4% maturing in 2028-2048. A lot of time, therefore, the company shows the same sort of trends that have enabled it to survive for over 50 years.

IPG’s future focus lies on driving growth in dynamic media offerings, with a focus on healthcare companies. Obviously IT and data is being used, and the company is trying to deliver an “open architecture” sort of client solutions, with further investments in so-called “emerging opportunities”, categorized as follows:

IPG IR (IPG IR)

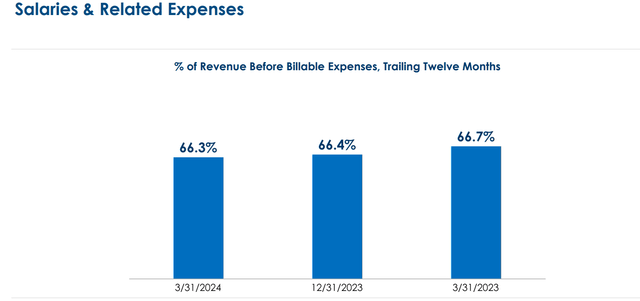

The company already has a strong history of expense management, proving that it can streamline operations and processes in a very solid manner. Salaries are a very good example – and when showcasing this, remember that this is despite salary inflation.

IPG IR (IPG IR)

Part of how the company has managed this is of course reduction in staff. We can see this clearly by looking at increased severance expenses, and some ever-so-slight increase in incentive expense, in order to get the employees they do want to keep in the company.

However, the fact that consulting and temp costs are actually down, means that this change in staffing was a positive, and a net efficiency gain without potentially losing much productivity in the process. Other expenses and Office are, as I said, also down 20 bps in less than a year.

This company has always had a good liquidity position and good fundamentals. This does not change as of this quarter either. With well over $3B available in cash, credit, and equivalents, IPG can “do what it needs to do”, within reason for its business and size.

The primary worries for a company like these are worries that arise with recurring frequency. We’re talking big accounts that companies like this need to defend with pricing and quality – Amazon (AMZN) is one of those for IPG. Companies such as IPG never discuss client specifics – but there are general questions that can be answered and highlighted, to illustrate how large client decisions impact a company like IPG. Obviously, if a large client decides to cut ad expenses or airtime, this impacts IPG in a non-trivial manner.

An example of this can be seen in the comment below from the latest earnings call.

I think what I would point out to you is it’s a significant and important ongoing relationship with us. So this is a client with whom we continue to do medical communications where public relations work globally. It was a sizable consolidation last year. We were obviously very proud of the talent that helped us win the creative assignment. And the client, as we understand it, and as I said, it’s what’s in the public domain, they’ve chosen to evolve their marketing model. They’re looking to rapidly drive change within their organization. So that’s a decision that we understand.

And in terms of trying to dimensionalize that for you or the magnitude of that shift, I mean, I think it’s fair to say our best estimate is baked into the remarks that we’ve shared with you in terms of expectations for the full year organic. So barring this news, I think we’d be very comfortable at the upper end of our target growth range. And now we’re telling you we think that will be challenging, but we’re still in the 1% to 2% band.

(Source: Philippe Krakowsky, IPG 1Q24 Earnings Call)

I view this as one of the major risks to any company in this space, and something that needs to be considered.

However, valuation remains by far the most interesting concern here.

IPG – The valuation is positive, the upside exists despite continued risk and is now larger than before

So, I think IPG is actually getting very interesting now, despite an expected downturn on the order of around 5% for this year.

Even with this downturn in earnings taken into account, we’re talking about the company trading below double-digit P/E, and at 9.62x normalized. This is all the while a yield of 4.7% that is very well covered here at a payout ratio of below 50% to adjusted earnings (Paywalled F.A.S.T graphs link).

Investing in a BBB company at this valuation can, if the company can manage a 3-4% upside annually and if there is nothing fundamental in the company’s forecast, nor a significant uncertainty to forecasts, only result in one sort of upside – and that is positive.

IPG is no different.

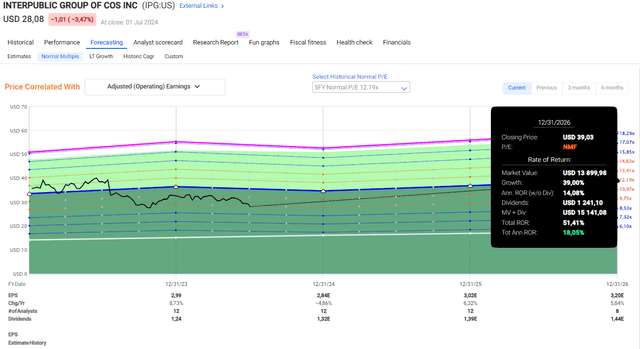

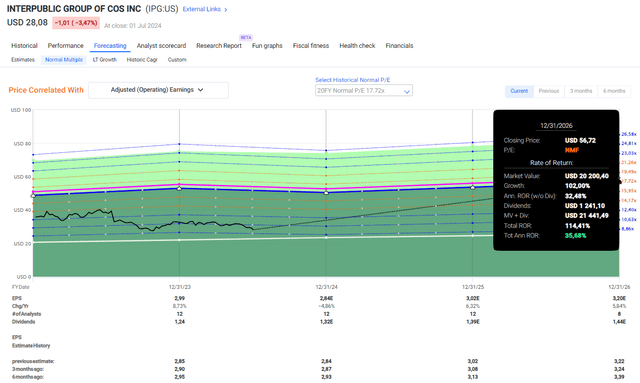

The 5-year average for the company lies at around 12x P/E which in itself is a discount, and where you can see an upside of 18.05% annually to a total upside of 51% at a share price target of $39/share.

IPG F.A.S.T Graphs Upside (IPG F.A.S.T Graphs Upside)

And $39/share isn’t even a very bullish or optimistic share price. If you were to look at the 20-year average for this company, you would find that IPG trades at 17.7x P/E, which would imply a triple-digit upside potential for this company.

F.A.S.T Graphs Interpublic Group Upside (F.A.S.T Graphs Interpublic Group Upside)

The truth I believe, lies somewhere in between, with significant upside possible any way you slice it here. I don’t believe triple digits in RoR is likely, but I believe the upside to be higher than 15-16%. Last time around, I gave the company a PT of $35/share based on relatively poor visibility but good earnings trends. I am now bumping this to $37/share due to better visibility for the client-related downturn, but believe the company could reach far higher than this.

Analyst-given valuation targets and estimates are a mixed bag. Currently, 12 analysts follow the company with a range of $31 on the low side to $39 on the high side, with an average of $36/share for the company as the current PT, and 8 analysts either at a “BUY” or an “Outperform” for the company here.

I agree for the most part with these estimates but choose to forecast higher in no small part due to a fairly significant (25%, with 10-20% margin of error) statistical historical likelihood of outperformance of more than 10%. I also want to point out that on a historical basis of 2 years, IPG never fails to hit its targets.

I believe that this creates a good enough circumstance for an investment in this company, and I am adding more shares to my position in the company here, at a price of close to $28/share.

My thesis is as follows for this company.

Thesis

I have the following thesis for IPG:

- This company is a “BUY” with a PT of $37, raised from my last article based on decent earnings and positive trends as well as increased visibility. There are advertising companies with better fundamentals, which is what led me to favor OMC above IPG historically, but IPG is still a good business with excellent valuation at this time. Given what other alternatives are available on the market today, I would be careful about going “too deep” into this company here, and my position will stay at 0.2%.

- I view the downside as unlikely given the market dynamics for companies such as this are continually positive.

- I continue to hold a very small position of shares and may add more here if we see more drops as of this month.

Remember, I’m all about:

- Buying undervalued – even if that undervaluation is slight and not mind-numbingly massive – companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn’t go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

The company also fulfills several of my investment criteria.

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap

- This company has a significant upside/is cheap based on conservative forecasts and historical valuation trends.

Due to IPG fulfilling every criterion I have for investment, I consider this company a “BUY” here and would add (and indeed, am adding to my position in the company) at this time.

Read the full article here

")

")

")