")

Introduction

Fixed income securities became big losers twice since 2020. The first time was when COVID terrorized the market, with several issues postponed payments on their preferred stocks. The second time was when the FOMC decided to fight inflation, mostly caused by excessive spending fighting the economic effects of COVID, by rising the FFR at the fastest pace ever. As the rate rose, existing issues saw their prices drop to realign their yields with what newer issuers were forced to pay.

With inflation down and some economic signs pointing to a slowdown in the US economy, hope has again risen that maybe the FOMC will do a rate cut before the end of the year. If indeed we are near a peak in interest rates, one potential strategy is owning fixed income assets without a maturity date, like most preferred stocks, or bonds or notes with extended maturity dates and decent Call protection.

This year, the AG Mortgage Investment Trust (NYSE:MITT) issued a pair of Notes that mature in 2029, with Call protection into 2026 which is the focus of this article.

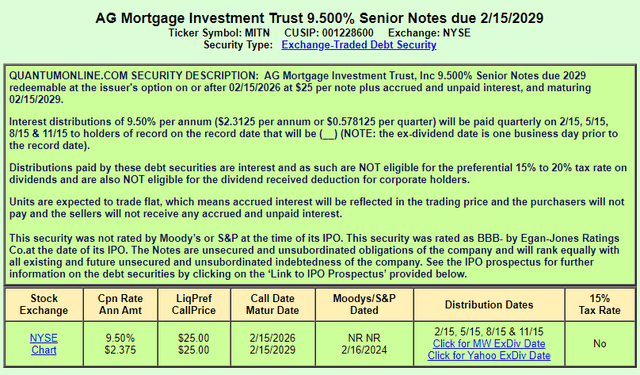

- AG Mortgage Investment Trust 9.500% Senior Notes due 2/15/2029 (NYSE:MITN)

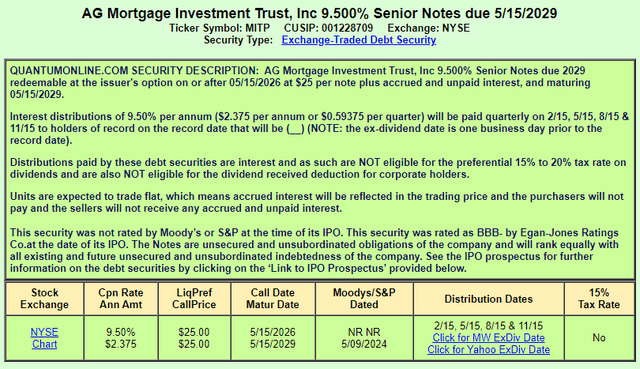

- AG Mortgage Investment Trust, Inc 9.500% Senior Notes due 5/15/2029 (NYSE:MITP)

With both trading near Par, I gave both a Hold rating as the yield did appear to compensate for the default risk, though possibly small, considering the low coverage ratio MITT provides.

AG Mortgage Investment Trust review

Understanding the issuer of these Notes is an important part of the due diligence in determining if their high yields justify the risk of owning Notes not maturing until 2029.

Seeking Alpha describes MITT as:

AG Mortgage Investment Trust, Inc. operates as a residential mortgage real estate investment trust in the United States. Its investment portfolio includes residential investments, including non-agency loans, agency-eligible loans, re-and non-performing loans, and non-agency residential mortgage-backed securities, as well as commercial loans and commercial mortgage-backed securities. The company qualifies as a real estate investment trust for federal income tax purposes. It generally would not be subject to federal corporate income taxes if it distributes at least 90% of its taxable income to its stockholders. AG Mortgage Investment Trust, Inc. was incorporated in 2011 and is based in New York, New York.

Source: seekingalpha.com MITT

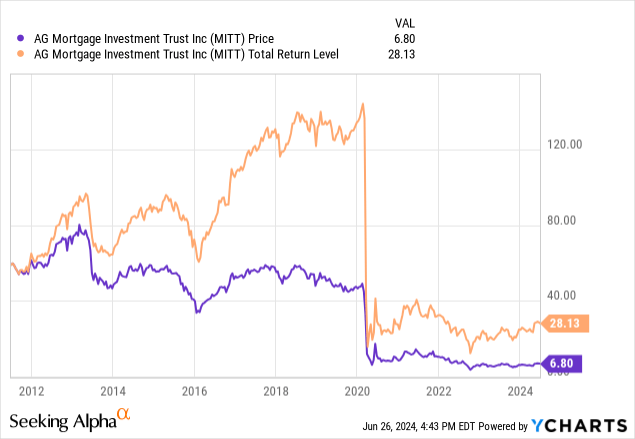

Not mentioned in that description is poor financial performance caused MITT to execute a 1-for-3 reverse split in July 2021, just ten years since its IPO! Also, as COVID hit, payments on its three preferred stocks were suspended twice; finally paid in full in the fall. Both illustrate how sensitive mortgage REITs are to the movement in interest rates.

MITT describes itself as:

AG Mortgage Investment Trust, Inc. is a residential mortgage REIT with a focus on investing in a diversified risk-adjusted portfolio of residential mortgage-related assets in the U.S. mortgage market. We are externally managed and advised by AG REIT Management, LLC, a subsidiary of Angelo, Gordon & Co., L.P., a leading privately-held alternative investment firm focusing on credit and real estate strategies.

Source: agmortgageinvestmenttrust.com/corporate-profile

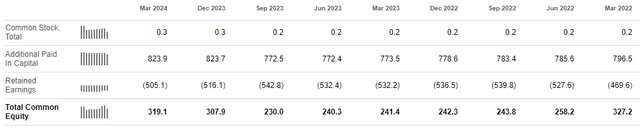

As a sign of confidence, the Directors and Executive Officers own almost 4% of the stock. That said, the financials are not the best, with MITT’s ability to generate a profit continuing to be mixed but improving.

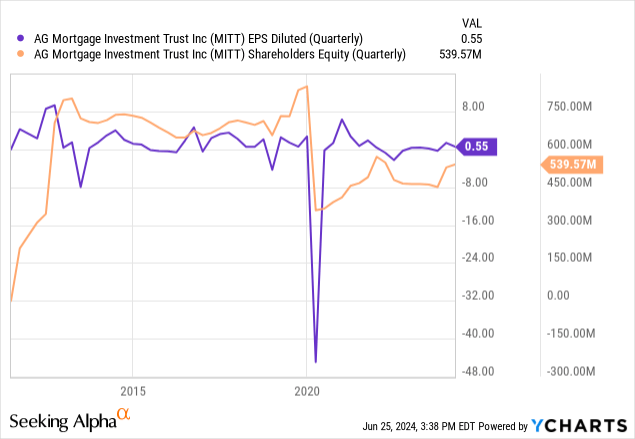

The next chart shows quarterly data back to March 2022.

seekingalpha.com/symbol/MITT/income-statement

Things have improved as MITT has reported positive Normalized EPS for six straight quarters after several that were in the red. Common dividends have held at $.18/quarter over that same period. After dropping since 2022, MITT has been able to issue over 9m new common shares since late 2023, which lowers the risk level, for now, that the $95m in Notes discussed will default. That said, the amount of Common Equity available to repay the Notes is just over 3X, A level that does not give me great warmth.

seekingalpha.com/symbol/MITT/balance-sheet

Notes reviewed

quantumonline.com MITN quantumonline.com MITP

| Factor | MITN | MITP |

| Issue date | 1/23/24 | 5/8/24 |

| Issue Size | $30m | $65m |

| Coupon | 9.5% | 9.5% |

| Call date | 2/15/26 | 5/15/26 |

| Maturity date | 2/15/29 | 5/15/29 |

| Price | $25.12 | $25.05 |

| Yield | 9.45% | 9.48% |

| YTC | 9.18% | 9.38% |

| YTM | 9.37% | 9.45% |

The major rating agencies provided no rating, but the smaller Egan-Jones Ratings Company gave them a BBB-, the lowest possible investment-grade rating. Others on Seeking Alpha have expressed doubts about ratings by EJ. Being Notes, the interest payments do not qualify for the lower tax rates dividends get.

Analysis

Both Notes offer the same coupon and can be called and then mature within three months of each other. The MITP Note is the better buy on all fronts. Along with the better Call protection, it offers investors a higher Yield, YTC, and YTM, though the differences are small. Mitt’s shaky past and current low coverage ratio (TCE/Notes MV near 3) has me giving both a Hold rating, except for risk seekers with a well-diversified fixed income ladder. Despite the volatile nature of mREITs, few have ever defaulted, but that is a concern here, in my opinion. Lower overall rates and a normal yield curve would help the issuer.

I do prefer these over the common, as the yield disadvantage is under 100bps: take the assets higher in the food chain for that little bit of extra yield the common provides. The MITN’s big advantages are it matures first and takes less cash to redeem as it has less outstanding versus MITP.

For investors okay with owning MITT securities, they have three preferred stocks (article link), two of which are yielding over 10%. That said, there are several reasons I own the Noted over the preferred stocks:

- Notes ranked higher if bankruptcy becomes necessary

- It is legally easier to skip preferred stock dividends than interest payments on the Notes.

- The Notes still have Call protection and have maturity dates for investors liking that factor.

- The yield advantage of the preferred stocks, to me, doesn’t compensate for the added risk.

Final thoughts

Are interest rates near a peak? My recent purchase of single-year HY bond ETFs maturing after 2027 has me firmly in that camp. An example of what they provide was covered in this article. While the estimated YTM is below 8%, the bonds held are rates around where EJ rated these Notes but come with the comfort the ETF owns a wide basket, so default damage would be less versus MITT going under.

Read the full article here

")

")

")

")

")