")

Investment summary

My recommendation for Veralto (NYSE:VLTO) is a buy rating. As a leading player in the segments it competes in, VLTO is set to benefit from multiple growth tailwinds in the coming years. In the Water Quality segment, growing demand for semiconductors and the US government’s focus on improving the country’s water infrastructure are key growth catalysts. As for the Product Quality & Innovation segment, consumer preferences to know what is in their packaged food, consumer packaging goods companies need for traceability, and pharmaceutical companies efforts to combat counterfeiting are major growth catalysts.

Business Overview

VLTO

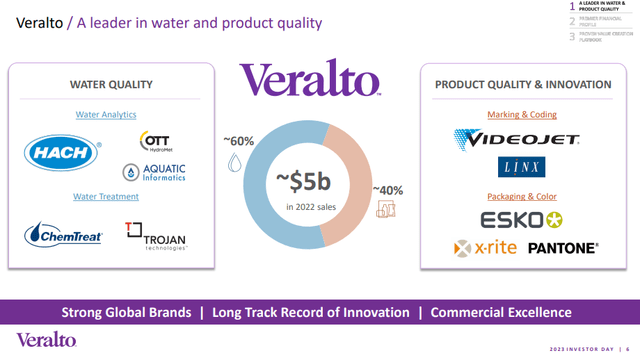

VLTO is a leading global provider of technology solutions to monitor water and product quality. The business was a spin-off of Danaher back in September 2023. As of FY23, VLTO generated ~$5 billion in total sales, of which ~60% comes from Water Quality [WQ] and 40% from Product Quality & Innovation [PQI]. The WQ segment offers products and services for water analytics and differentiated water treatment solutions to help reduce the environmental impact of industrial activity across residential, commercial, and municipal applications. The PQI segment provides solutions for packaging and end-to-end product tracking that enable speed to market, as well as traceability and quality control across industries such as pharmaceuticals and food and beverage.

Structural growth tailwinds for WQ segment

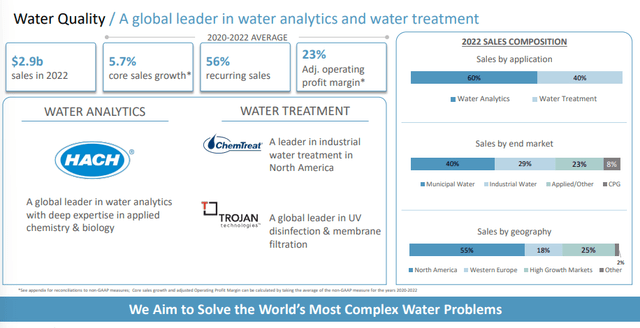

VLTO’s leading position in the WQ segment well positions it to benefit from the strong growth tailwinds in the US. North America makes up the majority of VLTO’s WQ sales (55.7%). Within it, industrial and municipal are the largest growth verticals, and I see strong growth catalysts for both verticals.

VLTO

Starting with the industrial vertical, the CHIPS act as well as an increase in semiconductor production globally to be significant growth catalysts for VLTA as the production of semiconductors requires ultra-pure water. Although the semiconductor industry has been weak in recent history, I believe the long-term growth trend remains positive as the world demand for digital tools and solutions, AI, autonomous driving, etc. will only drive up the need for more semiconductors. I expect VLTO to be able to capture demand because of its leading brands in the industry (ChemTreat and Trojan). Brand reputation is important because customers are unlikely to take the risk of using a cheaper alternative that is less trustworthy, given that the cost of failure is massive. Put another way, given that ultra-pure water is a vital ingredient to achieve optimal yield results (for chip production), it is likely that customers are willing to pay more to ensure they can achieve optimal yield.

Also, the extremely sticky nature of the relationship between VLTO and customers is due to the mission-critical nature of having access to ultra-pure water. Customers usually have to buy replacement parts or consumables on a regular basis once they have the instrument to keep it in good working order. This gives VLTO a competitive edge since its customers are more likely to stick with VLTO brand’s consumables because VLTO will not guarantee the product’s quality if they use a component from a different brand.

As for the municipal vertical, the growth catalyst is increased US government funding to solve the country’s water infrastructure problem. Indeed, the US government has stepped up on this. They recently announced another $5.8 billion in funding for America’s clean water infrastructure plan. Additionally, the EPA also announced $3.2 billion of funding through the Drinking Water State Revolving Fund, bringing the total to $8.9 billion to assist in getting clean drinking water to Americans, which will be used to upgrade water treatment plants. This is a clear sign that the US government is putting priority on this matter, and I expect these fundings to be catalysts for VLTO sales.

Looking ahead, I believe the US government is going to step up on the amount of funding because water utility systems have been underfunded for years, and based on the assessments by the EPA, over the next 20 years, the expected funding required is more than $1 trillion for drinking water and clean water infrastructure. Hence, the growth runway ahead for VLTO is visibly healthy, in my opinion.

Growth outlook for the PQI segment

VLTO

VLTO

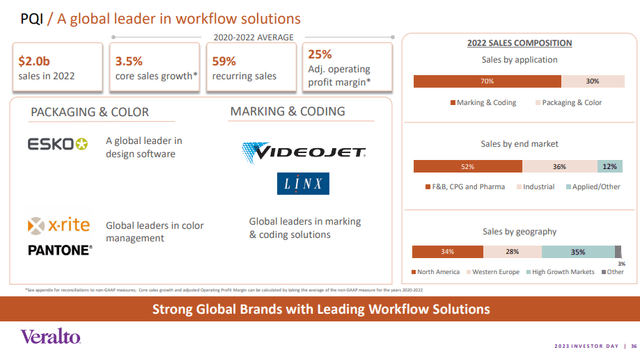

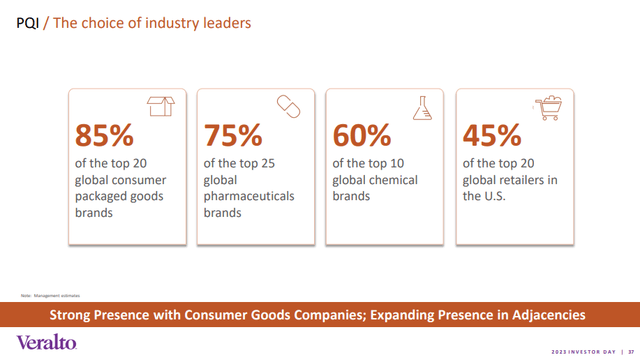

In the PQI segment (my focus is on the marketing & coding [M&C] sub-segment, given that it has the largest revenue mix), VLTO is also a leading player. We know that VLTO is a trusted player in the industry, as it serves 85% of top CPG companies and 75% of top life science and pharma companies. This feat validates the trust placed in VLTO’s brand. M&C is becoming increasingly important for consumer packaged goods [CPG] and pharmaceutical companies for multiple reasons, and they are growth drivers for VLTO.

VLTO

For CPG companies, the VLTO M&C solution enables traceability (in case the product goes bad, the CPG company can trace it); helps comply with regulations; and protects the brand name in case of dispute (ingredient list, allergen information, etc.). I believe these two factors are going to become more important as there is an increased demand for healthier food (consumers also want to know what is going into their food). The near-term concern is that inflation is going to hurt CPG volume (which hurts demand for VLTO services) as consumers look to cut back on spending. The good news is that inflation has certainly come down from 2023 levels, and although it has remained sticky, CPG volumes have started to show stabilization or improvement.

PWC

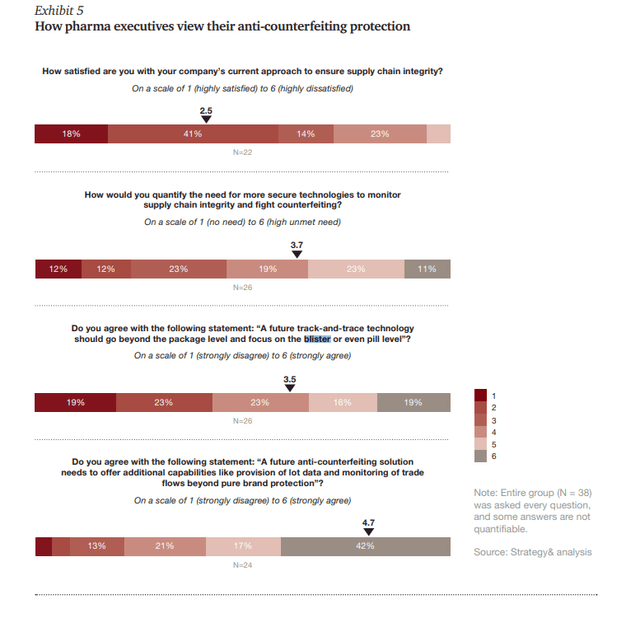

For pharmaceutical companies, the need to prevent counterfeiting and comply with regulations is a growth driver for VLTO in the foreseeable future. The former is the biggest problem, in my opinion, and that is driving more adoption of blister plastic films. This basically expands the VLTO use case (for instance, previously, codes were printed at the box level, but increasingly, prints are done at the blister pack level or pill level), which means more volume for VLTO. This also increases the complexity of the process, which means VLTO becomes more important in the process. In addition, like the CPG vertical, pharmaceutical companies are also subject to extensive regulatory scrutiny in regard to supply chain traceability, which I expect to be a permanent tailwind for VLTO.

Many recognize that adding barcodes to exterior drug packages provides far less protection than encoding products at the blister pack or even pill level. Several also expressed frustration with the short shelf life of traditional anticounterfeiting systems. Report by PWC

Valuation

Redfox Capital Ideas

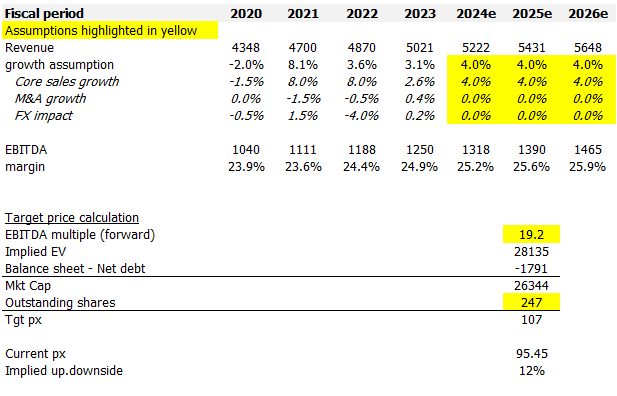

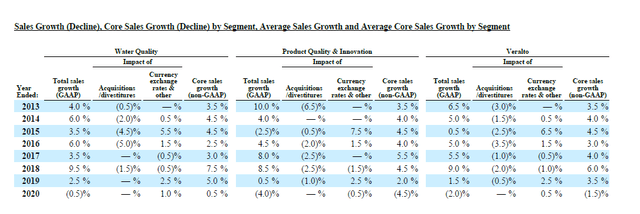

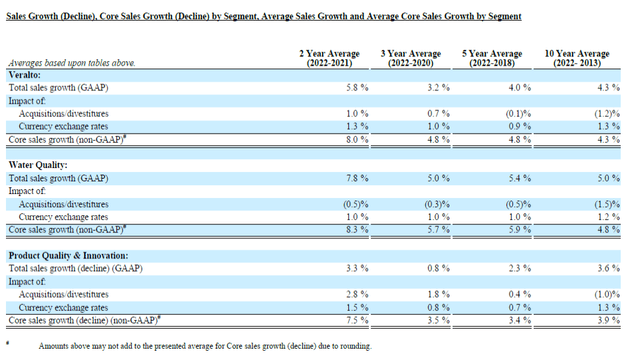

I model VLTO using a forward EBITDA approach, and using my assumptions, I believe VLTO is worth $107. While VLTO is a newly spun-off company, there are sufficient historical financials to rely on when forecasting the model (sales breakdown data available from FY13). Historically, VLTO has grown core sales (aka organic growth) at around ~4% on average (FY13 to FY19) pre-covid, and I am expecting VLTO to grow in line with this rate (CAGR basis). Growth could be higher, as the semiconductor industry growth outlook is certainly better today than it was a few years ago (for example, AI demand really only started to gain attention in recent years).

VLTO also has a history of expanding margins (adj. EBITDA grows faster than sales), and I believe margins can continue to expand as VLTO wins more recurring sales (which have a lesser cost associated with them than acquiring a new deal). Using the historical rate of ~35bps expansion per year (adj EBITDA margin went from high teens in 2002 to mid-20s in 2022, which I assumed to be 17.5% and 25%, respectively), I believe VLTO can achieve ~26% adj EBITDA margin in FY26.

The closest competitor to VLTO is Xylem Inc., which is a pure-play water treatment company. Given that VLTO has a very similar growth profile (~mid-single-digits growth outlook) but a higher EBITDA margin profile, I believe VLTO should trade at a slight premium to Xylem (Xylem now trades at 18.5x). Plotting both companies forward EBITDA multiple charts side by side shows that they trade basically in line with each other. As such, I believe VLTO should continue to trade at the current 19.2x.

VLTO

VLTO

Risk

Although there are signs of volume recovering for CPG companies, the sticky inflation environment is still a risk. While inflation has come down, there is no saying that it will not go up again. Suppose it goes up, and the Fed raises rates again. This would put a lot more pressure on consumer spending, which will indirectly impact VLTO growth. For the WQ segment, a slowdown in regulation as it relates to water quality is an inherent risk to the VLTO growth outlook, and this is something that is out of VLTO hands.

Conclusion

My view for VLTO is a buy rating. The WQ segment benefits from strong tailwinds in the US, driven by the CHIPS Act and increased government spending on water infrastructure. The PQI segment, particularly the M&C sub-segment, benefits from growing consumer demand for transparency and stricter regulations in the CPG and pharmaceutical industries. Notably, VLTO has a good track record of organic growth and margin expansion, which instils confidence in forecasting the business outlook.

Read the full article here

")

")

")

")

")