By Adam Meyers

Energy Dry Powder Spurs M&A

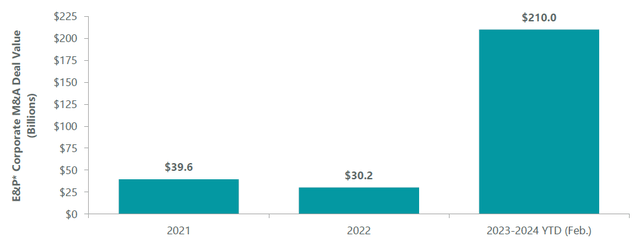

The beginning of 2024 has been anything but quiet within the energy sector. While 2023’s recessionary fears, lackluster demand from China, and range-bound oil prices produced subdued performance compared to 2022’s banner year, in which the sector’s 65% return made it the best performer in the S&P 500, the past few months have seen several high-profile acquisitions within the exploration and production (E&P) industry. These deals, including Diamondback Energy’s (FANG) acquisition of Endeavor Energy Resources, Exxon Mobil (XOM) buying Pioneer Natural Resources (PXD), and Chesapeake Energy (CHK) combining with Southwestern Energy (SWN), are merely the latest in the $210 billion worth of M&A in upstream energy producers over the past year — roughly 7x the total amount of M&A in the sector in 2022.

Exhibit 1: A Wave of Energy M&A

*Exploration and production. As of February 29, 2024. Source: Company Reports, Bloomberg, Daniel Energy Partners.

This wave of M&A activity highlights how the industry has made a significant pivot in its strategic priorities towards increased scale, efficiency gains, and greater capital discipline to provide sustainable dividends to investors. Rather than focusing on spending to grow their production levels, energy producers are increasingly looking to capture operating synergies with complementary acquisitions. They are also eliminating costs by reducing rig redundancies and optimizing production techniques. For example, Endeavor, prior to its acquisition by Diamondback, had prioritized double-digit production growth over capital discipline, leading to the quick depletion of its core inventory in the oil-rich Midland Basin. We believe Diamondback’s steady hand and focus on free cash flow generation will now allow the combined entity to rein back its production levels and extend the longevity of this high-quality acreage to fund cash returns. We see a similar dynamic playing out with ExxonMobil’s acquisition of Pioneer.

This M&A wave is also helping E&P companies increase their leverage over oilfield service companies, leading to better contract terms and lower operating costs. In 2015, the top seven producers in the Permian basin in Texas accounted for about 20% of total production. Today, they account for a little over 60%, leading to greater buying and pricing power when negotiating with oilfield service companies, which can support lower costs and higher returns.

Finally, the focus on capital discipline of these new, combined entities has prompted changes in how they are evaluating strategic planning and capital allocation. We are currently in an upcycle for international and offshore project spending but, unlike prior upcycles, this time companies are being more measured and conservative in their planning. The result is that over 90% of the offshore projects being pursued by major E&P companies are looking at breakeven points of $50 per barrel and below, which is still far below the $70–$80 oil prices we saw over the last year. In comparison, during the last upcycle in 2013–2014, some projects were being underwritten at prices of $100 per barrel to receive an economic return. This is also positive for offshore oilfield service players as their customers’ activity levels become less sensitive to commodity price weakness.

Ultimately, consolidation within the energy industry should be positive for investors. A leaner industry translates into higher-quality producers with longer inventory life, and a higher percentage of low-cost projects to support cash returns business models. A focus on more resilient and economic production projects as well as low debt levels should also help to mitigate the risk and volatility of oil prices.

Adam Meyers is a Vice President and Energy and Basic Materials Research Analyst at ClearBridge Investments. Adam earned a Bachelor of Science in Business Administration from Drexel University.

Read the full article here

")

")

")

preview")