")

Work colleagues talking at a data center.

In investing, it isn’t uncommon for the fundamentals of a business to not line up with share price performance. This is because, at any given time, market sentiment can overshadow a company’s fundamentals.

Iron Mountain (NYSE:IRM) is one of the latest cases of what I mean. When I last covered the stock with a hold rating in February, I already thought the stock price was ahead of the fundamentally justified valuation.

Don’t get me wrong: The REIT makes up 1.5% of my total portfolio value and is my 18th-biggest holding. I liked IRM’s accelerating growth prospects. The improving balance sheet was another plus at that time.

For the time being, it looks like this hold rating was premature. Shares of the REIT have gone on to gain 21% as opposed to the 8% gains of the S&P 500 index (SP500) in that time.

When IRM released its financial results for the first quarter on May 2, the company comfortably posted a revenue beat. The growth outlook remains robust. Leverage is also holding steady and within the company’s targeted range. However, I still contend that shares are not an enticing enough of a value to warrant a buy rating right now. Thus, I’m maintaining my hold rating.

Iron Mountain Is Delivering Record Quarter After Record Quarter

IRM Q1 2024 Earnings Press Release

In my last couple of IRM articles, the REIT has shared record quarterly revenue. In that sense, this article will be the same as prior ones.

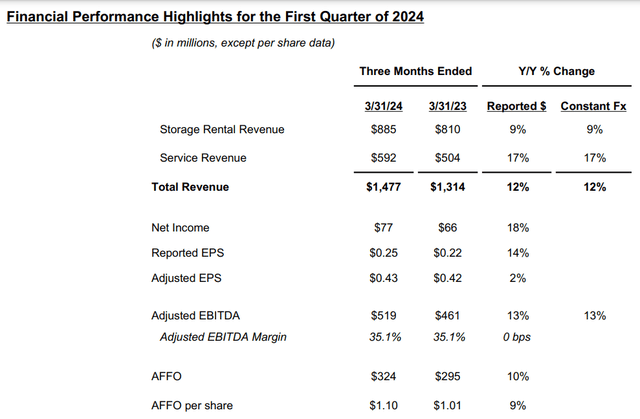

IRM recorded a new quarterly record of almost $1.5 billion in revenue during the first quarter, which was up 12.4% over the year-ago period. For more color, that was $30 million ahead of Seeking Alpha’s analyst revenue consensus. Given that both storage rental revenue and service revenue grew in the quarter, this topline growth was broad-based.

Storage rental revenue increased by 9.2% year-over-year to $884.8 million for the first quarter. According to IRM’s Q1 2024 10-Q Filing, higher storage rental revenue was due to increased volume in faster-growing markets and its Global Data Center Business segment.

IRM’s service revenue climbed by 17.4% over the year-ago period to $592 million in the first quarter. A combination of increased service activity levels in its Global RIM Business and higher volumes/pricing in its Asset Lifecycle Management business drove most of this growth.

The remainder of topline growth stemmed from $32.7 million linked to the recent acquisition of Regency Technologies. Even factoring out this acquisition, topline growth would have still come in firmly at a high-single-digit clip.

IRM’s AFFO per share rose by 8.9% year-over-year to $1.10 during the first quarter. Higher operating expenses and interest expenses led the company’s AFFO margin to contract by nearly 60 basis points to 22.5% for the quarter. That’s why AFFO per share growth lagged revenue growth in the quarter.

IRM Q1 2024 Earnings Presentation

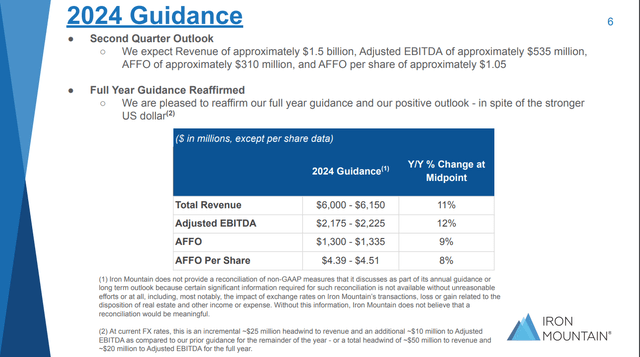

For this year, IRM reaffirmed guidance of between $4.39 and $4.51 in AFFO per share. At the midpoint, this would equate to an 8% growth rate over the 2023 AFFO per share base of $4.12. The $4.46 FAST Graphs analyst consensus for 2024 is also in line with company guidance.

Aside from bolt-on acquisitions that are moving the needle for IRM, the company is making progress in signing more data center leases with customers. During the first quarter, IRM signed 30 megawatts of data center leases with customers per CFO Barry Hytinen’s opening remarks during the Q1 2024 Earnings Call.

This will be an incremental catalyst in the quarters ahead. Not to mention that in Phoenix, construction on IRM’s third site has now commenced and there is a considerable pipeline of opportunities to fill it per Hytinen.

Per President and CEO William Meaney, the company’s approach to cross-selling to its 240,000-plus customers is also continuing to pay off. Mr. Meaney noted an oil and energy sector customer who initially selected IRM to manage its data containing geological information. Due to the company’s extensive range of products and understanding of customers’ needs, this customer added a secure IT asset disposition solution to its suite of services.

Another example of this in action was with a major bank in the United Arab Emirates. The customer relationship started with providing records management services for a growing volume of documents. Since this customer also needs to comply with regulations from the UAE’s Central Bank, it also added document capture and asset lifecycle management services into the mix.

This cross-selling is another reason why the forecast for beyond 2024 is also encouraging. For 2025, the FAST Graphs analyst consensus is that AFFO per share will rise by 7.5% to $4.80. In 2026, another 11.1% growth to $5.33 in AFFO per share is expected.

IRM Q1 2024 Earnings Presentation

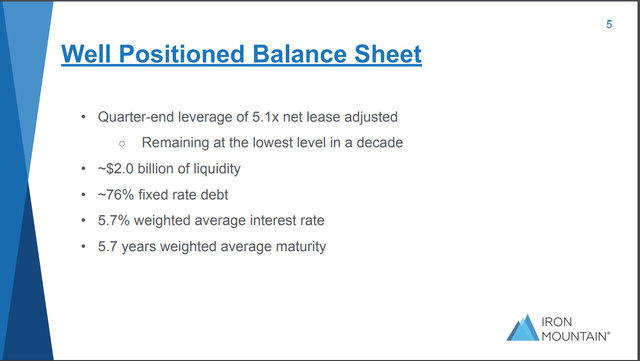

IRM’s balance sheet is also coming along. The company’s quarter-end net lease adjusted leverage ratio of 5.1 is in line sequentially with when I last covered it. This remains the lowest leverage IRM has had in a decade. It’s also within the targeted range of between 4.5x and 5.5x per Hytinen.

The company also had $2 billion in liquidity as of March 31, 2024. That leaves IRM with plenty of dry powder to opportunistically execute bolt-on acquisitions as it sees fit (unless otherwise sourced or hyperlinked, all details in this subhead were according to IRM’s Q1 2024 Earnings Press Release, IRM’s Q1 2024 10-Q Filing, and IRM’s Q1 2024 Earnings Presentation).

Fair Value Could Be Approaching $70 A Share

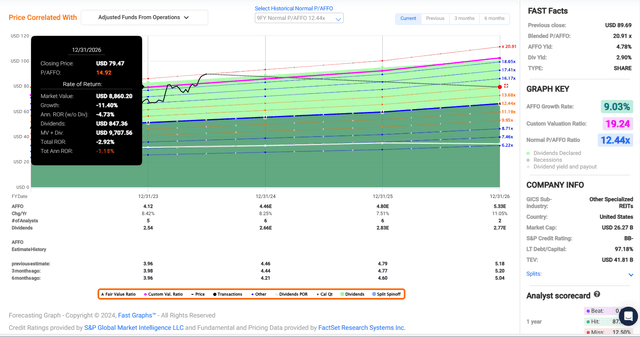

FAST Graphs, FactSet

Just as the fundamentals of IRM would have otherwise almost caught up with its fair value, I believe the rally since February leaves the valuation overextended.

The REIT’s current-year P/AFFO ratio of 20.4 is substantially above its nine-year normal P/AFFO ratio of 12.4 per FAST Graphs. On one hand, IRM’s annual AFFO per share growth prospects have improved from around 5% in that time to 9% now. In my view, this warrants a valuation multiple of three standard deviations above its normal P/AFFO ratio (excluding higher rates).

On the other hand, a higher interest rate environment moving forward will weigh on valuation to an extent. This is why I’m awarding a fair value multiple two standard deviations greater than the normal P/AFFO ratio, which would be 14.9. This is also right around the P/AFFO ratio of 15 that IRM has commanded for most of the past two years according to FAST Graphs.

The calendar year 2024 will be 51.9% complete in just a few more days. That means another 48.1% of the year remains and 51.9% of 2025 is still to come in the next 12 months. This is how I get a 12-month forward AFFO per share input of $4.64.

Plugging that into the aforementioned fair value multiple, I arrive at a fair value of $69 a share. From the current $91 share price (as of July 2, 2024), that would be a 31% premium to fair value. If IRM grows as anticipated and returns to my fair value multiple, cumulative total returns of -3% could be in store by the end of 2026. Put another way, the next couple of years of growth already seem to be baked into the share price.

Expecting Dividend Growth To Accelerate Further

The Dividend Kings’ Zen Research Terminal

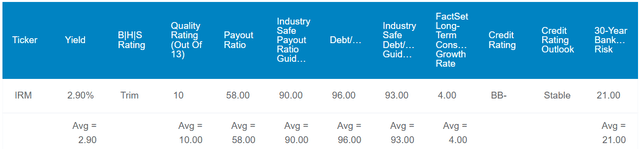

IRM’s 2.9% forward dividend yield is well below the real estate sector median of 4.7%. This explains the D- grade from Seeking Alpha’s Quant System for forward dividend yield.

Until recently, IRM’s dividend growth has been limited. The five-year compound annual growth rate of the dividend is 1.4%. That was because management’s goal was to get the payout ratio into the low-to-mid 60s percent range.

Now that this has been accomplished, the most recent raise was 5.1%. That’s more than double the sector median of 2.4%, which earns a B+ grade from the Quant System. Moving forward, I believe that annual dividend growth could even improve to 6%.

Assuming IRM raises its quarterly dividend per share by 6.1% to $0.69 in August, the REIT would pay $2.68 in dividends per share on dividends declared in 2024. Compared to the $4.45 midpoint AFFO per share guidance from management, this would be a 60.2% payout ratio. That’s well below the 90% payout ratio that rating agencies prefer from REITs and on the low end for IRM’s industry.

Risks To Consider

IRM’s fundamentals picture is quite robust right now, but there are always risks involved with investing in equities.

IRM’s customer base of 240,000 and counting is a great strength. However, it also comes with a meaningful risk. This large customer base makes the company’s IT networks an especially attractive target for hackers.

If a major cyber breach happened, this could lead to sizable lawsuits against IRM. Such an event could also undermine the trust of existing customers. This could cause customers to leave IRM and make it more difficult to attract new customers. That could be enough to hurt the company’s growth story.

IRM has been executing well for some time now. However, the somewhat lofty valuation opens the company up to the risk that a bad quarter or two could spark a major selloff in shares. This could potentially lead to a significant loss of capital for new money.

The company’s continued expansion into data centers is helping to drive its growth. If data center demand proves to eventually be overestimated, that could result in an oversupply of data centers. This could lead to increased competition with pricing to retain existing customers and attract new customers. That is another factor that could negatively impact IRM’s growth potential.

Summary: The Current Valuation Prices In Growth Through 2026

IRM is a business I’m happy to own in my portfolio. Relative to past years, growth is ramping up under the direction of Meaney. The balance sheet is also relatively strong for a junk credit rating of BB- from S&P. Unfortunately, I can’t get behind IRM at the current share price.

Is it possible that IRM continues to outperform the S&P? Sure.

But at this valuation, such an outperformance wouldn’t be justified even by the currently healthy fundamentals. This is why I’m not interested in adding new money to IRM until either the share price retreats into the low-$70s (or fair value catches up with the share price as time goes on).

Read the full article here

")

")

")

")

")