")

My last article about UiPath (NYSE:PATH) on January 1, 2024, gave a buy recommendation for the stock for aggressive growth investors. On May 29, 2024, the company issued poor fiscal year (“FY”) 2025 revenue and operating margin guidance. The market began fearing some of the risks I briefly discussed in my last article, such as a poor macroeconomy, emerging competition, and generative AI possibly negatively impacting the Robotic Process Automation (“RPA”) market. Additionally, three months after accepting the position, Chief Executive Officer (“CEO”) and board member Rob Enslin suddenly resigned effective June 1, 2024. All of the above is terrible for a company with a limited operating history, such as UiPath. The stock dropped 34% after the company released its first quarter FY 2025 earnings report. Since my January 1 article, it is down around 48% compared to the S&P 500 Index (SPX), which has risen 15%.

However, there are still reasons some aggressive growth investors may want to buy it. The company has double-digit revenue growth, one of the best gross margins in the software/cloud industry, and growing free cash flow (“FCF”). Additionally, customers love the company’s products, as evidenced by one of the industry’s best gross revenue retention rates (“GRR”), which means UiPath retains most of its customers.

This article will review the company’s first quarter earnings report and explain in more detail why the stock has dropped since the beginning of the calendar year 2024. It will also review the risks and valuation and explain why aggressive growth investors can still buy the stock.

A brief review of what the company does

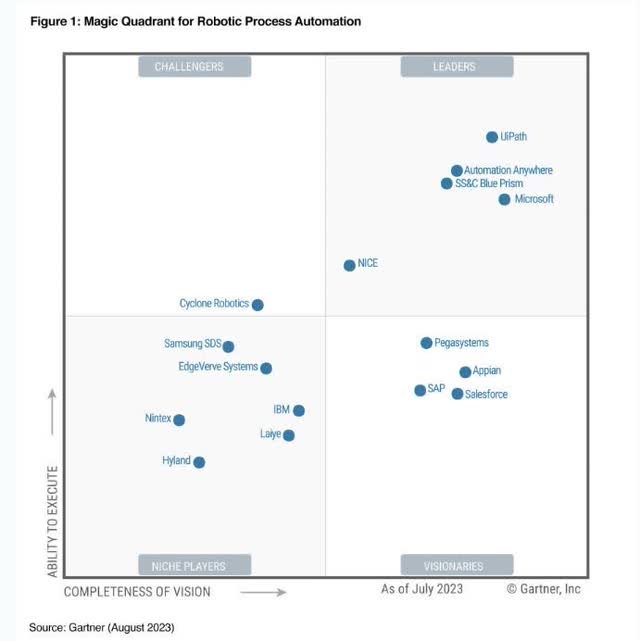

UiPath started in Romania as an early innovator in the RPA market in 2005. The company defines RPA as “a software technology that makes it easy to build, deploy, and manage software robots that emulate humans actions interacting with digital systems and software.” Over the last two decades, it has risen to the top of the market, and several analyst reports, such as Forrester Wave and Gartner (IT), rate it among the best RPA offerings. The following image shows UiPath is in the leaders’ Magic Quadrant for RPA.

UiPath website

The company didn’t get to a leadership position by accident. The company has expanded beyond the borders of what people call RPA. For instance, a Forrester Wave report has stated, “Today, UiPath is not only the largest RPA software vendor by revenue but has also evolved from an RPA pure play into what it refers to as a business automation platform.“

A mixed earnings report

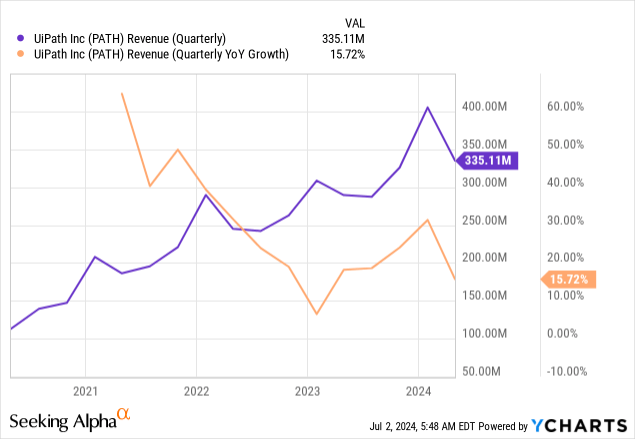

UiPath generated revenue of $335 million in the first quarter of FY 2025, beating analysts’ estimates by $2.10 million. Revenue grew 16% over the previous year’s comparable quarter. Although 16% revenue growth is solid, it is a far cry from the heady 60% year-over-year growth the company delivered in calendar year 2021.

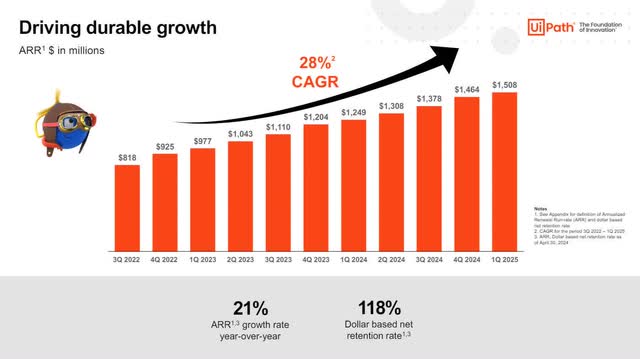

Annual Recurring Revenue (“ARR”) grew 21% to $1.508 billion, the low end of the company’s guidance. ARR represents the yearly value that a subscription or contract generates. Investors believe ARR will translate into a relatively predictable future income, and ARR’s growth (21%) compared to revenue (16%) is generally a positive indicator for future revenue growth.

UiPath First Quarter FY 2025 Earnings Presentation.

The company had a GRR of 98%, indicating that it keeps most of its customers. A GRR measures the percentage of recurring revenue retained from customers over a specific period after subtracting churn or upgrades. Its Dollar-based net retention rate (“DBNRR”) was 118%. UiPath’s DBNRR is the percentage rate of net ARR expansion from existing customers over the trailing 12-month (“TTM”) period. You can calculate this number by dividing the Total Current Period ARR TTM by the Total Prior Period ARR TTM times 100. A DBNRR of 118% means existing customers spent 18% more over the previous comparable period. While this number is solid, the following table shows a declining DBNRR since the fourth quarter of 2022. Since the GRR remains high at 98%, existing customers are likely reducing their spending levels. Possible reasons for the lower spending include companies wanting to save money in an uncertain economy. If DBNRR continues to decline, it could be a leading indicator of revenue shortfalls, and operating results diving below expectations. Investors should closely monitor GRR and DBNRR in future earnings reports.

| Fiscal Quarter | GRR | DBNRR |

| Q4 2022 | 98% | 145% |

| Q1 2023 | 98% | 138% |

| Q2 2023 | 98% | 132% |

| Q3 2023 | 98% | 126% |

| Q4 2023 | 97% | 123% |

| Q1 2024 | 97% | 122% |

| Q2 2024 | 97% | 121% |

| Q3 2024 | 97% | 121% |

| Q4 2024 | 98% | 119% |

| Q1 2025 | 98% | 118% |

Management reported that in the first quarter of FY 2025, remaining performance obligations (“RPO”) rose 22% year-over-year to $1.101 billion. The company’s current RPO also increased 22% to $683 million. Its RPO growth rates are above the revenue growth rate of 16%, which is generally good as some people consider the RPO growth rate a leading indicator of growth, suggesting the potential for revenue growth to reaccelerate.

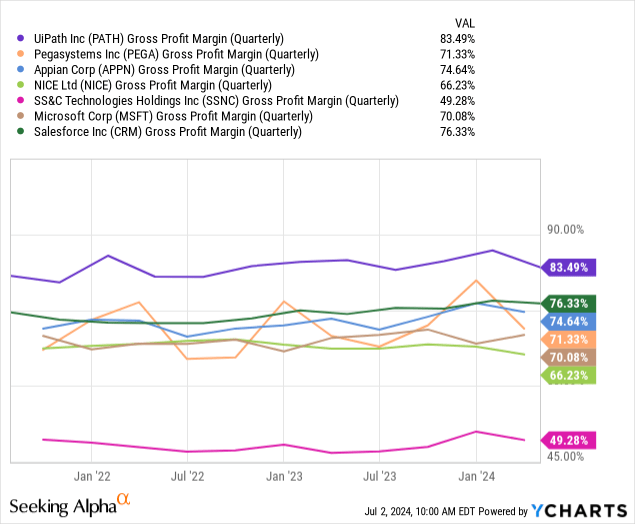

UiPath produced first quarter FY 2025 non-GAAP (Generally Accepted Accounting Principles) gross margins of 86% and GAAP gross margins of 83.49%, one of the highest gross margins in the cloud/software industry. The following chart compares it with other cloud/software companies that compete directly or compete with its automation software in adjacent markets.

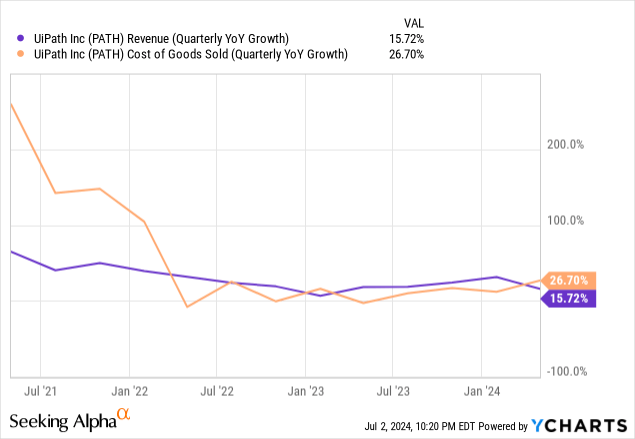

The chart below shows that the cost of goods sold (“COGS”) grew much faster than revenue, which is likely one reason why gross margins dipped from the fourth quarter. COGS growing faster than revenue can hurt profitability. Since early 2022, revenue growth has mostly exceeded COGS, and as long as these first-quarter results remain an outlier, the company should be ok. However, if COGS growing faster than revenue becomes a trend, the company will eventually have profitability problems.

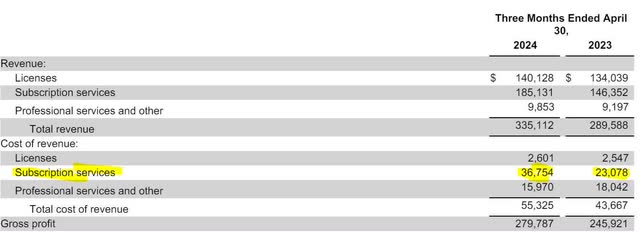

The image below shows that the biggest increase in costs of goods/revenue took place on the subscription services line. These costs typically include costs to develop the subscription services, data center costs, and customer support costs. Since management didn’t discuss why the subscription service cost of revenue increased, I won’t speculate. However, investors should be alert to these costs rising faster than earnings in future earnings releases.

UiPath First Quarter FY 2025 Earnings Release

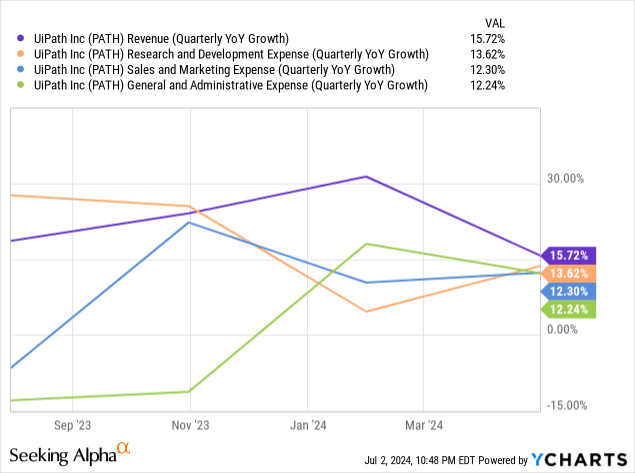

The following image shows that all operating costs are growing slower than revenue, which is an excellent trend showing that the company is becoming more operationally efficient. If the company can maintain a faster revenue growth rate than operating expenses, it portends good things for long-term profitability.

The company emphasizes non-GAAP metrics for operating income, likely because it has many one-time expenses. However, note that the company would be GAAP operating income profitable if it didn’t have $88.7 million in stock-based compensation. The second thing to notice in the following image is that the non-GAAP operating margin declined by 200 basis points year-over-year in the first quarter of FY 2025.

UiPath First Quarter FY 2025 Investor Presentation.

Analysts expect UiPath to reach full-year GAAP EPS profitability in 2027. Investors will likely need to be patient with this stock.

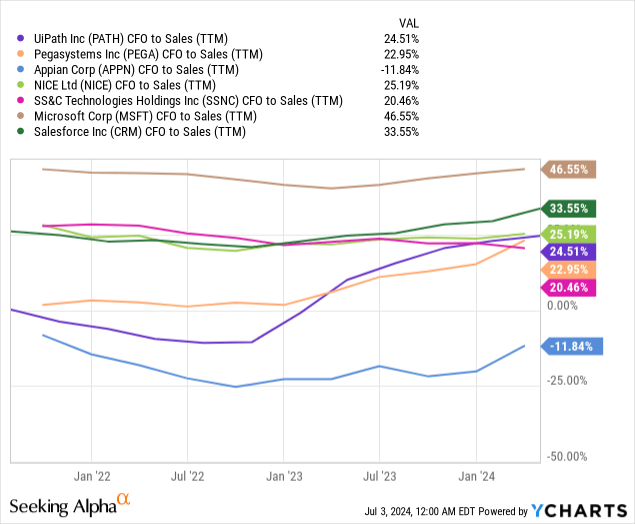

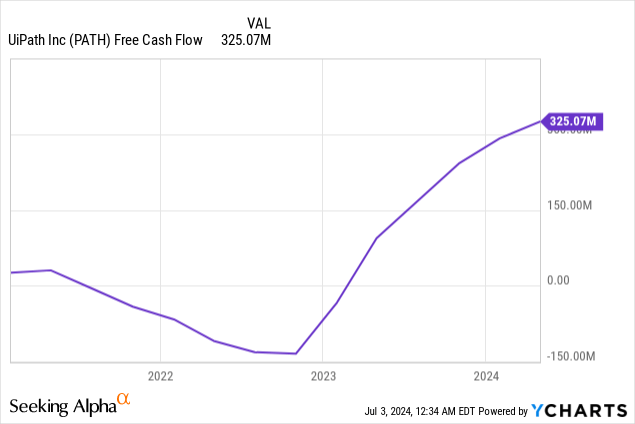

UiPath has a cash flow from operations (“CFO”) to sales of 24.51%, which means the company converts every $1 of sales to around $0.25 in cash flow. That is a decent amount at this stage of the company’s growth. As the company matures, I want to see CFO-to-sales expand to at least 35%, which would benefit FCF growth.

The company’s trailing 12-month FCF as of the first quarter of FY 2025 was $325 million. It had $1.936 billion of cash and short-term investments and no long-term debt at the end of the first quarter, so it should have plenty of resources to fund its near-term operations.

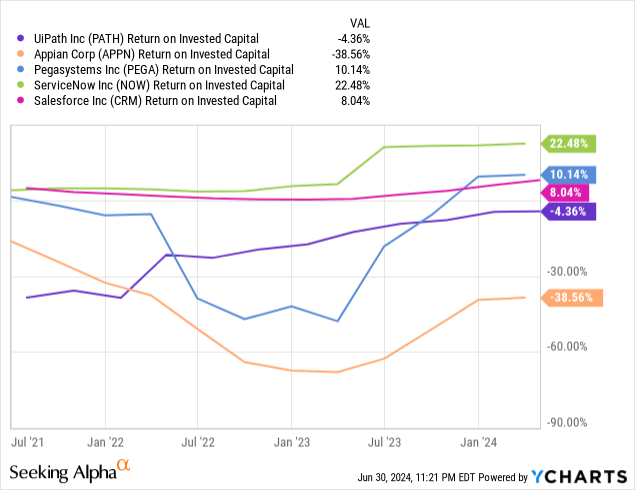

Last, the company has a negative return on invested capital (“ROIC”). Although the ROIC has been slowly rising, investors are unlikely to give companies with a negative ROIC the benefit of the doubt in a poor macroeconomy.

While the company’s first-quarter numbers were solid, the report showed several trends that are going in the wrong direction. Considering that the company gave terrible guidance, which this article will discuss in the next section, the market had good reason to sell off the stock post earnings.

Why the stock fell after earnings

The prime reason the market was disappointed with the first quarter FY 2025 report was that management slashed full-year FY 2025 revenue guidance by 963 basis points to $1.4075 billion at the midpoint and non-GAAP operating income guidance 51% to $145 million from its initial guidance given in the fourth quarter FY 2024 earnings release. The company also lowered its previous FY 2025 ARR guidance of $1.725 billion to $1.730 billion, down to a range of $1.660 billion to $1.665 billion, which implies full-year ARR growth of 14% instead of 18%. If the company hits its new ARR guidance, it will substantially drop from its FY 2024 ARR of 22%.

Some growth investors think it’s egregious that the company could reduce its guidance so much over the course of only three months. This guidance reduction reeks of a company unable to execute its vision.

UiPath first quarter FY 2025 earnings presentation.

The first reason Chief Financial Officer (“CFO”) Ashim Gupta gave for the company’s lowered guidance was a poor macroeconomy. He said at the William Blair 44th Annual Growth Stock Conference on June 6:

When you look at kind of Q1 earnings across many people highlighted somewhere around that mid-March — mid-March time frame. It just felt like the environment got tougher, longer deal cycles, more scrutiny on deals. That’s not about UiPath, I think that is more about just the environment that our customers are working through. And we saw the impacts of that, particularly with the impact of larger multi-year deals.

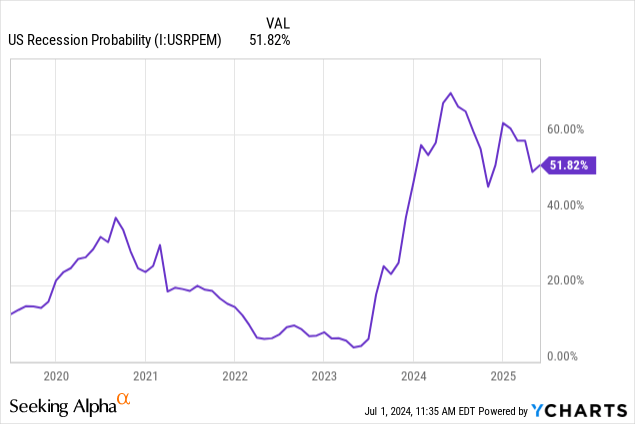

CFO Gupta may be correct in that statement. After all, enterprise software/cloud companies like Salesforce (CRM) said similar things about deals shrinking or lengthening sales cycles on large deals. EPAM Systems (EPAM), Veeva Systems (VEEV), MongoDB (MDB), and SentinelOne (S) also gave disappointing guidance. Enterprises may be reluctant to spend on software and cloud services, fearing a weak economy will eventually lead to a recession. Those fears may be justified. According to the Estrella and Mishkin method of forecasting recessions, the U.S. economy has a 51.82% recession probability. Until recession fears dissipate, some enterprise software/cloud companies may have issues growing their business.

However, some of UiPath’s issues were self-inflicted. The company blamed a lack of execution. At the William Blair conference, CFO Gupta said, “We just feel like we could have been deeper in the details on many — on our deals and some of the scrutiny that we have around it,” suggesting management had issues properly evaluating deals before closing, possibly leading to lower profitability. He also said that the company had problems managing “simple processes like sales compensation and just making sure we understood the downstream effects,” meaning the company’s new sales compensation plan may have had unintended adverse side effects on sales. Additionally, some of the company’s growth investments have so far underperformed.

CEO Rob Enslin’s departure after only three months on the job and the company’s re-appointing of the old CEO, Daniel Dines, who had only left three months before, created more uncertainty. For instance, why did CEO Daniel Dines really leave the company in the first place, and is he committed to fixing the company’s problems, restoring revenue growth, and keeping the company on the path to profitability?

There is also uncertainty over how much generative AI will impact the RPA software industry and UiPath. Some think that generative AI will lower the bar to entry into the RPA market and hurt UiPath’s competitive positioning. With all of the uncertainty surrounding the company and the reduced guidance, the market had issues with the stock’s valuation.

Valuation

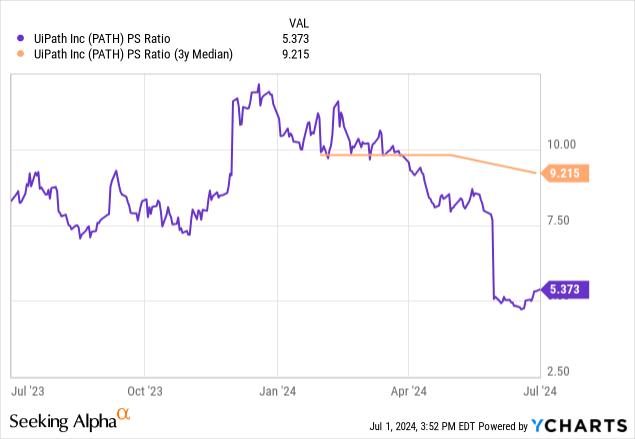

The following chart shows the massive drop in the company’s valuation post-May 29 earnings. The stock trades at a price-to-sales (P/S) of 5.373, well below its three-year P/S median of 9.215, suggesting undervaluation.

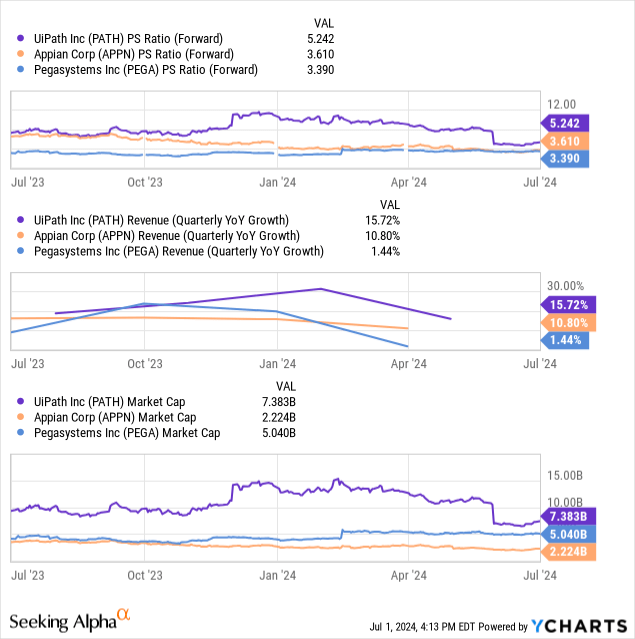

Let’s compare the company’s forward P/S ratio to several competitors. Although UiPath has the highest forward P/S ratio, it has the fastest revenue growth rate despite having the highest market cap.

One good rule of thumb for determining whether to consider a stock overvalued or undervalued is comparing a company’s estimated EPS growth rate to its forward P/E ratio for a given fiscal year. The market fairly values the stock if the two numbers match. The market may overvalue the stock if the forward P/E ratio exceeds the estimated growth rate. The market may undervalue the stock if the estimated EPS growth rate exceeds the forward P/E. The company has encountered short-term headwinds, so I prefer using FY 2026 numbers to this year’s. Since analysts’ consensus EPS estimates call for an 18.59% growth rate and the forward P/E is 28.38, some may call this stock overvalued. However, the highest analyst estimate calls for an EPS of $0.67, which translates to an EPS growth rate of around 49% year-over-year, signaling undervaluation. Suppose UiPath’s forward FY 2026 P/E trades at a number equal to that 49% growth rate; the stock price would be 18.62, up 44.5% from its July 1 closing price of $12.88.

Suppose you are optimistic about the company in the longer term and think that management can hit the high end of analysts’ 2026 EPS estimates; it’s reasonable to believe that the company still has an upside at the current valuation. I call this stock an aggressive growth investment because an investor must make an aggressive assumption about the company’s future EPS growth to achieve a decent upside to the current stock price.

Seeking Alpha

Let’s do a reverse discounted cash flow analysis on UiPath.

UiPath Reverse DCF

|

The first quarter of FY 2025 reported Free Cash Flow TTM (Trailing 12 months in millions) |

$325 |

| Terminal growth rate | 3% |

| Discount Rate | 11% |

| Years 1 – 10 growth rate | 10.9% |

| Current Stock Price (July 1, 2024 closing price) | $12.88 |

| Terminal FCF value | $4.147 billion |

| Total Present Value of Cash Flows | 7.381 billion |

| FCF margin | 24% |

Analysts estimate that UiPath should grow revenue at a compound annual growth rate (“CAGR”) of around 12% over the next five years. Suppose the company can maintain FCF margins at 24% and maintain a revenue growth rate of at least 12% over the next ten years; the estimated intrinsic value would be $13.95, up 8.3% over the stock’s July 1 closing price. These assumptions are aggressive, since analysts only expect FCF to grow at a 1.63% CAGR and maintain an annual FCF margin of around 20% over the next three years.

There are some reasons for optimism

After now former UiPath CEO Rob Enslin suddenly left the company at the beginning of June, the company wasn’t left rudderless. One reason for investor optimism is that the returning CEO, Daniel Dines, was a cofounder, is very familiar with the company, and likely cares about seeing the company succeed. Dines has already addressed some of the execution issues the company ran into that have recently hurt sales. CFO Ashim Gupta said at the Williams Blair Conference:

The impact on sales compensation, fixed already. Just that is something that we committed to that we would fix in the quarter, and we are running with that. And then there is more of — as Daniel takes the helm of the CEO, that is fixing those deeper execution items on the go-to-market side, just being closer to the customer. We built…too many central organizations that slowed down the chain of information, and I think we can speed that up.

When Ashim Gupta talked about central organizations slowing things down, he likely meant that UiPath became too bureaucratic, which slowed down decision-making. Although he didn’t talk about the specific measures the company has taken, there are numerous things the company could have initiated to become nimbler in decision-making. Another issue CEO Dines is working on is breaking down silos within the company to improve communication and collaboration between the product development and the sales and marketing teams within UiPath.

Last, Gupta discussed underperforming growth investments. He said at the Williams Blair Conference:

When you look at the common theme of investments that have paid that we are not satisfied from an ROI [return on investment] standpoint that has been built over the last year or two. It’s really the central organization. The organizations that are furthest away from the customer…And we are putting together our thoughts in terms of go forward, but we definitely see both within sales and marketing and G&A. We see what you see, which is there — when you look at our benchmark, there is a continued — there’s a continued opportunity to drive efficiency without really sacrificing innovation or growth.

He didn’t specify what he meant by “central organization.” However, the term likely means company bureaucratic functions that don’t interact with customers. Some examples could be Human Resources, the finance department, the internal Information Technology department, or even product development teams. So, what Gupta likely meant by that statement, without getting overly specific, is that recent investments have been too internally focused on bureaucratic functions within the company and not focused on customer needs and demands. The result has been slow decision-making and less sales. Additionally, the company expects its new sales compensation impact to improve revenue this year and into 2025. If Daniel Dines achieves more efficiency while the company remains innovative and grows sales rapidly, UiPath may exceed analysts’ revenue growth and earnings expectations.

The company was an early adopter of Artificial Intelligence (“AI”). Some of the company’s earlier AI-powered products include Document Understanding and AI-powered Optical Character Recognition. CFO Gupta said at the William Blair 44th Annual Growth Stock Conference on June 6:

AI is like we said, has always been infused within our platform. So when you look back computer vision, as I talked about, that was embedded deeply within our platform. Task mining. You really need to understand and analyze data at scale and use AI to give the appropriate suggestions and inferences that are there. The advent of Generative AI has given us really an open source set of LLMs to build more efficiently specialized models.

The company has several of its generative AI Autopilot versions live for testing as of October 2023. The company says Autopilot helps developers code faster and accomplish complex coding tasks. According to the company, developers have found 70% of Autopilot’s suggestions helpful. CEO Daniel Dines briefly discussed AI on the first quarter earnings call:

I want to start by saying that the AI and Gen AI is a tailwind for us. And we have invested significantly over the years and in particular, over last year in Gen AI. In June, we are going to launch our first series of autopilots in GA [general availability]. And there is a lot of excitement around our customers about using our Autopilot to drive more adoption to reduce the time to value and overall reduce the total cost of ownership.

UiPath may benefit significantly from generative AI. People who are pessimistic about the company should remember that the benefits from generative AI represent a potential upside that has yet to kick in.

A buy for aggressive growth investors

This company has clearly run into near-term headwinds, and its recent drop in valuation is justified. While the company has potential upside in the future if it executes its vision, UiPath still has a limited operating history, poor recent execution, a weak macroeconomy, and some uncertainty because of a management change. Conservative investors might prefer established companies with lower risk profiles. Still, suppose generative AI proves to be a tailwind for the company and not a headwind to the business. In that case, the company may surpass analysts’ most optimistic revenue, EPS, and FCF estimates and justify the stock’s current valuation. If you are an investor willing to speculate on aggressive growth assumptions, the stock is a buy at current prices. I maintain my buy rating on UiPath for aggressive growth investors.

Read the full article here

")

")

")

")

")