")

")

New Mountain Finance (NASDAQ:NMFC) is a BDC that has a relatively decent NAV base of ~ $1.4 billion, ranking it well above the sector median of $839 million. NMFC is also one of the few BDCs with a conservative business strategy that I have not covered so far.

Just as most conventional BDCs, NMFC focuses on providing direct lending products (from primarily senior to junior loans) to U.S. upper middle market companies, which are backed by private equity sponsors. Here it is important to underscore that NMFC does not invest in CLO structures or VC type businesses, which introduces a completely new layer of risk (volatility).

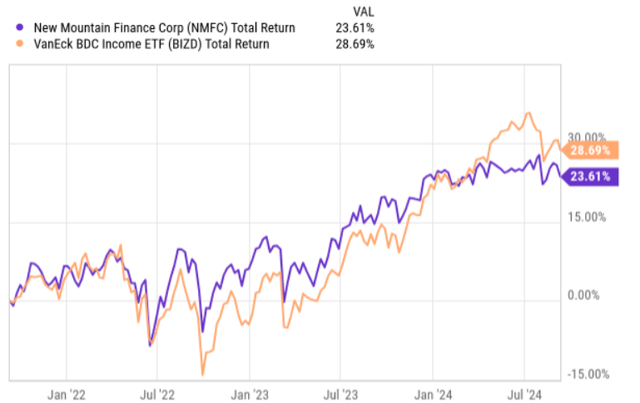

If we look at the chart below, we will notice a quite correlated trend with the overall BDC market, where over the past 3 years NMFC has delivered circa 23% in total returns, which is ~ 5% below the benchmark result.

YCharts

On a Price to NAV basis, NMFC trades almost exactly at par, which gives no direct advantage or disadvantage in the process of deciding whether to invest or not.

With this in mind, let’s take a look at the underlying core fundamentals to understand whether NMFC embodies some specific advantage as to why it should be included in the portfolio and that would substantiate a higher valuation (i.e., effectively a premium to NAV) than what is currently priced in.

Thesis

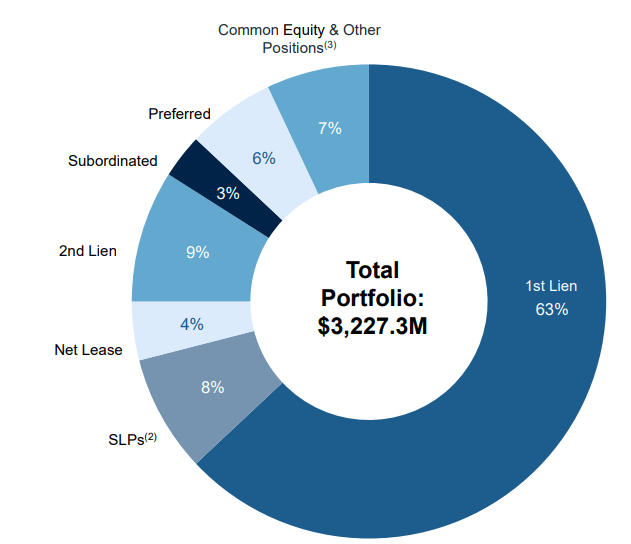

While as I described above, NMFC indeed puts a focus on first lien structures, the total exposure towards this specific asset segment is actually not that large relative to what other defensive BDCs have in place. The pie chart below depicts the situation nicely, where we can see that only 63% of the AuM is explained by first lien with the remaining chunk being spread across more risky asset classes such as subordinated debt, second lien, and equity investments.

New Mountain Finance

Already from this fact alone, I would expect some discount to NAV just to account for the above-average risk profile that is embedded in NMFC (i.e., way lower concentration in first lien investments than for other sector peers).

The second nuance, which, in my opinion, could be considered a notable disadvantage, is the concentration risk that lies in NMFC’s Top 15 investments. These specific investments (or portfolio companies) account for more than 40% of the total portfolio asset base, which is again significantly above the sector average negatively.

Furthermore, speaking of the risk profile, the underlying credit statistics do not look good either. For example, as of Q2, 2024 the weighted average net debt to EBITDA and weighted average interest coverage for portfolio companies stood at 6.3x and 1.7x, respectively. This is once again an indicative of a more elevated risk than what we can observe by contrasting NMFC with other sector peers such as Main Street Capital (MAIN), Crescent Capital (CCAP), and Blackstone Secured Lending Fund (BXSL).

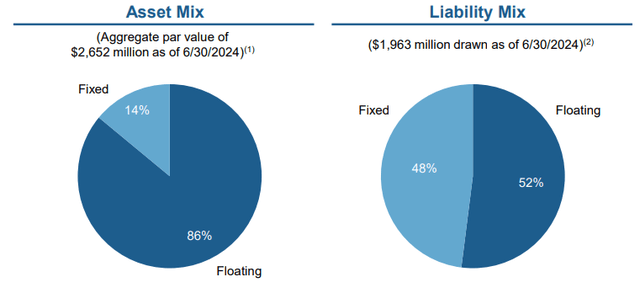

Apart from the quality, it is critical to factor in a quite specific nuance, which is not that common in the BDC space – i.e., NMFC’s mismatch on the asset and liability side.

New Mountain Finance

In this chart, we can see that 86% of the BDC’s assets are based on a floating rate component, while the debt side has only 52% of the assumed leverage linked to SOFR. Theoretically, this could be an advantage if the fixed-rate borrowings were subject to higher financing costs than what could be currently sourced from the market. Yet, if we peel back the onion a bit here, we will notice that most of the fixed-rate borrowings have been assumed at below current market-level financing levels. For instance, the largest fixed rate borrowing piece is based on 3.875%, which is clearly not possible to obtain in the prevailing interest rate environment. Even if the interest rates drop by 50 or 100 basis points, the new financing after this particular debt rollover will be much higher.

Finally, by assessing the recent dynamics of one of the most important core performance metrics – adjusted NII generation per share – the overall picture does not look that promising either.

In Q2, 2024 NMFC generated adjusted NII per share of $0.36, which just barely covers the current dividend of $0.34 per share, resulting in dividend coverage of 105%. Given the aforementioned dynamics, I would definitely expect a higher margin of safety on the dividend – just to account for the potential risk that could stem from increased non-accruals and further headwinds from higher financing costs.

In fact, the situation gets worse if we consider the backdrop of declining adjusted NII generation levels, which starting from Q4, 2023 have been subject to elevated pressures from primarily the spread compression angle. This is not an NMFC-specific element, but rather a general trend in the BDC space, especially when it comes to the U.S. upper middle market segment in which NMFC operates.

The Bottom Line

As the analysis above shows, New Mountain Finance clearly carries several fundamental risks that, in my humble opinion, should lead to a material discount to NAV, which has currently not been priced in by the market.

It is mostly the combination of subpar portfolio quality (security and structure wise), unfavorable asset and liability mismatch, and thin dividend coverage that renders the overall investment case just too risky for my taste.

At the same time, given that NMFC has a decent portion of its portfolio allocated towards equity instruments, there could be an additional return component that could be realized once the M&A markets open (which are set to do so as the interest rates go down). Plus, the BDC has a slightly lower leverage profile than the other peers have, which, in turn, would enable NMFC to grow the asset base from here, thereby boosting the adjusted NII result. Hence, I would not recommend shorting NMFC.

Read the full article here

")

")

")

")