")

Introduction

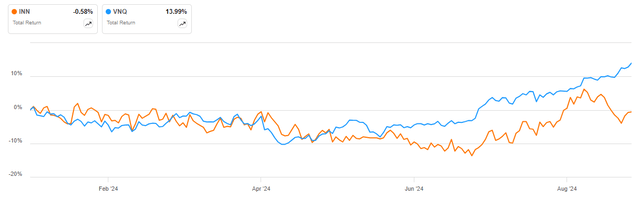

Summit Hotel Properties (NYSE:INN) has substantially underperformed the Vanguard Real Estate Index Fund ETF (VNQ) so far in 2024, with the shares delivering a ~1% loss against the ~14% gain for the benchmark ETF:

INN vs VNQ in 2024 (Seeking Alpha)

This has resulted in the REIT trading at a discount to larger peers, whether you look at its AFFO multiple of 6.8x or the market-implied cap rate of about 10.3% before capital expenditure. Coupled with a debt-heavy capital structure and 24% floating-rate debt, I think Summit Hotel Properties is worth a Buy rating and should outperform going forward.

Company Overview

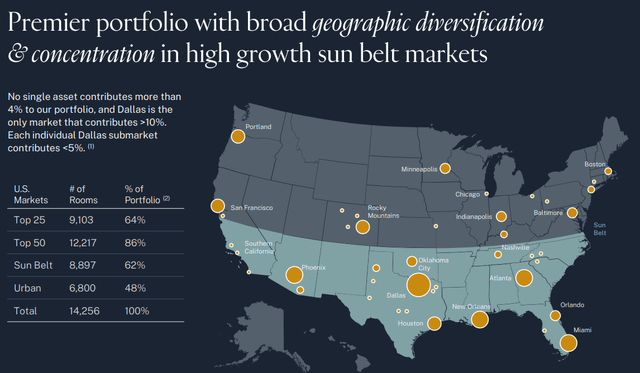

You can access all company results here. Summit Hotel Properties is a lodging REIT with significant exposure to the Sun Belt region which accounts for 62% of all rooms operated by the company:

Portfolio overview by market (Summit Hotel Properties September 2024 Presentation)

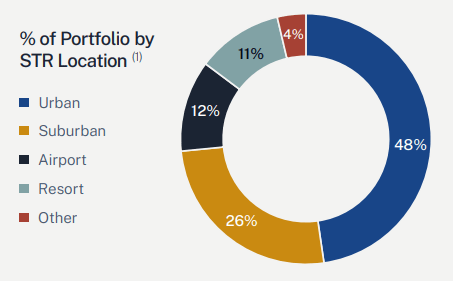

Summit Hotel Properties focuses primarily on Urban (48% of all rooms) and Suburban (26%) locations, with 95% of all hotels operated under the Marriott, Hyatt, and Hilton brand:

Portfolio overview by hotel location (Summit Hotel Properties September 2024 Presentation)

Operational Overview

In Q2 2024 Summit Hotel Properties delivered RevPAR growth of 3.4% Y/Y, driven by a higher occupancy (+2.4% to 77.7%) and a higher ADR (+0.9%).

Adjusted FFO grew 9.7% Y/Y to $0.29/share as the company benefitted from lower operating and interest expenses.

During the quarter the company sold 3 hotels at a 6.8% capitalization rate, generating $84 million in proceeds and a net gain of $28 million.

In its September 2024 presentation, the REIT reported that RevPAR growth decelerated to 1.50-2.00% in July and August.

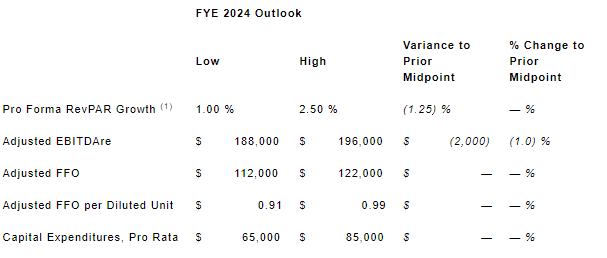

Reduced 2024 Outlook

Given the moderating RevPAR growth the REIT cut its full-year 2024 RevPAR growth outlook to 1.00-2.50%:

Reduced 2024 Outlook (Summit Hotel Properties Q2 2024 Results Press Release)

Taking into account that RevPar growth in H1 2024 was 2.3% and the above-mentioned RevPAR increase in July and August of 1.50-2.00%, I expect RevPar growth to land at the high end of the company’s 1.00-2.50% full-year outlook.

It is encouraging to see that the adjusted FFO outlook is unchanged, resulting in a $0.95/share midpoint for 2024, or a 6.8x multiple, which is quite attractive for a commercial REIT.

Capital Structure

Summit Hotel Properties ended Q2 2024 with a net debt of $1 billion (after deducting $300 million of debt owed by joint venture partners). The company also has $310 million in preferred shares outstanding. Combined with the $800 million market capitalization (cumulative common shares and units outstanding totaled 124.22 million) the REIT’s enterprise value stands at about $2.1 billion. Net debt accounts for 48% of enterprise value, implying that the REIT is well-positioned to benefit from real estate cap rate compression as the Fed normalizes monetary policy, although leverage is by no means excessive.

Accounting for the effect of interest rate swaps, 24% of debt is floating rate. While forward interest rate expectations are quite dynamic, futures markets currently predict a Fed funds rate of about 3% in July 2025. I estimate this would lead to interest rate savings of about $5.4 million on an annualized basis, or $0.04/share, representing a 4.5% boost to the $0.95/share 2024 adjusted FFO midpoint.

Looking ahead to February 2026, adjusted FFO will likely come under pressure as the company will have to refinance a $288 million convertible note which currently carries an interest rate of 1.50% and is highly unlikely to be converted into common stock.

Market-implied cap rate

Considering that adjusted FFO is likely to increase in 2025 before dipping in 2026 as the company manages its debt burden, looking at an enterprise-level valuation metric such as the market-implied cap rate may provide a better perspective.

I estimate that on a run-rate basis, the REIT will generate $118 million in adjusted FFO, pay some $83 million in interest, and distribute $16 million in preferred dividends. As a result, cumulative cash flows to enterprise value should total approximately $217 million, which against an enterprise value of $2.1 billion represents a market-implied cap rate of 10.3% which is very attractive for a commercial REIT as it already incorporates management overhead except equity-based compensation which is added back to adjusted FFO as is standard practice with REITs.

The capital expenditure budget stands at about $75 million, indicating a 6.8% market-implied cap rate after capex which is also quite attractive.

Valuation and prospects

To put Summit Hotel Properties’ valuation in context, especially its 6.8x adjusted FFO multiple, you may refer to Dane Bowler’s article which puts the market cap weighted average AFFO multiple at 19.87x for US REITs. Clearly relative to large-cap REITs Summit Hotel Properties trades at a steep discount. The valuation discount can be explained by a higher market-implied cap rate (between 6.8% and 10.3% as calculated in the previous paragraph), higher-than-average leverage, and small company size (smaller REITs traditionally trade at a discount).

At the same time, smaller REITs such as Summit Hotel Properties tend to have more floating rate financing compared to larger peers. As such, I expect Summit Hotel Properties to show stronger AFFO growth as the Fed normalizes policy.

To summarize, considering the company’s valuation and its capital structure, I think Summit Hotel Properties is worth a Buy rating and should outperform real estate peers going forward, especially larger ones.

The preferred shares

I reckon the 6.25% Series E (INN.PR.E) and 5.875% Series F (INN.PR.F) preferred shares present decent income opportunities but given the enterprise-level valuation are inferior to the common stock which should deliver higher returns albeit with a larger risk. If we do see an uptick in the company’s enterprise-level valuation though, both preferred series offer some capital appreciation potential down the line. For the time being, I would rate them a Hold.

Risks

The key risk facing Summit Hotel Properties is a potential recession which will reduce demand for hospitality services, severely affecting RevPAR growth. The effect of an economic downturn may be mitigated by looser Fed monetary policy as the unemployment rate is a key consideration for the Fed after the recent slowdown in inflation dynamics.

The other key risk to mention is the aggressive Fed easing priced by markets by July 2025, with the Fed funds rate seen at about 3%. If the Fed does cut rates as markets currently predict, it will boost Summit Hotel Properties’ AFFO and allow the company to refinance its big February 2026 maturity at favorable terms. If the Fed does not reduce interest rates, I would expect adjusted FFO to face significant headwinds in 2026 as the convertible note is refinanced.

I would also note that longer-term RevPAR growth should be driven by increases in the ADR rather than a higher occupancy, which was the case in Q2 2024. Unless ADR growth picks up, we could see much weaker RevPAR growth in 2025.

Conclusion

Summit Hotel Properties reported strong AFFO growth in Q2 2024 but cut its full-year outlook for RevPAR growth as the outsized 3.3% Y/Y RevPAR increase in Q2 2024 should prove temporary.

Nevertheless, I think the REIT is attractively valued in terms of adjusted FFO multiple (6.8x) and market-implied cap rate (10.3% before capex), which coupled with its debt-heavy capital structure should help it outperform larger real estate peers which account for the majority of VNQ holdings.

Thank you for reading.

Read the full article here

")

(NASDAQ:CGBD)")

")

")