")

Investment overview

I wrote about Tenable (NASDAQ:TENB) previously (21st Feb 2024) with a buy rating as I expected strong growth momentum going into FY24 and strong long-term growth ahead, supported by growing demand for cybersecurity. I remain buy-rated for TENB as I see continuous strength in demand, especially in the enterprise market, and that TENB’s Tenable One continues to win deals, which opens up more upsell opportunities.

1Q24 earnings (announced on May 1)

TENB reported strong revenue performance of $216 million (14.4% y/y growth), which beat the high end of management’s guidance and consensus estimates of $213.6 million. Adj gross margin also came in higher than expected at 80.9% vs. 79.6%, with absolute gross profit dollars of $174.7 million. As a result, adj EBIT came in at $37 million, which was much higher than the high end of management’s guidance ($27 million to $29 million). Finally, adj net profit saw $30.4 million, which also beat guidance and consensus estimate of $21.3 million.

Notably, subscription and maintenance y/y growth rate accelerated in 1Q24, breaking the 10% threshold line for FY23, suggesting momentum despite what seemed to be a tough macro environment of high rates. In my opinion, the highlight of the quarter was really profitability, where TENB beat consensus EBIT margin expectations by ~500bps. Given the strong set of results, management raised FY24 guidance across the board, now expecting revenue between $900 and $908 million, adj earnings of $135 million and $140 million, adj EBIT of $158 million and $163 million.

No signs of weakness and execution remains on point

TENB 1Q24 performance was nothing but spectacular, and I don’t see any signs of weakness at this point. When compared to peers, TENB outperformed as well; both Rapid7 (RPD) and Qualys (QLYS) saw 12% y/y growth (TENB outperformed by 240 bps). In terms of growth momentum and outlook, I believe the underlying strength remains strong, and this can be seen from: (1) where the demand strength is coming from; and (2) 1Q24 close rates.

On the one hand, it was very positive to know that the enterprise market is the main source of strength. The reason I say this is because large companies are often the first ones to splurge in a macro recovery (as they have the financial resources), and I take this as a strong sign that large enterprises remain confident in a recovery ahead. For reference, TENB saw great traction with six-figure deals and also saw ~30% y/y increase in ACV from new clients. They also added 410 new enterprise platform customers this quarter, 31 more than in 1Q23. Moreover, enterprise sales represent around 60% of TENB sales; hence, it is good to learn that TENB’s largest market is thriving. Regarding close rates, performance was solid. 1Q24 saw relatively high close rates (60 to 70%) in recent years, even when compared to 1Q22, where TENB saw its highest y/y growth. This tells us that execution has been on point.

I expect growth momentum to continue into 2Q24, with potential for y/y growth rates to further accelerate, as growth in 1Q24 could’ve been better if not for the continuing resolution [CR] by the Feds. Assuming CR goes away and TENB is able to tap into the full strength of the public market, which was noted to be exceptionally strong during the call, TENB should easily see growth accelerate.

Funds are starting to open and flow down to different agencies. Activity around customers is as strong as we’ve ever seen in Federal. So we’re certainly excited. We think we’re providing a bullish outlook on the year and certainly a good start to it with regard to our results for the quarter. Company 1Q24 earnings

Tenable One continues to perform

The most important highlight of TENB performance, which instills confidence in growth ahead, is Tenable One, which continues to see healthy traction in 1Q24, growing to 26% of total new business, up from 22% last quarter. I continue to see plenty of runway for incremental penetration for Tenable One, which provides improved economics over standalone vulnerability management [VM], as the selling price is 70% higher (according to the 3Q23 earnings call).

My view is that Tenable One is going to help TENB win more deals because it offers a strong value proposition to customers and provides more bundling and upsell opportunities, and there are two evidences of this. Firstly, as noted above, Tenable One continues to take up a larger share of total new business, now representing 26% of total new business (which means Tenable One is clearly offering strong value). Secondly, exposure solutions, which include Tenable One and standalone cloud security, identity security, and operational technology security, represented ~50% of total new business in the quarter. This shows that TENB is the main driver for exposure solution growth (26%/50%). If you recall what management said in the 3Q23 earnings call, they commented on Tenable One opening up upsell opportunities. Hence, my belief is that as Tenable One continues to gain traction, TENB is able to take advantage of this landing phase to expand (upsell) other products.

This is also why the integration of Ermetic with Tenable one is very important, and encouragingly, it continues to progress. Ermetic is an agentless solution that adds a broad set of cloud-native application protection platform [CNAPP] capabilities, including identity cloud management, risk analysis, discovery, and compliance. This opens up TENB to tap into the very fast-growing market of the cybersecurity space. Due to their complexity and increased attack surface, cloud-native applications pose a new security risk. The visibility and control provided by traditional security tools are severely limited when it comes to cloud-native architectures. CNAPP provides a means to simplify things while enhancing safety and the developer’s work. According to P&S Intelligence, the CNAPP industry is expected to continue compounding at 20% per year until the end of this decade.

Valuation

May Investing Ideas

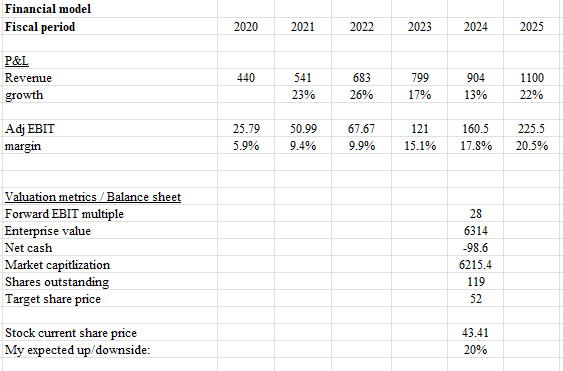

Based on my research and analysis, my expected target price for TENB is $52.

- I improved my growth outlook for TENB by $4 million in FY24 to reflect the improved FY24 guidance and 1Q24 strong performance, but kept my FY25 revenue estimates the same as prior as I like to wait for more evidence that Tenable One is able to drive more upsell opportunities, which will make me more bullish for FY25.

- I improved my adj EBIT margins for FY24 and FY25 by a similar amount to reflect the improved FY24 guidance (an improvement of 40bps)

- My valuation expectation for TENB has been downgraded from 35x forward EBIT to 29x forward EBIT, not because TENB performance is weak. But rather, it’s because the industry that TENB competes in (with RPD and QLYS) has seen a de-rating over the past few months, from ~30x to 22x today, and this has dragged down TENB’s multiple as well. That said, because of TENB’s stronger performance and my positive outlook, I expect TENB to continue trading at its historical premium of ~25%, which translates to a multiple of 28x forward EBIT.

Risk

TENB’s net dollar retention rate [NDRR] declined sequentially to 109% in 1Q24 from 111% in 4Q23. While it was mentioned that this was largely due to the business mix, which skewed towards more new deals, if NDRR continues to deteriorate, it could mean that TENB is seeing more churn than expected. While it is hard to ascertain the cause of this, the risk is that the market will further discount valuations to stay conservative.

Conclusion

I give a buy rating for TENB despite a slight valuation downgrade. The company continues to demonstrate strong growth momentum, exceeding expectations in its latest earnings report. TENB’s core business is healthy, with high close rates and increasing traction in the enterprise market. Tenable One, a key product offering, is gaining market share and presents significant upsell opportunities. While there are minor risks like a declining net dollar retention rate, TENB’s overall performance is impressive.

Read the full article here

")

")

")

")

")

")