")

")

Investment Thesis

One Liberty Properties (NYSE:OLP) has some strong points such as:

- solid business metrics

- high dividend yield

- the ongoing shift towards a more industrial-oriented portfolio

However, it also has some weaknesses that shouldn’t be overlooked, such as:

- low AFFO per share growth

- no dividend growth

- high AFFO payout ratio

- a history of poor capital allocation decisions that lead to inefficient portfolio

Considering the above factors, I believe that OLP’s valuation is not justified when compared to some of its competitors. There are better alternatives within both industrial or retail-oriented property sectors, such as:

That said, I am bearish on OLP and don’t consider it as a reasonable addition to my portfolio.

Introduction

OLP is a diversified REIT with a portfolio heavily leaning towards industrial properties (responsible for ~65.9% of contractual rental income) and retail properties (~24.4% of contractual rental income). The rest of the contractual rental income is derived from, among other things, health & fitness centers, restaurants, and theatres. Let me already establish my general view on diversified REITs.

I prefer specialized REITs as they tend to outperform diversified REITs as they can focus on the sector of their core competence. For example, I consider Realty Income’s (O) diversification decisions as being forced by its size and weakness rather than strength as the new property sectors (e.g. gaming properties, data centres) lie far away from its core area of competence. However, I don’t intend to paint each diversification attempt with the same brush. I advocate for VICI Properties’ (VICI) expansion into the non-gaming experiential property sector or EPR Properties’ (EPR) portfolio reorganization to reduce the share of the theatre segment in its ABR.

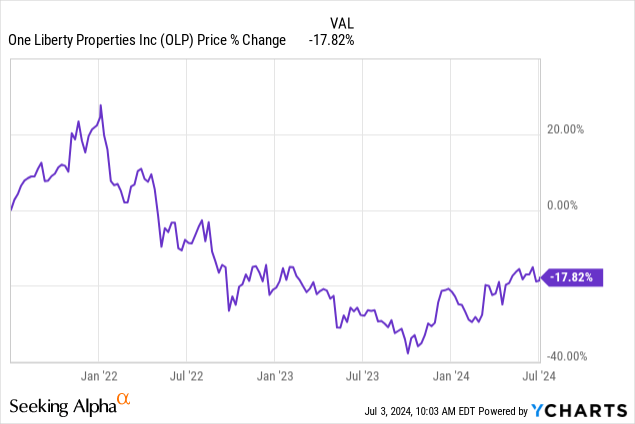

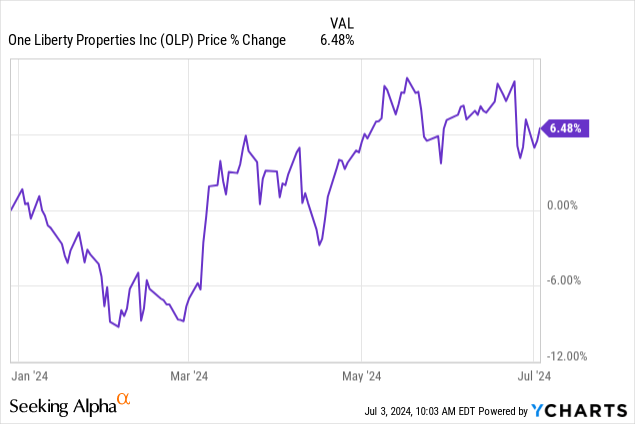

Therefore, each diversification strategy should be overviewed before stating an opinion. During the last three years, OLP’s stock price declined by 17.8%, which is not a surprise considering the REIT sector as a whole and the headwinds accompanying the industrial property sector. However, the stock price saw some recovery YTD and marked an increase of ~6.5%. Let’s examine whether OLP is worth considering as an addition to a well-structured portfolio, enjoy the read!

One Liberty Properties – Overview

The Business

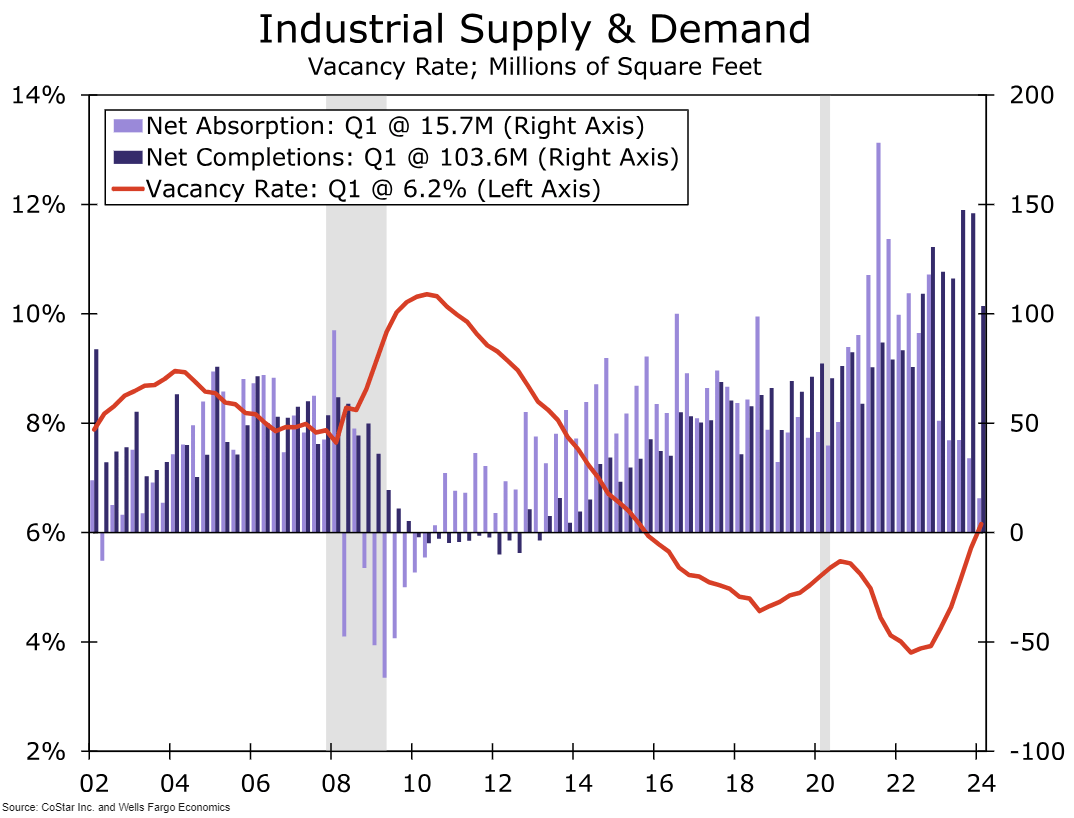

Most of OLP’s revenue is derived from the industrial property sector, which has been accompanied by headwinds related to the supply-to-demand relationship. As indicated within the Wells Fargo report:

- Q1 2024 marked a 7th consecutive quarter with net completions exceeding 100m sq. ft.

- the net absorption declined further and reached 15.7m sq. ft. – the lowest level since 2012

- as a result, the vacancy rate has increased to 6.2% – the highest level since 2015

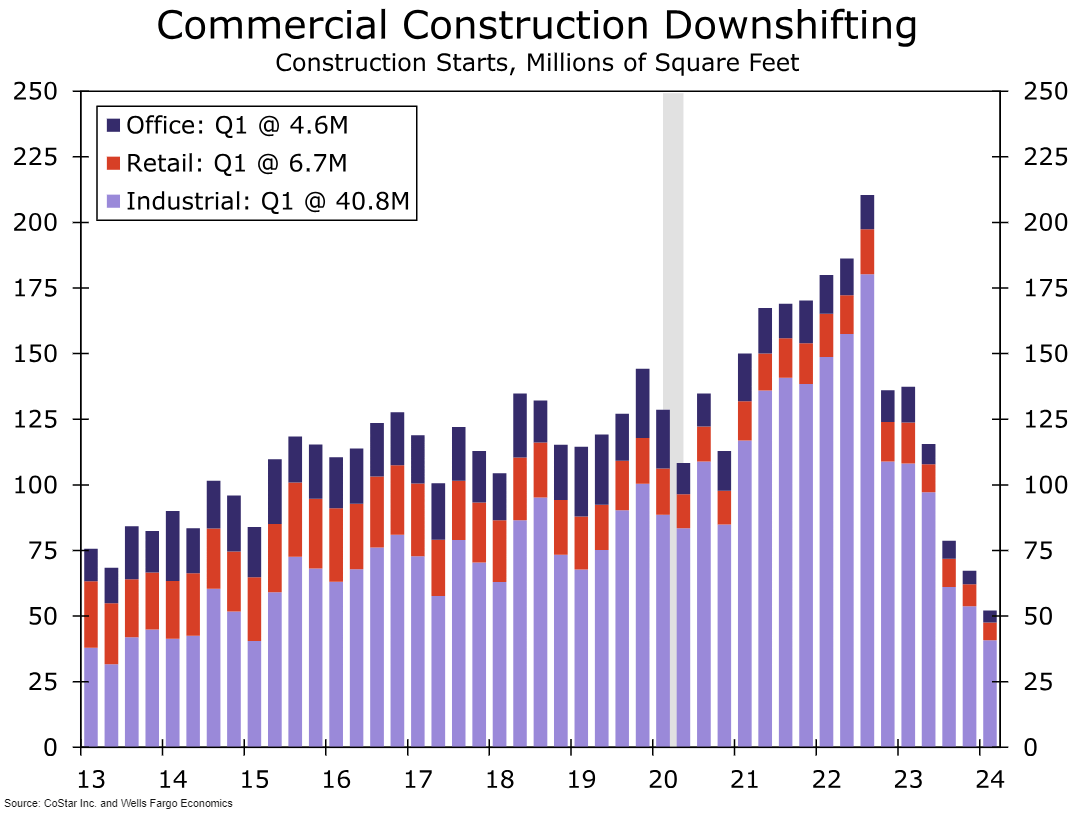

While some of the most recognizable sector representatives, e.g., the biggest industrial REIT in the world, Prologis, expect the headwinds to continue for the upcoming quarters, there are already first signs of an upcoming improvement in market conditions. Construction starts within the industrial property sector equalled 40.8m sq. ft. in Q1 2024 (a significant decrease since the peak of ~175m sq. ft. recorded in Q3 2022). With the demand accompanied by promising value drivers (demography, growing income, e-commerce) and low construction starts influencing the future supply, a positive shift in the supply-to-demand relationship can be expected.

CoStar Inc. and Wells Fargo Economics CoStar Inc. and Wells Fargo Economics

Regarding the business metrics, let’s start with the occupancy rate. As of March 2024, the Company held a high occupancy rate when compared to some of the most popular industrial property REITs, which amounted to 98.8%. For reference, the occupancy rate stood at:

- 95.5% for First Industrial (FR)

- 97.7% for STAG

- 97.7% for EastGroup Properties (EGP)

- 97.0% for PLD

However, one has to remember that the industrial property sector is not the only sector in which OLP is involved. The market vacancy rate for retail properties is considerably lower than the one for industrial properties, which improves OLP’s score. For reference:

- 99.6% for ADC

- 99.8% average since the IPO for Essential Properties Realty Trust (EPRT)

- 99.4% for NNN

Moreover, it’s worth emphasizing REITs with similar portfolio situations, i.e., with a majority of rental income derived from industrial properties, followed by income generated via retail/service-oriented properties:

Nevertheless, looking at the investment & disposition strategy of OLP, we may assume that the Company intends to grow the significance of its industrial property segment across the whole portfolio. Also, it already contributes the majority of rental income. Looking at the weighted average lease term (WALT), OLP is capable of securing solid lease terms on its agreements as its WALT stood at 5.5 years (as of December 31, 2023). For reference, the metric has recently stood at:

- 12.2 for WPC

- 4.4 for STAG

- 4.2 for TRNO

- 8.2 for ADC

- 14.1 for EPRT

- 10.0 for NNN

#2 Capital Allocation

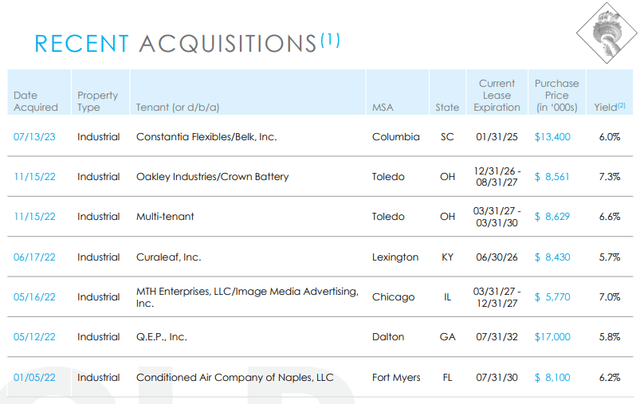

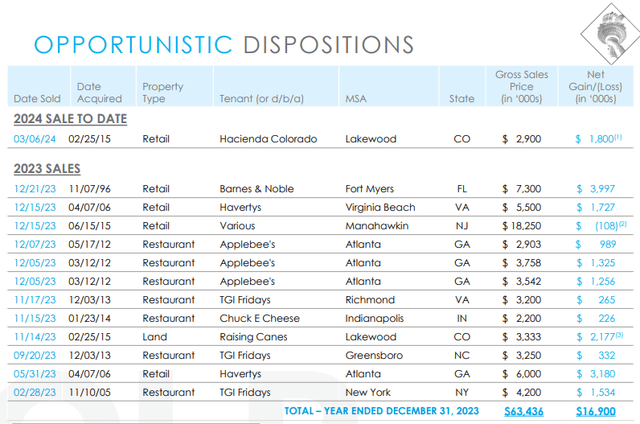

OLP’s strategy involves increasing the significance of the industrial property sector within its portfolio through industrial property acquisitions and disposals of other non-industrial properties. Each acquisition in 2022 and 2023 (with investment volumes of $56.5m and $13.4m, respectively) involved industrial property. Moreover, OLP acquired a single-tenant industrial property for $6.5m in April 2024. On the other hand, the property dispositions regarded mostly retail and restaurant properties.

OLP’s Investor Presentation OLP’s Investor Presentation

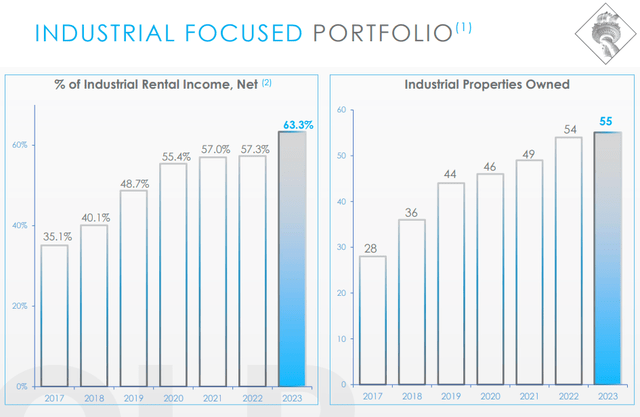

As a result, the industrial segment of OLP’s portfolio continues to increase its significance in terms of the property count and the share in its rental income, which grew from 35% in 2017 to 63% in 2023. Therefore, I’ve mostly referred to the industry property sector representatives.

OLP’s Investor Presentation

#3 Credit & Financial Stance

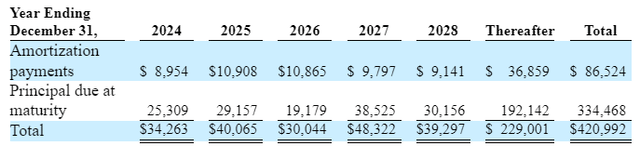

As of March 2024, the Company had a well-laddered maturity schedule for the upcoming years, with annual principal payments ranging from ~5-11% of its total mortgage debt. Therefore, even prolonging the high-interest rate environment will have a limited impact on OLP’s financial performance, especially given its fixed-rated debt orientation.

OLP’s Investor Presentation

However, OLP shows significant weakness in terms of its fixed charge coverage ratio, which amounted to 1.5x as of December 2023. For reference, the above metric stood at:

- 7.6x for PLD

- 5.5x for STAG

- 4.7x for WPC

- 4.6x for BNL

- 4.3x for NNN

- 5.9x for EPRT

- 4.9x for ADC

During the last three years, OLP delivered a low AFFO per share growth, which amounted to 2.6%, 1.5%, and 0.5% on a year-over-year basis in 2021 – 2023, respectively. For details, please refer to the table below.

| AFFO per share ($) | 2020 | 2021 | 2022 | 2023 |

|---|---|---|---|---|

| OLP | 1.90 | 1.95 | 1.98 | 1.99 |

On June 10th, 2024, OLP announced its quarterly dividend of $0.45 per share, upholding the status of an entity that increased or upheld its dividend for 126 consecutive quarters. OLP upheld or increased its dividend for over 30 consecutive years. The current dividend yield stands at a high ~7.8%; however, it hasn’t grown in recent years. Moreover, the forward-looking AFFO payout ratio exceeds my comfort levels and stands at ~93.8%. The credit & financial stance is a major weakness of OLP.

Risk Factors

The weakness of OLP’s credit metrics is certainly a risk to consider given the high interest rate environment and high payout ratio. Any events negatively impacting its financial performance could lead to the inability to increase or uphold its dividend.

Naturally, any financial turmoil regarding OLP’s tenant could translate into OLP’s issues, which is the case for each REIT. Moreover, the Company delivered a weak AFFO per share growth and was outperformed by the key market players. Should this tendency continue, OLP will generate lower total returns than its peers. Any other material adverse changes could negatively impact its financial stance and lead to higher stock price volatility.

Valuation Outlook & Key Takeaways

As an M&A advisor, I usually rely on a multiple valuation method, which is a leading tool in transaction processes. This method allows for accessible and market-driven benchmarking. While this method is not perfect (or any other), as there are no identical companies, it provides a reference point for the market sentiment. However, reviewing the specific factors that may influence a given multiple is crucial.

With that said, the forward-looking P/FFO ratio stood at:

- 13.2x for OPL

- 11.5x for WPC

- 10.6x for BNL

- 15.1x for STAG

- 12.8x for NNN

Also, PLD, EPRT, and ADC noticeably exceed OPL’s multiple.

Although OPL has some solid business metrics, high dividend yield, and ongoing portfolio restructuring towards industrial properties; the Company is accompanied by too many ‘red flags’ for my taste. Just to name a few of them:

- low AFFO per share growth

- no dividend growth

- high AFFO payout ratio

- a history of poor capital allocation decisions that lead to inefficient portfolio

Given the above circumstances, I don’t consider its 13.2x multiple justified compared to its peers. I won’t consider it a potential opportunity until its valuation multiple approaches a more suitable range (given its credit and business stance) of 10.0x-11.0x.

There are significantly more attractive investment opportunities in the current market. I have recently covered most of the REITs I’ve mentioned in this article, each offering a better risk-to-reward ratio. As each investor’s capital is limited, I prefer to allocate it to the leading industry representatives. OPL is currently not on that level; therefore, I have a bearish view.

Read the full article here

")

")