")

The global derivatives market is growing rapidly, with new products launched at a steady cadence. According to the Bank for International Settlements, the notional value of all OTC derivatives in 2023 stood at $667 trillion, growing 8% over the prior year. Why is this relevant to the average retail investor in the U.S.? The main reason, I believe, is that it provides much broader investment opportunities that were heretofore only available to institutional investors with hundreds of millions in managed funds.

Today, that picture is very different, and this reality is marked by the rise of increasingly new ways in which an investor can deploy their funds. One such interesting study is the Return Stacked® U.S. Stocks & Futures Yield ETF (BATS:RSSY), which is the subject of our discussion today. The fund has an expense ratio of 1.04%, which is quite reasonable, in my opinion, and the AUM is a little shy of $130 million as I write this.

How Does the ETF Make Money?

The fund essentially follows two key strategies. The first is the simple act of investing in U.S. large-cap stocks, and the second is a more complex approach that takes advantage of futures yields across multiple segments, including currencies, commodities, bonds, and equities. According to the fund’s website, the ETF:

Aims to provide simultaneous exposure to U.S. stocks and a futures yield strategy. For every $1 invested, RSSY aims to provide $1 of exposure to large-cap U.S. equities and $1 of exposure to a futures yield strategy.

This futures yield component of the strategy is interesting, because the fund rebalances daily, and the futures contracts can be any mix of the above underlying assets, but it also involves both long and short positions. The end result is the fund’s ability to “harvest” the roll yield or roll return, which is calculated as follows:

Roll yield = (total change in futures prices) – (total change in spot price)

Now, this is different from a dividend yield or a fixed income yield (such as a bond’s YTM or yield to maturity), but it essentially has the same effect of complementing the core return from the changing price of the underlying asset – whether that’s a bond, a commodity, an equity, or a currency pair.

RSSY, therefore, can be said to use a strategy that not only directly benefits from an equity’s price gain or loss, but adds a couple of layers on top of that – the price change in the underlying assets and the roll yield.

The mechanics are more complex than that, of course, but the essence of it is that when long-dated contracts are priced higher than short-dated contracts (contango), the roll return is negative, while the inverse is true when the futures curve is in backwardation, which is the exact opposite and longer-dated contracts are priced lower than short-dated contracts. This second situation can happen when the commodity, such as soy, sugar, gold, corn, etc., faces short-term shortages that aren’t expected to be repeated the following year. Therefore, the total return for the fund comprises the price appreciation/depreciation component of the equities and futures contracts and the yield or roll return component of the contracts.

The best part about this is that you don’t need to understand any of this if you’re investing in an ETF that does the job for you. So, that now begs the question: how has this fund performed so far?

Is it worth considering RSSY for your portfolio?

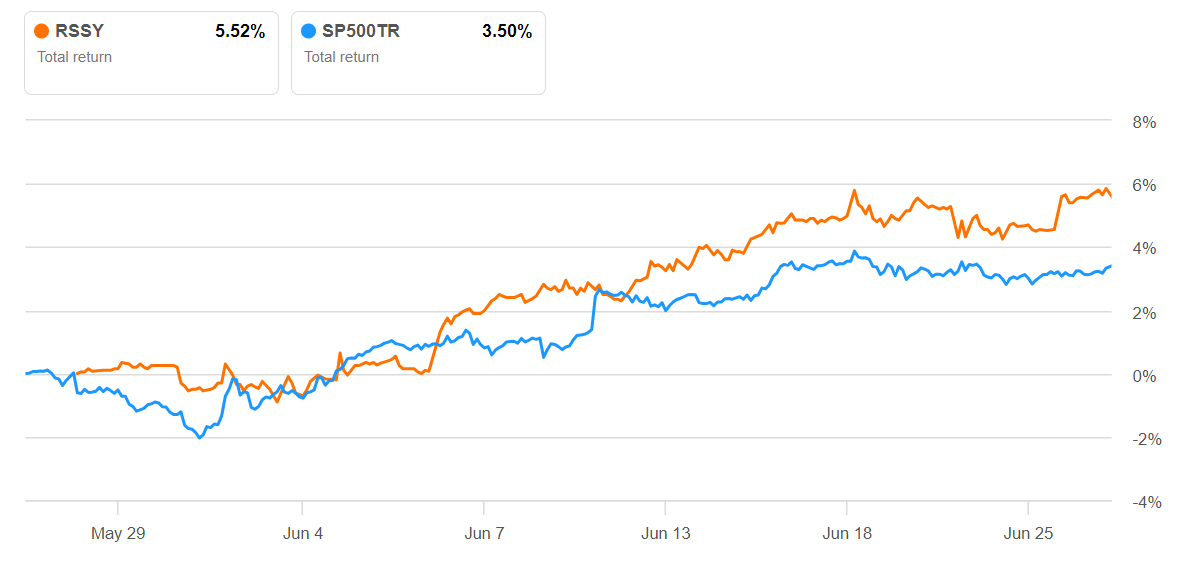

Unfortunately, since the fund is only a little over a month old, we don’t have robust historicals. However, looking at the past month’s total return of 5.52% against (SP500)’s 3.5%, I’d say it’s off to a great start.

SA

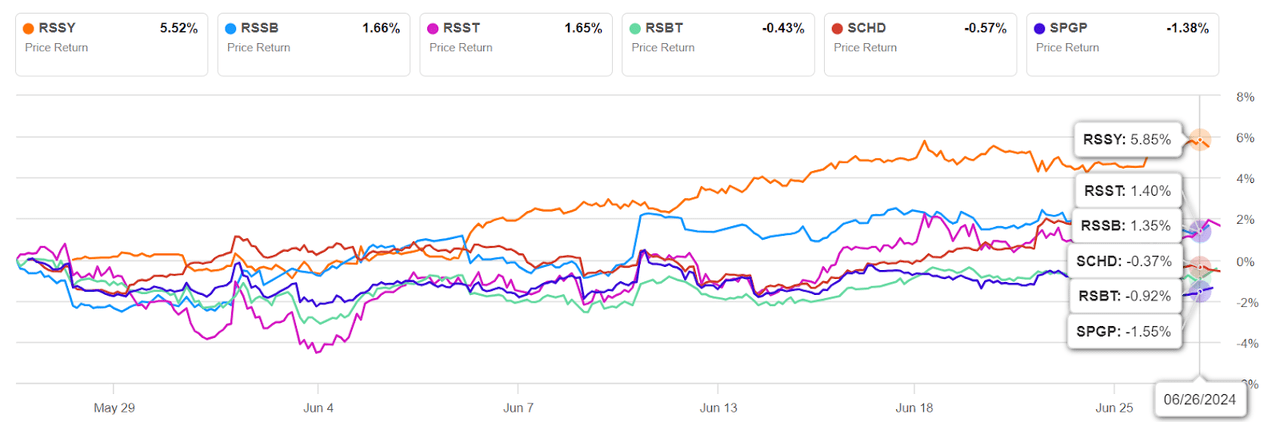

While the time frame is quite limited, we can already see RSSY outperforming not only its peers, but also broader dividend equity ETFs like SCHD and value plays like SPGP.

SA

The new fund seems to be racing past its peer group, and I’m assuming that’s because the fund managers have refined their strategy based on learnings from the sponsor’s older products, like RSST, which uses a similar U.S. stocks and futures approach but with some significant differences. My best guess is that yield-harvesting on futures contract rolls is more lucrative than the trend-following strategy employed for RSST.

One important consideration here is that the fund is flexible in terms of direction. It uses both long and short trades to maximize its yield, and that dynamic approach gives the fund managers a lot of freedom when compared to funds with more restrictive strategies, such as the leveraged and inverse ETFs that I’ve written quite a bit about in the past several months. I invite you to check those out if you’re interested in how these various ETF strategies differ from each other.

As a knock-on effect, the daily rebalancing in the case of ETFs like RSSY is very different from that of leveraged and inverse ETFs that seek to achieve a gain equal to a multiple of the underlying assets. The difference is that the impact of volatility decay is a little muted in this scenario. That doesn’t mean the risks are fewer or, well, less risky; all it means is that you won’t see the kind of volatility drag on your investment that you see with leveraged and inverse leveraged ETFs, especially the 2x, -2x, 3x, and -3x funds.

That’s a big consideration depending on how long you plan to hold the fund in question, but that’s not a risk you need to be overly worried about with RSSY, in my opinion. However, please don’t be under the impression that there’s no leverage risk here, because futures contracts are, by definition, giving you added investment exposure. Leverage, in other words. The only reason I say that this particular risk is a little muted or less pronounced is that RSSY also invests directly in equities, while most leveraged ETFs don’t. Direct equity ownership doesn’t come with leverage risk because you’re not getting any additional exposure for greater gains (or greater losses).

That said, there are certainly other risks you need to be aware of as an investor, including derivatives risk, VIE structure risk or Cayman subsidiary risk, commodity risk, bond risk, currency risk, leverage risk (as mentioned above), non-diversification risk, and the all-important new fund risk because this was recently launched.

All things considered, and with the limited historical data we have, I would definitely recommend this fund as a way to hedge your portfolio against – at the very least – the uncertain economic climate in the United States. Remember that this fund also gives you exposure to currencies as well as interest rates, and the long-short strategy used by the fund should, if they work as planned, help you offset at least some unrealized losses in your core portfolio of U.S. stocks. There’s also the emerging market risk with RSSY, but the current situation with the strong dollar and higher-for-longer Fed fund rates transforms that risk into an opportunity if you’re willing to hold RSSY for the long run.

The last thing I’d like to say before I recommend a Buy for RSSY is that you need to carefully weave this into your portfolio and size it based on your expectations for the overall market. While we don’t yet know how this fund will perform in the event of a market downturn, it’s structured in such a way that it should theoretically benefit from strong momentum regardless of the direction of that momentum. The 50% U.S. large-cap and 50% futures yield mix looks like it’s structured to withstand a downturn, but it’s not been tested in the real world yet. That, to me, is the biggest risk to be aware of.

Regardless, from what I’ve seen of RSSY, it looks like a good way to hedge your other bets – the quantum of which you’ll need to decide based on where you think the market will be headed in the next three, six, and twelve months. That’s the real bottom-line consideration here, and I hope this analysis has been helpful. Please feel free to leave your thoughts in the comments section. Thank you for reading.

Read the full article here

")

")

")

")