")

Have you ever ordered Tostilocos? It seems to have been a thing for over 8 years, why are you missing out")

")

Shares of Sanofi (NASDAQ:SNY) have yet to fully recover from the business strategy change the company dropped on investors in October 2023. At the time, Sanofi announced plans to increase R&D investments to “drive long-term growth and enhance shareholder value” and to separate its consumer healthcare business to enable greater focus and resources to the biopharma business. This was a shocking turn of events for a slow-growing, dividend-paying company, and I understand the reluctance of the shareholder base, which likely experienced increased turnover since the announcement.

As hard as the decision may have been for the company to make, as a growth investor, I genuinely liked it and felt it was one of the best decisions the company made in years, and I believe increased pipeline investments will lead to higher long-term shareholder returns and that the short-term pain is worth it.

The immunology business is in great shape, by far, and is doing a lot of the heavy lifting to get the company to a higher growth mode, and I expect that to remain the case in the second half of the decade and in the 2030s, led by Dupixent and by the emerging pipeline candidates such as amlitelimab and frexalimab, and we should see further complementary business development transactions going forward.

Commercial business is performing well

Dupixent generated nearly $12 billion in net sales last year, and at its R&D day presentation in December 2023, Sanofi guided for a low double-digit CAGR in the 2023-2030 period which suggests annual sales will reach at least $22-23 billion by 2030. We will see increased competition in many of the indications Dupixent is approved for or being developed for in the following years, but I believe this goal will be either met or exceeded, as penetration rates of biologics and of Dupixent are still relatively low in many of the large indications.

Looking across the rest of the commercial biopharma portfolio, there are not many other standout performers and I will highlight four, although the fourth one has a big asterisk:

- Sarclisa in multiple myeloma. This is Sanofi’s attempt at capturing significant market share with a product that shares the mechanism of action but is significantly behind the market leader – Johnson & Johnson’s (JNJ) Darzalex. Sarclisa still has a narrower label compared to Darzalex, but it grew 29% Y/Y in the first quarter to EUR106 million (approximately $115 million) and it had a recent clinical trial win in first-line multiple myeloma which should lead to label expansion and a new growth phase. Regulatory submissions are under review, and if approved, Sarclisa will be the first anti-CD38 therapy approved in combination with standard of care VRd regimen (bortezomib, lenalidomide and dexamethasone) for the treatment of newly diagnosed multiple myeloma patients not eligible for transplant.

- Beyfortus was approved in July 2023 for the prevention of RSV lower respiratory tract disease in infants, and it had a strong launch with EUR547 million (approximately $600 million) in net sales in 2023, and it is Sanofi’s intention for this product to become a blockbuster in 2024 with the majority of sales coming in the second half of the year.

- Altuviiio, the once weekly factor VIII replacement therapy for hemophilia A, was also approved in 2023, and is off to a decent start with EUR159 million ($175 million) in net sales in 2023 and EUR122 million ($130 million) in the first quarter of 2024.

- Nexviazyme for the treatment of Pompe disease. Q1 net sales grew 96% Y/Y to EUR150 million ($165 million), but the big asterisk I mentioned is that it is the next-generation enzyme replacement therapy which is growing primarily by taking share from Sanofi’s first-generation product Myozyme/Lumizyme. Adjusted for the cannibalization, net sales of the Pompe disease franchise are growing only in the high single digits.

The growth of Dupixent and the relatively recent launches of Beyfortus and Altuviiio were enough to offset the currency headwinds and the poor performance of other products, including the generic erosion of the multiple sclerosis product Aubagio. Net product sales grew 5.3% in 2023 and 6.7% in the first quarter of 2024.

On the earnings side, given the October 2023 announcement of 2024 being an investment year, management expects a low single-digit EPS decline for the full-year at constant exchange rate and stable if the impact of the higher tax rate is excluded. A strong EPS rebound should follow in 2025.

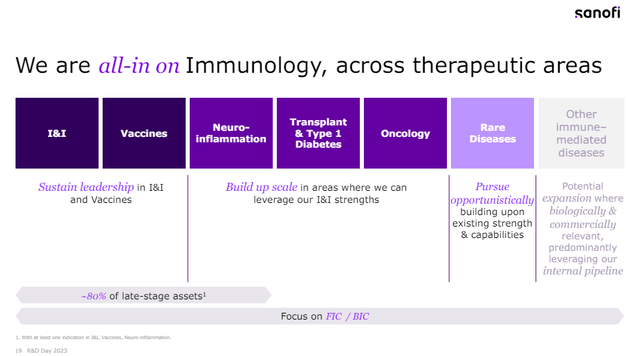

All-in on immunology – and the pipeline reflects it

“We are all-in on immunology, across therapeutic areas.”

This was the title in one of the presentation slides at the December 2023 R&D day and reflects Sanofi’s commitment to this segment that spans across several areas.

Sanofi December 2023 R&D day presentation

The obvious leader here is Dupixent, which is already approved for a double-digit number of indications and with more on the way, including important opportunities such as chronic obstructive pulmonary disease (‘COPD’). There was a modest setback recently as Sanofi and partner Regeneron (REGN) announced that the PDUFA date for this indication was extended by three months by the FDA, as the agency requested additional efficacy analyses. The two companies remain confident in the efficacy and safety of Dupixent in this patient population, and I agree, as both efficacy and safety looked strong in the two phase 3 trials. I wrote about this opportunity from Regeneron’s side in last year’s article.

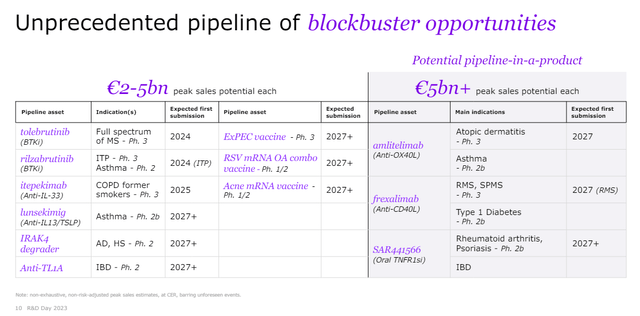

There are many “mini-blockbuster” assets in Sanofi’s pipeline capable of generating low to mid-single-digit billions in annual peak sales, and they are shown in the R&D day presentation slide below.

Sanofi R&D day investor presentation

Analysis of these smaller pipeline products is beyond the scope of this article, but they are worth mentioning, and I do want to say a few words about the three big ones – amlitelimab, frexalimab, and SAR441566.

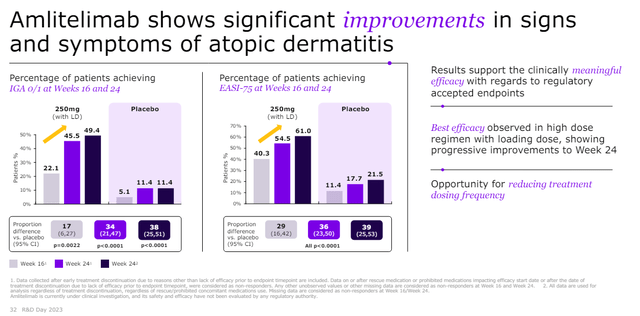

I am bullish on the OX40 class and Sanofi and Amgen (AMGN) are leaders here with amlitelimab and rocatinlimab, respectively. The development timelines of the two candidates are similar, and the addressable markets are very large. Sanofi says amlitelimab falls in the group of candidates with greater than EUR5 billion in annual peak sales.

Both amlitelimab and rocatinlimab have demonstrated excellent efficacy and good safety in atopic dermatitis patients with high EASI75 scores of amlitelimab in the phase 2 trial. Phase 2 results of amlitelimab in atopic dermatitis patients are shown below.

Sanofi R&D day investor presentation

Sanofi has an aggressive and broad development program that also targets asthma, hidradenitis suppurativa, alopecia areata, celiac disease, and systemic sclerosis. Phase 2b results in asthma patients are expected in the second half of the year, phase 2 results in hidradenitis suppurativa in 2025 and phase 3 results in atopic dermatitis patients in 2026.

Frexalimab is an anti-CD40 ligand antibody, and it is in development for the treatment of multiple sclerosis (‘MS’), type 1 diabetes, Sjogren’s syndrome and systemic lupus erythematosus (‘SLE’). Sanofi recently reported promising phase 2 results of frexalimab in MS patients, but there is a long wait for the phase 3 results which are only expected in the second half of 2027, and so are the phase 2b results in type 1 diabetes patients. However, there are upcoming minor catalysts over the next 12 months – phase 2a results in Sjogren’s syndrome in 2H 2024 and phase 2a results in SLE in 1H 2025.

These are all relatively large specialty markets and I believe success in two out of four indications will be sufficient to get frexalimab above Sanofi’s EUR5 billion-plus annual sales guidance, and all four would probably push the number closer to or above EUR10 billion.

SAR441566 is a “differentiated oral TNFR1 signaling inhibitor with potential for antibody-like efficacy” and Sanofi also claims it could have lower infection risk than TNFα antibodies because of the binding to R1 that still allows membrane-bound TNFα to bind to TNFR2 to conduct homeostatic functions.

This sounds promising in theory, especially considering the markets this candidate is going after are dominated by the formerly largest drug in the world the TNFα antibody Humira. It is still early, though, and all Sanofi showed to date is preliminary efficacy signal and good safety in patients with mild to moderate psoriasis in the phase 1b trial. 2025 will be an important year for SAR441566 as we should see phase 2b results in two large indications – psoriasis and rheumatoid arthritis. Showing antibody-like efficacy with improved safety would be a big win for this candidate.

Efforts in oncology probably need some extra work. There is not much in the advanced pipeline other than Sarclisa, but there is an emerging early-stage pipeline of antibody drug conjugates (‘ADCs’) and NK cell engagers.

Business development is another important long-term growth driver

In addition to the healthy immunology pipeline, we should see business development transactions that should complement the product portfolio and pipeline. Management seems more focused on bolt-on deals in the range EUR2 billion to EUR5 billion, but they are not excluding the possibility of larger deals should one come along. For example, it is public knowledge that Sanofi was one of the potential acquirers of Horizon Therapeutics in late 2022, but Amgen ended up buying Horizon for $28 billion.

And the balance sheet is strong enough to do both, as net debt at the end of Q1 was relatively modest at $8.5 billion.

Another way to free up some cash is the spinoff of the consumer unit. This unit generated $5.6 billion in net sales in 2023 and earlier this year, it was reported that Advent International and Blackstone are among the interested parties that could value the consumer unit at over $20 billion.

Overall, I would expect Sanofi to be an active M&A participant in the following quarters and years, especially if the spinoff of the consumer unit is successful.

Other possibilities for the use of cash are increasing the dividend and doing buybacks.

Risks

Making a bold choice to invest more in the business creates heightened execution risk, and there are no guarantees the increased pipeline investments will bring good results and value creation.

The balance sheet is in good shape, and the risk here is the company making poor business development decisions. I am not super-confident the company will make the right choices, and I am not thrilled by the choices it made over the last few years. But I think Sanofi can do better deals going forward.

Increasing competition is also a medium and long-term risk. Many companies are going after the same targets and the same diseases, including those currently dominated by Dupixent and targeted by pipeline candidates such as amlitelimab and frexalimab.

Unlike many other big pharma companies, Sanofi does not have big patent cliffs anytime soon and the key product Dupixent has a healthy IP position with exclusivity likely going out to the late 2030s.

Conclusion and upside potential

Last year’s decision to increase investments was a bold move, but I believe it is the right one if Sanofi wants to deliver decent long-term shareholder gains. There are no patent cliffs to worry about, and the immunology business should carry the company forward. The healthy pipeline coupled with bolt-on deals and an occasional larger deal should create a good mix of upside drivers to future expectations.

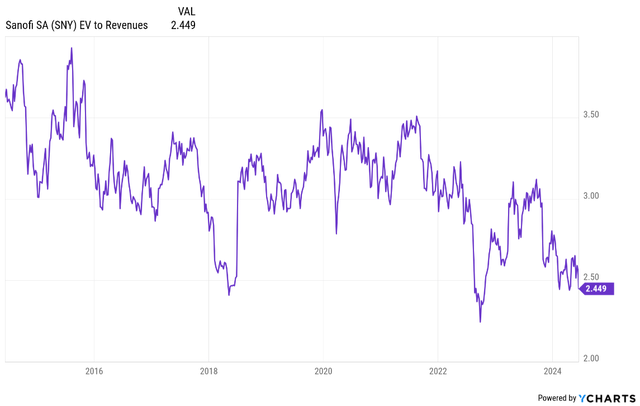

Based on the current setup, I believe the stock can re-rate back to an EV/revenue ratio of at least 3.5, driven by mid-single digit topline growth and up to high single-digit bottom line growth. Based on the current growth estimates, this translates to low double-digit share price CAGR (inclusive of dividends) through the rest of the 2020s. I believe the risk-reward looks good with limited downside given the historically low valuation, the expected growth profile and a lack of true binary events such as losses of exclusivity for key products and the lack of make or break clinical trial readouts.

Ycharts

There is also an upside scenario if topline growth goes up to the high single digits or low double digits and bottom-line growth in this case reaches the low double digits or mid-teens, driven by pipeline wins, good acquisitions for revenue growth upside, and, on the earnings side by the recovering margins after the recent compression led by increased investments. In this case, the compounded annual growth rate could go up to the high teens.

Read the full article here

")

(NASDAQ:SOFI)")

")

")