")

")

One company that has been on a pretty wild ride over the past several months has been Newpark Resources (NYSE:NR). Year to date, shares of the company are up 16.9%. And over the past year, they have soared by 84.8%, handily outperforming the broader market. Even so, the firm has seen some volatility on the downside. On June 14th, for instance, shares dropped 7.2%. Lately, the firm has exhibited some weakness on both its top and bottom lines. This follows a few years of generally better growth on a year-over-year basis. From an absolute perspective, I would argue that shares look somewhere between undervalued and fairly valued, but compared to similar enterprises, the stock does look a bit pricey. Given this and after factoring in the aforementioned volatility, I would argue that the firm makes for a solid ‘hold’ candidate. But if we can start to see some improvements with one core part of the firm, it wouldn’t take much to justify an upgrade to a soft ‘buy.’

An interesting prospect

At a high level, the management team at Newpark Resources describes the company as a diversified supplier that provides its customers with environmentally sensitive products, as well as rentals and services to customers across a wide array of industries. This is rather vague in my opinion. A better way to come to understand the business would be to look at each of its two operating segments individually. The first of these is the Industrial Solutions segment. Through this unit, the company provides customers with work site access solutions. Examples here include the rental of recyclable composite matting systems, as well as similar solutions, to customers in the oil and gas space, the pipeline space, the renewable energy market, construction, and more.

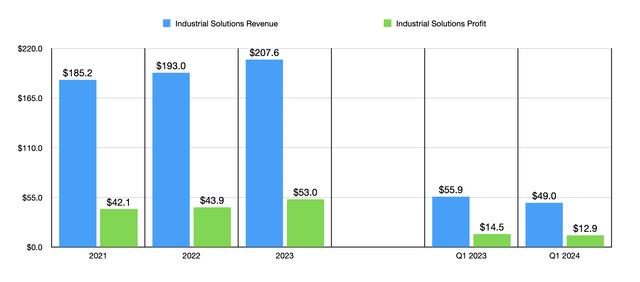

The primary product in this segment is called DURA-BASE, and it essentially operates as a protective mat that can be interlocking and that is often used as a temporary road In harsh environments where traditional roads would be too expensive, time-consuming, and illogical to utilize. In the past, mats composed of timber were used. But because of environmental purposes and long-term costs, DURA-BASE is considered is superior option. Last year, this part of the company was responsible for $207.6 million, or about 27.7%, of the company’s overall sales. Management claims that the vast majority of the revenue associated with this segment comes from the power transmission sector.

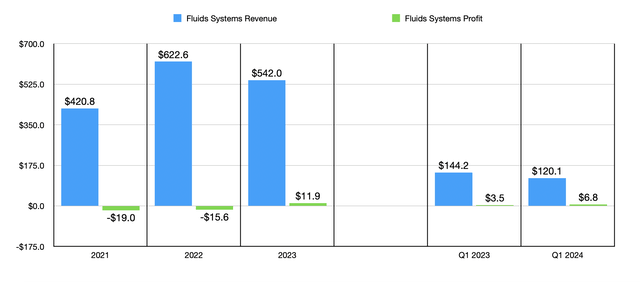

A more significant part of the company, from a revenue perspective, is the Fluids Systems segment. Through this unit, the company provides drilling and completion fluids products and related services to customers in industries such as oil and gas exploration and production, geothermal energy, and more. The Industrial Solutions segment of the company gets most of its revenue from the US and the UK. By comparison, the Fluids Systems segment is far more global. 44% of its revenue comes from a combination of countries spread throughout the EMEA (Europe, Middle East, and Africa regions, while another 4% comes from the Asia Pacific region. The remaining 52% is attributable to customers in North America. This is a much larger portion of the company, accounting for $542 million, or 72.3%, of overall sales last year. The firm used to have another segment called Industrial Blending. But management ended up winding this down in the first quarter of 2022.

Author – SEC EDGAR Data

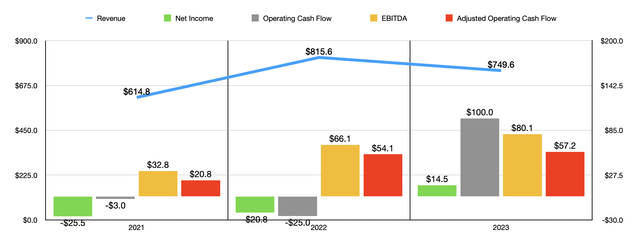

Over the past few years, Newpark Resources has seen a good deal of volatility on both its top and bottom lines. From 2021 to 2022, for instance, sales for the business jumped from $614.8 million to $815.6 million. Then, in 2023, sales fell to $749.6 million. This is not to say that all parts of the company have seen this kind of volatility. In fact, the Industrial Solutions segment has actually seen pretty consistent growth, with sales growing from $185.2 million to $207.6 million over this window of time. It has been the Fluids Systems segment that has seen downward pressure. After reporting revenue growth from $420.8 million in 2021 to $622.6 million in 2022, sales then plummeted to $542 million last year. Some of this is because of lower demand for its services in the US, as well as a loss of market share. However, the company did suffer to the tune of $82.7 million from certain business units that the company had divested itself of over this window of time.

Author – SEC EDGAR Data

One good thing about management is that they have been very transparent about recent operations. In 2023, for instance, the company conducted a review regarding strategic alternatives for the Fluids Systems segment. This would likely take the form of a sale of that business in its entirety, though we have no idea what kind of terms to expect. The company has also exited a variety of lines of business, including its chemicals product line, its offshore Australia operations, its operations in Chile, and more.

Author – SEC EDGAR Data

One thing that I would like to point out is that while the Fluids Systems segment of the company is responsible for the bulk of revenue, it’s actually responsible for only a small portion of overall profits. From 2021 to 2023, segment profits went from negative $19 million to positive $11.9 million. By comparison, the Industrial Solutions the segment reported growth in profits from $42.1 million to $53 million. This is why, if a sale does occur regarding the Fluids Systems part of the company, investors should not expect a significant amount of cash in return.

Over this three-year window, profits and cash flows through the company generally improved even in spite of the top line volatility the company exhibited. The firm’s net loss went from $25.5 million in 2021 to a gain of $14.5 million last year. Operating cash flow went from negative $3 million to positive $100 million. Other profitability metrics followed this movement higher. Adjusted operating cash flow, which ignores changes in working capital, went from $20.8 million to $57.2 million. Meanwhile, EBITDA for the company expanded from $32.8 million to $80.1 million.

Author – SEC EDGAR Data

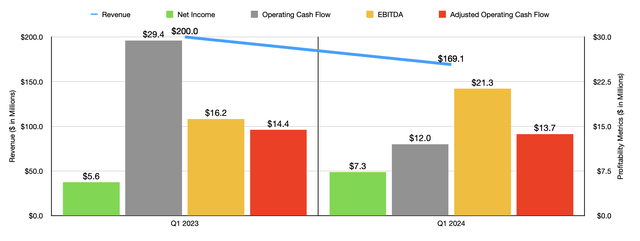

When it comes to the current fiscal year, the picture has not been as pleasant. Revenue for the first quarter continued falling, dropping from $200 million last year to $169.1 million this year. Driven by a decline in rig count throughout North America from 981 units in 2023 to 831 units today, the revenue that the company generated from its Fluids Systems segment fell from $144.2 million to $120.1 million. Even the Industrial Solutions segment of the company took a hit, dropping from $55.9 million to $49 million. Management did say, however, that this decline was largely the result of a drop in product sales associated with this segment as opposed to a reduction in rental revenue. You see, while the company does prioritize renting out these products, it does also sell them to customers across the globe. Management attributed this reduction in product sales to the timing of customer products and orders.

Despite these pains on the top line, there was a bright spot for investors to enjoy. And this was an increase in net income from $5.6 million to $7.3 million. Some of this was because of a reduction in interest expense from $2.1 million to just under $1.8 million. However, the company also benefited from a decline in other costs, such as a $1.1 million reduction in selling, general, and administrative costs, and a $1.4 million rise in income from other operating activities. The latter of these was largely the result of a gain regarding a final insurance settlement stemming from damage done during Hurricane Ida back in 2021, as well as a gain from a legal settlement that management decided not to provide additional details of. Other profitability metrics were mixed. Operating cash flow, as an example, was cut significantly from $29.4 million to $12 million. If we adjust for changes in working capital, we would get a more modest reduction from $14.4 million to $13.7 million. Meanwhile, EBITDA for the company expanded from $16.2 million to $21.3 million.

One thing I would like to point out here is that management seems optimistic when it comes to profitability for the Industrial Solutions segment. Even though segment profits dropped from $14.5 million to $12.9 million, management expects its EBITDA to come in at between $80 million and $85 million this year. This should be based on revenue of between $230 million and $240 million. At the midpoint, this translates to a year-over-year increase in sales of 13.2% and a year-over-year increase in EBITDA of 10.9%. This is interesting considering the weakness seen in the first quarter of this year relative to the same time last year.

Author – SEC EDGAR Data

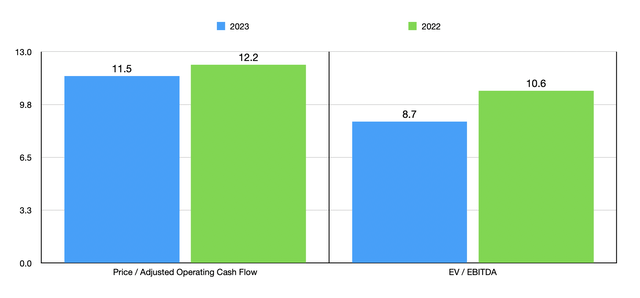

Because of a lack of other estimates for 2024, I think it would be premature to estimate what the rest of the year will look like and to value the company according to that. Instead, in the chart above, I decided to value the firm using historical results for 2022 and 2023. As you can see, the stock is definitely not expensive. On the other hand, I wouldn’t call it cheap either. It seems to be sitting somewhere in between, depending on which valuation metric you prefer. Relative to similar firms, however, shares are quite expensive. On a price to operating cash flow basis, four of the five companies I compared the firm to in the table below are cheaper than it. This drops to three of the five when using the EV to EBITDA approach.

| Company | Price / Operating Cash Flow | EV / EBITDA |

| Newpark Resources | 11.5 | 8.7 |

| Dril-Quip (DRQ) | 10.8 | 10.8 |

| Enerflex (EFXT) | 2.0 | 5.8 |

| Core Laboratories (CLB) | 51.9 | 15.7 |

| North American Construction Group (NOA) | 3.6 | 5.5 |

| ProPetro Holding Corp. (PUMP) | 2.4 | 2.9 |

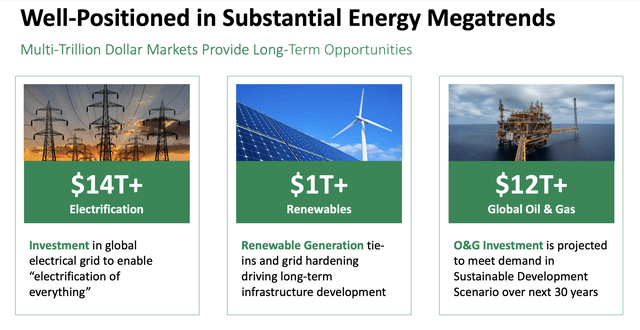

Even though I am moving forward with a ‘hold’ rating for the stock, this does not mean that I don’t believe in the company’s potential in the long run. The fact of the matter is that the company operates in industries that have tremendous dollar amounts behind them. The global electrification market, for instance, is expected to see over $14 trillion worth of investments over the next several years. The renewable generation market should add another $1 trillion, if not more, in infrastructure development. And the global oil and gas space is expected to see over $12 trillion of investments over the next 30 years. Clearly, this invites opportunity for the business, particularly if it does proceed with a sale of the Fluids Systems business and uses the proceeds from that sale to make further investments in growth for what will be its only remaining operations on its books.

Newpark Resources

Takeaway

Based on the data provided, Newpark Resources is most certainly an interesting company. In the long run, management will probably create some value for investors. I especially like the company’s strategy of becoming simpler and focusing on one core area. On the other hand, shares of the business do look pricey relative to similar firms, and historical volatility is disappointing to see. You also have the fact that there is a great deal of uncertainty when it comes to what will ultimately occur regarding the Fluids Systems business. Even though it has net assets of $205 million, the earnings associated with it are small. It wouldn’t be surprising to see it sell off at a rather low price. Until some of this uncertainty clears up, and perhaps until we have a better idea of whether or not guidance will hold for this year involving the Industrial Solutions business, I think that rating the company a ‘hold’ makes the most sense.

Read the full article here

")

Married With Children’s Ed O’Neill tells the story of how he was cut from the Pittsburgh Steelers")