")

Dear Fellow Investors,

The Partners Fund returned approximately 10% net in the fourth quarter and 13% net for the year.1 Please check your individual statements for your returns.

Investing is a creative endeavor. The combinations of what one can own are virtually endless among public companies, private companies, public debt, private debt, and a myriad of other financial instruments financial engineers have concocted over the years. Within public equities there are markets on six continents with an aggregate of over 50,000 listed companies. One can purchase shares directly or invest in a fund or even a fund of funds.

At the Partners Fund we have narrowed the investing universe at the manager level with our original criteria:

- One-person investment committee

- Concentrated holdings

- Reasonable amounts of capital (‘AUM’)

- Significant personal investments (“skin in the game”)

- Original thinking

- Mindset: getting rich is not the point

The logic of the Partners Fund criteria is that if we can find talented managers with fair and aligned incentives, we have a chance to grow our capital at attractive rates. Given the dynamics of compounding, a few extra points of performance per year lead to gargantuan differences over time. We don’t need all of the managers to excel – if just one or two are exceptional, we will do quite well.

We ended the year invested in 15 funds. They all fit the criteria outlined above, except for North Peak, which has an investment committee of two (they are brothers). The funds that we are invested in also have two other characteristics. The managers we invest in tend to invest in smaller companies, and some or all of their investments are international. We value these exposures for their diversification away from large companies that are better owned through ETFs and other passive options. However, as global market performance continues to be led by U.S.-based technology highflyers, both small and non-U.S. have been headwinds to relative performance, including in 2023.

Each manager has their own reason for allocating some or all of their portfolio to international equities. For Sixteenth Street (South East Asia) and Desert Lion (South Africa), their geographic focus is in their mandate. For other managers, it is likely a function of our “skin in the game” criteria. Speaking from personal experience – when you have the vast majority of your net worth in your fund, some geographic diversification lets you sleep better at night, and there are some wonderful companies at compelling valuations listed outside of the US. In aggregate across managers, I estimate that the Partners Fund has approximately 20% international exposure.

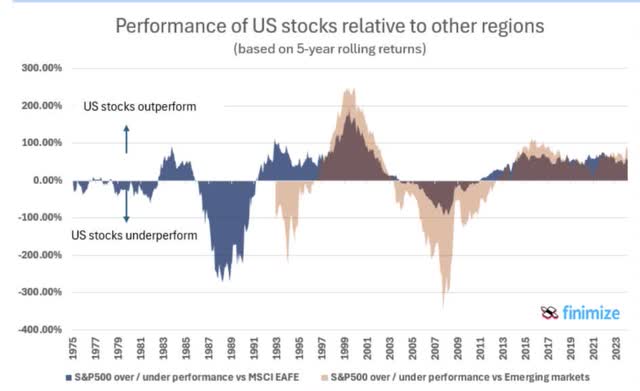

As the data below from Finimize shows, we remain in a very extended period of outperformance by U.S. stocks vs. their international peers on a 5-year rolling basis. In fact, it is the longest period of continued out performance in the last 50 years.

Can U.S. outperformance continue? Certainly. To better understand the situation, it’s worth noting the key components of the returns that have led to U.S. outperformance. From a high level, equity returns can be broken down into three primary buckets – dividend yield, growth, and multiple expansion/contraction. These three buckets are interconnected in various ways, so we need to look at them each on a standalone basis and then as a whole. The US outperformance started around 2012, so we will use that as a baseline:

US METRICS

Across all U.S. companies, the dividend payout ratio has remained roughly flat, growing from ~38% in 2012 to ~39% at year-end 2023. Meanwhile, the trailing EPS multiple has expanded by almost 60%, growing from ~33.7x in 2012 to ~53.0x at year-end 2023, and leverage for U.S. companies also increased substantially.

How do the same factors look for all European companies?

EUROPEAN METRICS

Interestingly, multiple expansion has been roughly the same for U.S. and European companies since 2012. However, European companies have increased their payout ratios and improved ROA despite reducing leverage over the same period. Can U.S. outperformance continue? Certainly, but the valuation discrepancies have widened and I believe that the tailwinds are more likely to become headwinds than permanent structural advantages.

At a more granular level, I encourage you to read the Sixteenth Street letter (attached) where PM Rashmi Kwatra lays out the investment case for MAP Active, the dominant activewear retailer in Indonesia. From my perspective, MAP Active is a compelling combination of exclusive brands with a long runway for growth, reinvestment opportunities, and an undemanding valuation. This is just one example of an international holding within the Partners Fund, and it is exactly the type of equity I want exposure to.

For those LPs that want a closer, first-hand look at one of our international investments, Desert Lion is hosting a visit for investors in Cape Town in April and has saved 2 spots for our LPs. South Africa is a complicated country and deserving of a large risk premium. The portfolio manager, Rudi van Niekerk, will expose visitors to growing companies with low single digit PEs that, while listed on the South African exchange, derive the majority of their revenue from OUTSIDE of South Africa. I recently visited South Africa with Rudi and left with an increased excitement on the investment landscape and glad that we have feet on the ground to help identify opportunities. If you would like to learn more or may be interested in joining the visit, please email [email protected].

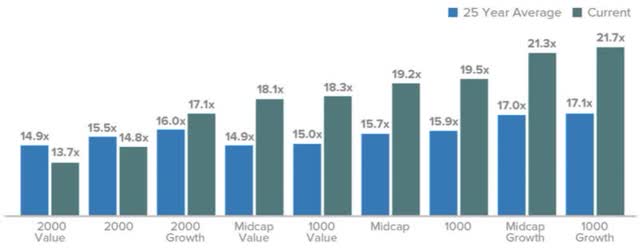

Now, let’s take a moment to explore the opportunity in smaller companies and why our managers may have gravitated there. For starters, one can argue that the valuations are more compelling. Here is a 2023 chart from Royce Funds which shows that the Russell 2000 and Russell 2000 Value segments of the market are currently sitting below their 25-year average valuation ratios.

According to Elliot Turner of RGA Investment Advisors, “Small caps make up less than 4% of the entire U.S. equity market, a level reached only twice before (the 1930s, the COVID crash, and now). Their performance relative to large caps over the past five years is in the 7th percentile, indicating a rare degree of relative underperformance.”

A visual representation of the outperformance of the largest companies relative to the smallest over the last 25 years can be seen in the to the right. The outperformance of the mega caps is currently the highest it’s been since the Dot Com bubble.

Can large cap stock outperformance persist? Absolutely – there is nothing magical about that level, but it is an interesting data point and suggestive of nearing historical boundaries. There are arguments that benefits of scale today are greater than ever before and, as David Einhorn of Greenlight Capital has suggested, because so much money is passive (index funds), price discovery may be broken. It is certainly surprising to me that Apple is larger than all of the Russell 2000 companies combined and Apple + Microsoft are larger than all of the publicly traded European companies combined.

I cannot say with certainty that size will become a burden for the largest companies. This time could be different, but what I do know with certainty is that smaller companies are difficult to access for investors. In fact, for large funds, they are virtually inaccessible. For the large $10B fund where a 5% position is $500M, investing in smaller companies in a concentrated fashion is simply not feasible. After extensive personal vetting over the many years of our relationships, I believe that the managers within the Partners Fund have the experience, aptitude, and structures that can allow them to capitalize when the tide turns. The ingredients for success are there.

As I have said at the end of every letter, our fund of funds is going to be different. It will be smaller, the underlying holdings will be more esoteric, and I hope the managers will continue to collaborate more over time. I believe that it will be “good different,” but only time will tell. Thank you for joining me on this journey. I will work hard to grow your family capital alongside mine.

Sincerely,

Scott

|

Footnotes 1Performance: (i) is representative of a “Day 1” investor in the Partnership, (ii) represents returns earned by Class B investors assuming a 0.75% annual management fee and no incentive allocation, and (iii) is stated net of expenses, including commissions, legal, audit, administration, and other. Year-to-date performance for an individual investor may vary from the performance stated herein as a result of, among other things, the timing of their investment and the timing of any additional subscription and withdrawals. Disclaimer: This document, which is being provided on a confidential basis, shall not constitute an offer to sell or the solicitation of any offer to buy which may only be made at the time a qualified offeree receives a confidential private placement memorandum (“PPM”), which contains important information (including investment objective, policies, risk factors, fees, tax implications and relevant qualifications), and only in those jurisdictions where permitted by law. In the case of any inconsistency between the descriptions or terms in this document and the PPM, the PPM shall control. These securities shall not be offered or sold in any jurisdiction in which such offer, solicitation or sale would be unlawful until the requirements of the laws of such jurisdiction have been satisfied. This document is not intended for public use or distribution. While all the information prepared in this document is believed to be accurate, Greenhaven Road Capital Partners Fund GP, LLC makes no express warranty as to the completeness or accuracy, nor can it accept responsibility for errors, appearing in the document. An investment in the fund/partnership is speculative and involves a high degree of risk. Opportunities for withdrawal/redemption and transferability of interests are restricted, so investors may not have access to capital when it is needed. There is no secondary market for the interests, and none is expected to develop. The portfolio is under the sole investment authority of the general partner/investment manager. A portion of the underlying trades executed may take place on non-U.S. exchanges. Leverage may be employed in the portfolio, which can make investment performance volatile. An investor should not make an investment unless it is prepared to lose all or a substantial portion of its investment. The fees and expenses charged in connection with this investment may be higher than the fees and expenses of other investment alternatives and may offset profits. There is no guarantee that the investment objective will be achieved. Moreover, the past performance of the investment team should not be construed as an indicator of future performance. Any projections, market outlooks or estimates in this document are forward-looking statements and are based upon certain assumptions. Other unanticipated events may occur and may significantly affect the returns or performance of the fund/partnership. Any projections, outlooks or assumptions should not be construed to be indicative of the actual events which will occur. The enclosed material is confidential and not to be reproduced or redistributed in whole or in part without the prior written consent of Greenhaven Road Capital Partners Fund GP, LLC. The information in this material is only current as of the date indicated and may be superseded by subsequent market events or for other reasons. Statements concerning financial market trends are based on current market conditions, which will fluctuate. Any statements of opinion constitute only current opinions of Greenhaven Road Capital Partners Fund GP, LLC and are subject to change, and Greenhaven Road Capital Partners Fund GP, LLC does not undertake to update them. Due to, among other things, the volatile nature of the markets, and an investment in the fund/partnership may only be suitable for certain investors. Parties should independently investigate any investment strategy or manager, and should consult with qualified investment, legal and tax professionals before making any investment. The fund/partnership is not registered under the investment company act of 1940, as amended, in reliance on an exemption thereunder. Interests in the fund/partnership have not been registered under the securities act of 1933, as amended, or the securities laws of any state and are being offered and sold in reliance on exemptions from the registration requirements of said act and laws. |

Original Post

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Read the full article here

Q3 2024 Earnings Call Transcript")

")