")

Want to see what all the fuss is about, but all out of gold-pressed latinum? The full first season of Lower Decks is free on YouTube to watch")

")

The decline in interest rates that has fueled an interest in REITs like Simon Property Group, Inc. (NYSE:SPG). But that trend, in general, has paused. That pause will likely continue until the Federal Reserve feels comfortable resuming the downtrend. For the rest of the current fiscal year, that appears to be unlikely. Therefore, the stock may be caught in a relative trading range for at least the rest of the year and maybe longer.

Lastly, the first quarter was off to a great comparison and guidance was raised. But that all happened because of a onetime sale that implies a tough comparison in the first quarter of the next fiscal year. That first quarter is coming up fast and may well be reflected in stock price action as the first quarter gets closer because the stock market looks forward.

Simon Property Group mentioned that the CEO is undergoing cancer treatments. At the same time, it was announced that Eli Simon, the son of David Simon was elected to the board of directors. But should things turn out worse than expected, the record of really anyone trying to fill the shoes of someone like David Simon is at best mixed. In fact, it is usually a good deal worse than “mixed.”

High-Quality Reputation

There are many reasons to believe that this issue will remain a high-quality issue for some time. Much of the advantages possessed by the company come from its diversification, its size, and the location of its properties. That is not easily undone, and it can result in years of satisfactory investment performance just by keeping what the company already has going.

Much of the time, a successor will continue the company policies in place as long as the CEO is around, and that sometimes happens for a while after there is a change in CEO’s.

This is the real estate business, and the company has locations that have long outperformed competitors. That is a situation that will not change overnight. Instead, what is more likely to happen is steady growth combined with the dividend climbing. Management and management policies of such a business are unlikely to change significantly for at least a year or two, no matter what lies ahead.

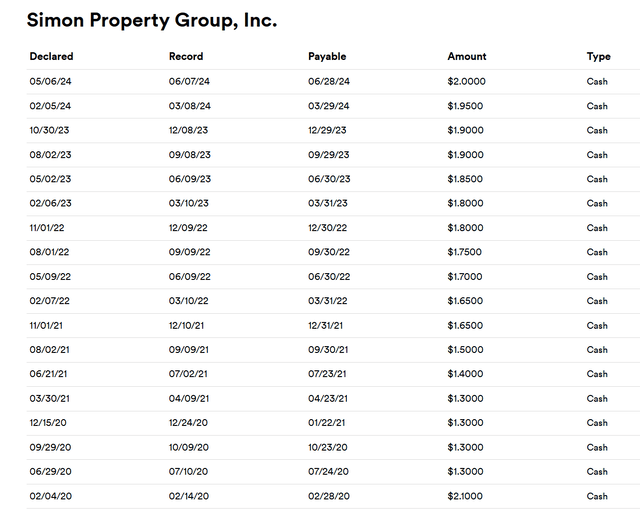

Dividend History

Management again increased the dividend as that dividend gets closer to the level paid before the latest dividend cut.

Simon Property Group Dividend History (Simon Property Group Website June 26, 2024)

The dividend should eventually surpass the level paid a few years ago if this management has been working on increasing business profitability as it has in the past.

The dividend yield is historically high. But the news on the health of the CEO could well stop the rally of the stock price “in its tracks” until there is more clarity about the situation.

I previously thought there was “a lot more where that came from” but that was dependent upon key management remaining in the status quo. A cancer diagnosis is an extremely significant variance that is likely to change the future outcome. It may well change the present stock price outlook as well.

While I believe that the business can continue on the same track for at least a few years if the worst happens. New management will need to take that time to demonstrate at least a reasonable level of skill comparable to what has existed until now. It is very rare to have two skill levels in a row comparable to what David Simon has done for this company.

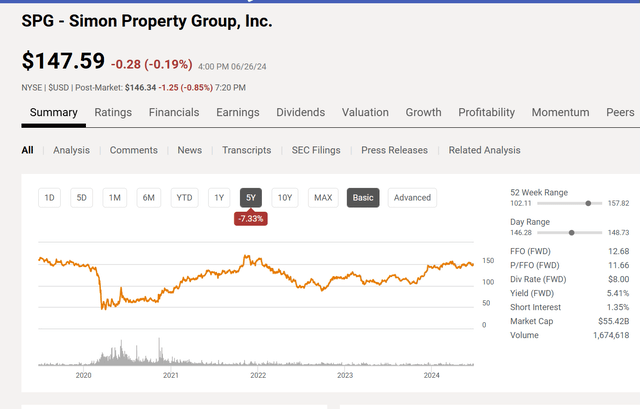

Stock Price

The stock price has not only been higher in the past, it has also had a higher valuation attached to it.

That higher valuation occurred when interest rates were lower. Since interest rates appear to be “stuck” where they are right now, the stock price may well be the same.

While this company has an excellent debt rating and access to debt markets on good terms virtually at will, there is a market fear that years of inflation could force enough debt to be refinanced at higher rates to detract from future earnings progress (and cash flow progress).

Simon Property Group Dividend History (Seeking Alpha Website June 26, 2024)

The problem with comparing much of anything to the past is that management records largely determine whether a stock performs well or exactly what valuation is appropriate. If there is a risk of management change (as there is now), then the future valuation and the evaluation of the stock as a potential bargain can be quite uncertain.

There will clearly be some market emphasis on performance. But there will also be a demand for management clarity going forward. That uncertainty combined with current market conditions point to a stock price “stall.”

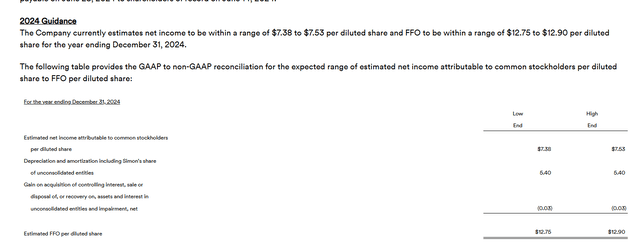

First Quarter Results

Meanwhile, the company was off to an excellent start and began the fiscal year by raising guidance based upon that excellent start.

Management mentioned that a one-time gain fueled the positive comparison. There was a sale of the remaining interest in the “Authentic Brands Group” that resulted in a significant first quarter gain. This gain resulted in a large positive earning per share comparison with the quarter in the previous fiscal year. It also will set cash flow for a good gain as well in the first quarter. Now, due to the one-time nature of the event, it could make for a difficult first quarter comparison in fiscal year 2025.

Simon Property Group First Quarter 2024, Guidance Revision For The Fiscal YearvSimon Property Group First Quarter 2024, Guidance Revision For The Fiscal Year (Simon Property Group First Quarter 2024, Earnings Press Release)

Cash flows in the business are fairly predictable, as are expenses when the company is large and well diversified. It would take a major change in the short-term economic outlook to cause a major revision to the figures shown above. So far, that is “not in the cards.”

But the other consideration is that many of these REIT’s have some sort of inflation protection built into the contract. Inflation has declined, therefore earnings growth from that inflation protection will also decline. Since this market is oriented towards positive earnings comparisons and earnings growth comparisons, a decline in the earnings growth combined with a maintenance of interest rates may well cause the market to ignore this issue for a while.

Risk

By far the biggest risk would be the loss of the services of David Simon. This business has long been very private about the family in general. That does not bode well for the communication of the health progress of David Simon. Investors need to evaluate this investment as the future unfolds according to their own risk tolerance. Currently, it is difficult to tell what decision is the right decision.

Even though David Simon plans to continue as CEO, Chairman of the Board, and President, conservative investors may want to look for an exit while the rest of us may pause our respective strategies to try and determine the effect of the treatments on the future of the company. This is because a situation like this may well meet the “loss of services” of a critical person to the company, even though the person remains on the job.

Ideally, a succession plan should be similar to the one Cenovus Energy (CVE) has in place, where the CEO was promoted to the board and another person became CEO. The two have been working together for some years and the training will continue. As the Bob Chapek and Bob Iger situation at Disney (DIS) firmly demonstrated, the CEO has a rather dramatic and somewhat immediate effect on company prospects. This is why a plan needs to be in place. It is not enough to simply announce a successor.

In particular, the quant system outlook almost does not apply until the outcome of the cancer situation is known (and if needed the successor leadership is in place). At that point, a comparison can be made with the past to determine what measurements from the past are relevant.

Simon, the company, itself has some major location advantages and the advantages of size and diversification. But depending upon the future of David Simon, a less capable CEO may be making decisions in the future that could materially set the company back or do worse.

Any company can only grow as large as management is capable of growing it. But right now, we do not even know the future of the current management in place. Therefore, future projections have more risk than would currently be the case.

Summary

The business itself is healthy and Simon has locations that outperform competitors. However, the force behind recent earnings growth was a decline in vacancies caused by the covid challenges combined with inflation protection that is evident in many of these types of agreements.

All of this is likely to lead to a decline in earnings progress in the future compared to the progress made immediately after covid. Should interest rates remain higher for as long as the market fears or longer, there could be pressure on earnings. I, personally, give little weight to interest rate fears because usually the wait for a resumption in the decline of inflation is months, not years. However, right now, the market disagrees with me, and Mr. Market will likely continue to disagree with me for some time.

The health of the company’s CEO impairs the good news that are part of the first quarter earnings report.

Presently, I would consider this a hold for a few months to maybe a year and conservative investors may want to place their money elsewhere as this issue may be stuck in a trading range for a while. As usual, the business is good. But it is not growing so fast as to demand a growth premium to the current price.

Read the full article here

")

")

")

")