Q1 2024 Earnings Call Transcript")

")

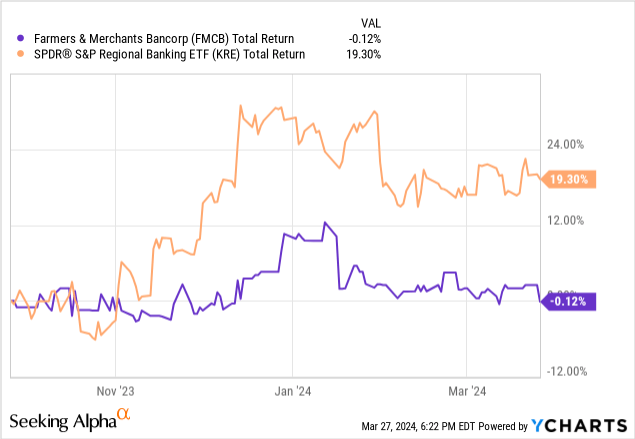

Tucked away on the pink sheets with pretty thin trading volume, life can often move quite slowly for the shares of Farmers & Merchants Bancorp (OTCQX:FMCB). Indeed, just as this California-based lender avoided the sell-off that hit other regional banks in the early part of 2023, it also missed out on the end-of-year rally, ultimately resulting in around 20ppt of underperformance since my last update in September.

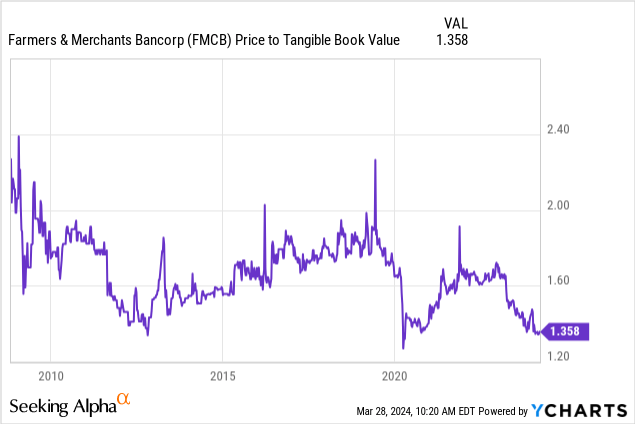

Headwinds to income stemming from higher funding costs and weak loan growth drove my Hold rating back then. While quality was/is not an issue with this bank, a then-valuation of 1.45x tangible book value per share (“TBVPS”) looked about right given FMCB’s mid-teens return on tangible common equity (“ROTCE”) and potentially declining earnings.

Earnings have been pleasingly stable here – better than I expected and representing a very strong performance given how tough comps were for regional banks in the second half of last year. With the shares now down to around 1.35x TBVPS, FMCB looks more interesting for long-term investors, and I upgrade the stock to Buy.

FMCB Recap

To quickly recap from initial coverage, FMCB is the holding company of F&M Bank, a circa $5b asset community lender that operates predominately in California’s Central Valley. As its name suggests, agricultural and agricultural real estate lending is a significant part of the loan book here, accounting for just under 30% of total loans at the end of last year. The bank is the fourteenth largest agricultural lender in the United States.

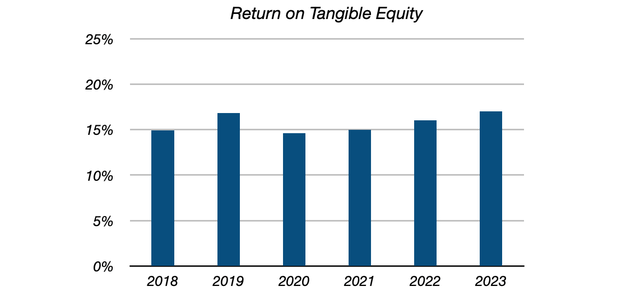

FMCB has consistently generated high quality earnings, with ROTCE averaging in the mid-teens area in recent years. As a mark of its consistency, ROTCE was in the double-digits even in years of very subdued returns for the wider banking industry, including in COVID-hit 2020.

Data Source: Farmers & Merchants Bancorp Forms 10-K

Cost advantages explain the above. For one, FMCB controls an excellent core deposit franchise, with non-interest-bearing (“NIB”) and cheap interest-bearing demand balances currently funding close to half of its balance sheet. On a blended average basis, these cost the bank a measly 9bps last year compared to an average interest-earning asset yield of over 5%.

Furthermore, FMCB has an excellent underwriting track record, consistently reporting very low levels of net charge-offs. During the Global Financial Crisis, for example, the bank’s annual net charge-off rate peaked at just 57bps – significantly lower than the industry average.

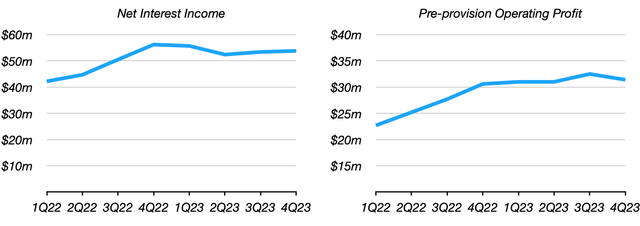

Income Still Relatively Stable

While funding cost pressure was a significant headwind for the industry in the back half of last year, FMCB has actually been reporting relatively stable income. At ~$107 million and ~$64 million, respectively, H2 2023 net interest income (“NII”) and pre-provision operating income were both basically flat on H1. Likewise, the Q4 annualized run-rates for NII (~$215 million) and pre-provision operating income (~$126 million) were also fairly stable.

Data Source: Farmers & Merchants Bancorp Forms 10-Q and 10-K

To be clear, both deposit migration and a higher cost of interest-bearing balances have been issues, it is just that these headwinds have been less severe here, allowing FMCB to largely offset them with modest loan growth and higher yields on earning assets.

Furthermore, the drivers of higher funding costs continue to moderate. NIB balances, for example, now look to have settled down having fallen steeply earlier in the year. End-of-year balances of $1.48 billion were actually a shade higher than Q3.

Deposit costs are also stabilizing, with Q4 interest expense of $13.6 million implying an annualized cost of funding of approximately 1.15%. That would make the figure around 11-12bps higher than Q3, but with the rate of change much lower than the 28bps increase seen between Q2 and Q3 and the 40bps rise seen between Q1 and Q2. As a result, Q4 net interest margin of around 4.2% was actually up a few basis points sequentially.

Sequential loan growth also looked fairly strong here at just under 3% in Q4 (versus around 0.9% for the industry). While one quarter doesn’t make a trend, loan growth could provide a tailwind to NII and pre-provision income this year in the face of likely lower interest rates, with the current forward curve and Fed guidance pointing to 75bps of cuts by the end of the year.

Credit quality continues to be outstanding, supporting net income and profitability. Net charge-offs were again virtually zero in 2023, with Q4 net income of $21.4 million mapping to a strong ROTCE of around 15%. Provisioning expenses of $9 million (~27bps cost of risk) resulted in a 15bps increase in the bank’s credit loss reserves, and with this now standing at 2.05% of gross loans FMCB remains conservatively placed to meet any downturn. That said, there is currently very little sign of deterioration in its loan book, with both NPLs and total past due loans essentially zero.

Shares Look Interesting At This Level

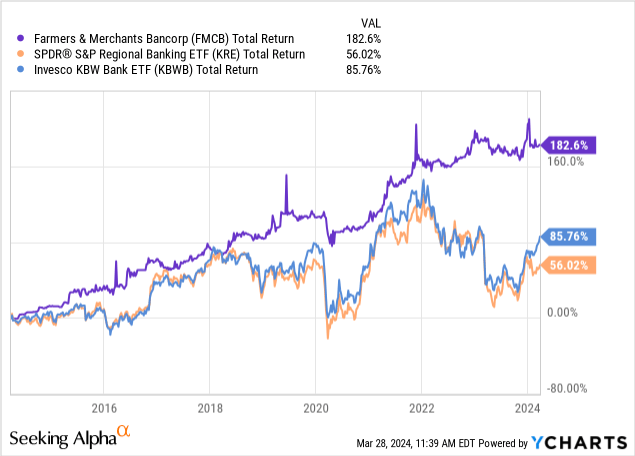

FMCB stock trades OTC and volume is typically thin. As such, this bank will probably only appeal to retail investors with a long-term buy-and-hold style outlook. While this also means the shares can drift from quarter-to-quarter, over longer-term horizons FMCB has outperformed various regional bank indices by a decent margin.

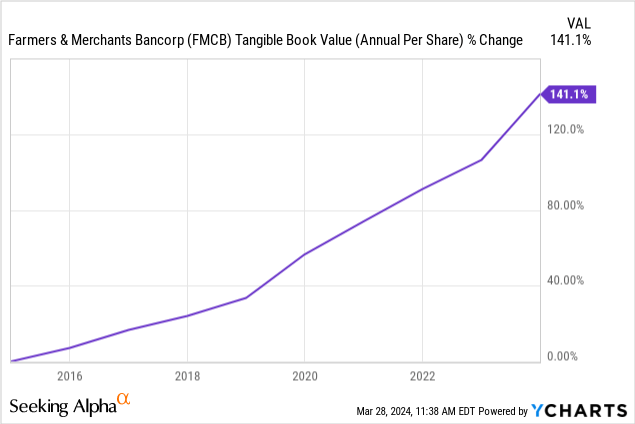

More importantly, the current valuation looks relatively attractive. TBVPS increased by around 17% last year to $717.50, and is around 8% higher than it was at previous coverage. As the stock price has been virtually flat in that time, its multiple has derated to just above the 1.35x mark. That is historically cheap; indeed, with the exception of COVID-affected 2020, investors typically haven’t been able to buy at these levels.

On a mid-teens ROTCE and 1.35x TBVPS, FMCB offers investors a nice double-digit internal rate of return. Capital returns are a bit so-so; the dividend payout ratio is just 15% of net income, equating to a current yield of just 1.8%, while the bank has been reducing the share count at a circa 2-3% annualized clip in recent years. However, FMCB has made up for this with stronger rates of balance sheet growth, increasing TBVPS at a 9-10% CAGR over the past decade.

Summing It Up

I stated last time out that I thought FMCB would offer investors better long-term entry points in the coming quarters. While earnings have so far been more resilient than I expected, these shares appear to trade at close to their lowest premium to tangible book value in years despite the bank still reporting very good levels of ROTCE. Between balance sheet growth, multiple expansion and its modest dividend, FMCB now looks priced for double-digit annualized returns for long-term investors, and on that basis I upgrade the stock to ‘Buy’.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here

")