")

2023 winning Pueblo Chili cook off contest green chile recipe, non-commercial category. It’s called Pueblo green chile for a reason, this recipe is a one pot solution with 4 lbs roasted, peeled, diced green chile")

")

Introduction

If you’ve been reading my articles for a while, I think you know that I’ve been advocating looking at the S&P 500 Index (SP500, NYSEARCA:SPY) constructively and not buying the index itself in ETF format, but instead focusing on individual names (with a clearer bias towards value). Contrary to my expectations and the expectations of other skeptics regarding the high probability of an imminent SPY correction, the index has continued to update its ATHs as expectations have risen regarding the growth of artificial intelligence and its role in the future of operational efficiency and thus higher margins and corporate profits.

Seeking Alpha, my coverage of SPY

Despite its exceptional strength of late, I think the S&P 500 index is likely to feel a spike in volatility shortly – on the eve of the US election this is the norm, plus the seasonal factor suggests a high probability of this event. My basic recommendation for today is to be prepared for increased volatility soon, and not to be fooled by excessive growth optimism.

Why Do I Think So?

Just yesterday, June 27, the presidential election debate cycle began. I don’t want to draw any political conclusions here, but rather take a look at the history of how debates influence the behavior of stock market indices.

TME newsletter, Barclays [proprietary source]![TME newsletter, Barclays [proprietary source]](https://static.seekingalpha.com/uploads/2024/6/28/49513514-1719562683660611.png)

According to analysts at Barclays (proprietary source), the S&P 500 index is at least in a slight correction 10–15 weeks before the actual election day, although it usually rises rapidly after the election day, based on the last 4 cases. Currently, we see the SPY breaking out to the upside, but if the experience of the last 2 decades is anything to go by, we are already approaching a short-term turning point.

A look at the S&P VIX Index (VIX) confirms the thesis that the S&P 500 Index is likely set to surprise investors negatively due to 2 main factors. Firstly, the VIX is currently at its locally very low levels – the probability of an upward movement is rising sharply.

Seeking Alpha, VIX

Second, going back to the election as the main catalyst for the VIX rise, history helps us to better recognize the probability that exists. According to Nomura (proprietary source), options markets tend to price in the presidential election ~3 months before the event, and that hasn’t happened yet, but we’re rapidly approaching that upcycle:

Nomura [June 24, 2024], proprietary source![Nomura [June 24, 2024]](https://static.seekingalpha.com/uploads/2024/6/28/49513514-1719562284959168.png)

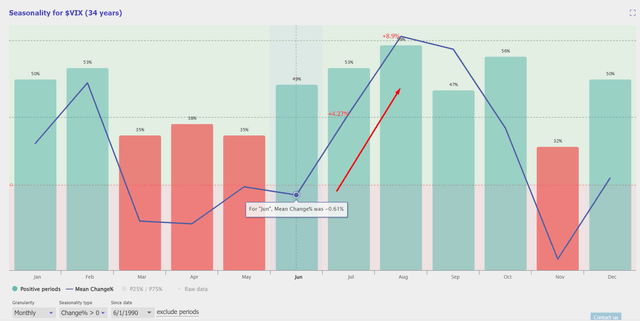

The probability calculated considering the fact of the election year is also confirmed in the sample without this criterion: If we look at the June 1990 data, we see that the VIX has the highest seasonal odds of a rapid expansion in the next 8 weeks, with median expansions of 4.27% in August and 8.9% in September.

TrendSpiders Software, the author’s notes

Every statistical pattern must have a logical basis. I attribute the rise in volatility in presidential years to the increasing uncertainty that always spooks markets. The principle at work here is similar to uncertainty in corporate earnings: If investors can’t properly calculate what the chances are that the profits from their investment will continue to grow in the future, they prefer to trim, which leads to increased volatility. The same thing usually happens with broad-based ETFs. However, this is not yet the case if you look at this Goldman Sachs data (proprietary source) showing the further expansion of market participants’ cumulative equity positions ahead of the elections.

TME newsletter, Goldman Sachs data [proprietary source]![TME newsletter, Goldman Sachs data [proprietary source]](https://static.seekingalpha.com/uploads/2024/6/28/49513514-17195694458430877.png)

The discrepancy that exists today between the historical and current behavior of the index provides an excellent opportunity to hedge against the highly likely increase in volatility in the foreseeable future.

The Verdict

From what I see today, the market seems completely unconcerned and unprepared for the uncertainty that the pre-election period usually brings: Neither the price action nor the cumulative flow to US equities suggests that anything ominous could be waiting on the horizon for investors. However, a statistical pattern is crying out for it, both in terms of the historical momentum of the S&P 500 Index and the setup that has formed in the VIX.

Therefore, I conclude that while optimism still prevails, it is unlikely to last too long – the logic that explains past patterns is still valid, and therefore US equities should dive into a correction or consolidation (at least in the short term). Therefore, I urge investors to be vigilant and not increase their equity exposure even if this asset class looks strong today.

Thank you for reading!

Read the full article here

")

")

")

")

")