")

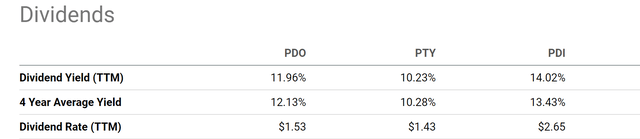

PDO CEF’s 12% dividend yield

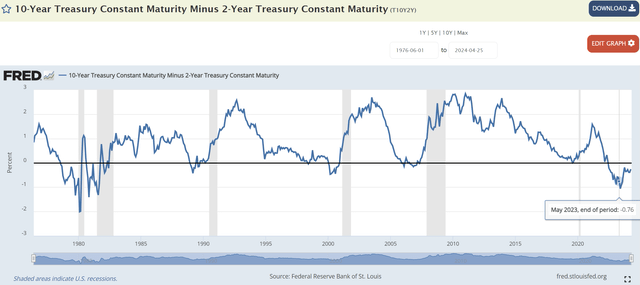

The PIMCO Dynamic Income Opportunities Fund (NYSE:PDO) is a relatively new addition to the PIMCO fund family. I’ve written two articles in the past to introduce this new member. In this article, I want to draw your attention to the first one I wrote back in May 2023 (see the chart below) because I am seeing a similar set of conditions currently. I was concerned about two specific risks: the inverted yield curve and the spread between the BAA and Treasury rates. Quote:

… the current yield spread between the 10-year Treasury Constant Maturity rates and 2-year Treasury Constant Maturity rates is -0.52%. To contextualize it, it is the deepest level of inversion in the past 3 decades. Even the 2000 episode did not reach this level.

… the current yield spread between high-yield corporate bonds and risk-free interest rates is also on the thin end of the spectrum.

I was concerned that PDO’s exposure (more on this later) would make it sensitive to such macroeconomic conditions. Indeed, the fund suffered a large correction shortly after, as seen.

Seeking Alpha

Today, I am seeing a similar macroeconomic setup (or probably even more concerning setup) compared to then and thus want to caution investors about the risks lurking beneath the 12% mouthwatering dividend yield, as you can see below.

Seeking Alpha

PDO CEF’s exposures

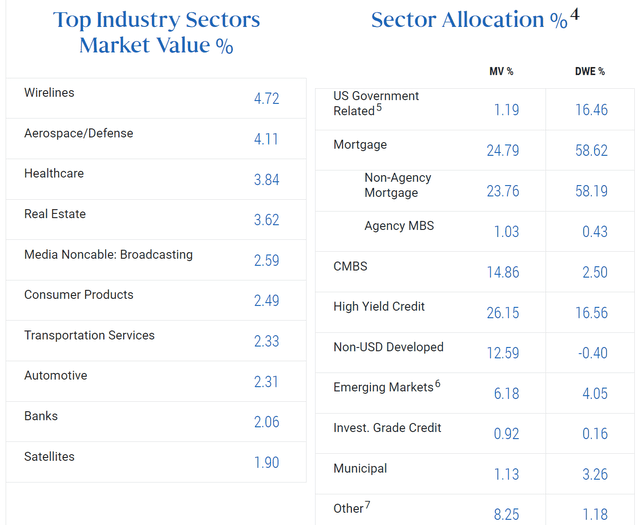

To explain the risks, we have to first take a closer look at PDO’s exposures. As described in PDO’s fund description (the emphases were added by me), it focuses on fixed-income instruments with a particular concentration on mortgage-related assets:

PDO manages the fund with a focus on seeking income-generating investment ideas across multiple fixed-income sectors, with an emphasis on seeking opportunities in developed and emerging global credit markets. The fund will normally invest at least 25% of its total assets in mortgage-related assets issued by government agencies or other governmental entities or by private originators or issuers. The fund may invest up to 30% of its total assets in securities and instruments that are economically tied to “emerging market” countries.

Indeed, as you can see from its detailed allocation below, mortgage-backed securities are its largest allocation, with a weight of 24.79% by market value, close to its allocation target. However, by duration-adjusted weight (“DWE”), mortgage-related asset represents a far higher weight of 58.62%.

Next, I will elaborate on the risks caused by such large exposure.

PDO fund description

The current setup vs. 2023’s

I have a pessimistic outlook for mortgage-related assets in the near future. I’ve written articles dedicated to mortgage REIT stocks recently to detail the reasoning. Thus, here I will just quote the essence of my chain of logic, so I can focus more on the current conditions that are directly relevant to PDO’s analysis.

Mortgage-related assets are sensitive to the yield spread between long-term rates and short-term rates. The thicker the long-short spread, the easier it is for mREITs to make money. The business model of mREITs is to primarily invest in mortgage-backed securities (“MBS”), which offer fixed interest rates based on the prevailing rates at the time of issuance. Wider spreads mean their longer-term MBS holdings generally offer higher interest rates compared to the shorter-term borrowings they use to finance these investments. This difference in rates widens their net interest margin (“NIM”), leading to increased profitability.

Against this background, a key reason for my concern back in 2023 was the inverted yield curve, as you can see from the chart below. At that time, the yield spread between 10-year and 2-year treasury rates was among the most negative levels in the past 3 decades. Such a negative spread has pressured PDO tremendously, as reflected by its large price correction afterward.

FRED

Then the yield spread began to widen (i.e., become less negative) and currently, it is hovering around zero, although still at a negative level of -0.26% as of this writing. So the next logical question is if the yield spread A) would keep widening and become positive or B) reverse the recent trend and become more inverted again.

I think B is a much more likely scenario than A. The gist of my logic is quite straightforward. First, the Federal Reserve only has control over short-term rates. On this front, I don’t think the Fed would lower the short-term rates in the foreseeable future given the persisting inflation. According to the latest PCE data,

The Core PCE Price Index, the Federal Reserve’s preferred measure of underlying inflation, rose 0.3% M/M in March matching the +0.3% consensus and the +0.3% pace logged in February. The core PCE number strips out volatile energy and food prices, which the Fed says provides a better view of inflation trends. By that measure, inflation kept up its elevated pace of the previous two months.

Second, longer-term rates are not controlled by the Fed by market dynamics. At times of uncertainties like this (with elevating geopolitical risks, inflation concerns, or even stagflation concerns), the market demand for safe-haven investments tends to increase, and long-term treasury bonds are a primary (if not the primary) safe-haven instrument. With 30-year treasury bonds’ yield hovering near 5%, investors can lock in a 5% return for the next 30 years – quite an appealing idea. Such market forces can drive up long-term bond prices and push down their yields.

Combining the above considerations, I see a large probability for the yield spread to reverse its recent trend and become more negative in the near future, putting pressure on the profitability and valuation of a large portion of PDO’s holdings.

Other risks and final thoughts

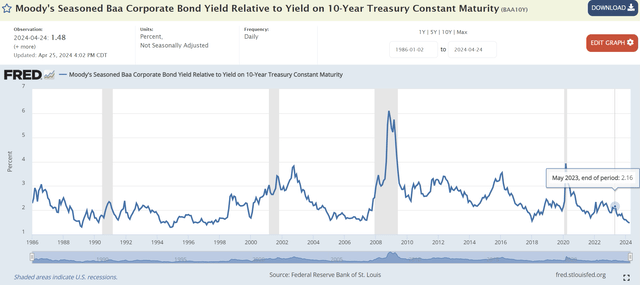

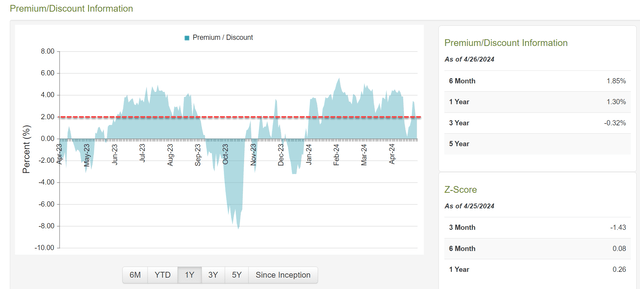

The other risks involve the yield spread between BAA corporate bonds and Treasury Rates (referred to as SBAA hereafter). As seen, the SBAA has become much narrower now compared to that in 2023 at my earlier writing. PDO’s exposure to investment-grade bonds is negligibly small. A thin SBAA translates to heightened risk premium in non-investment grade instruments in my mind. On a more positive note, the fund is currently trading close to its NAV as seen in the second chart below, which does not offer an obvious discount but does not signal too much overpricing risk either.

FRED CEFConnect

All told, I see a very similar set of macroeconomic conditions and risks associated with PDO CEF now compared to mid-2023. Based on the large price corrections the fund suffered following mid-2023, I think it is prudent for investors to take advantage of the recent price rebound and sell the fund. The fund’s 12% yield is indeed very attractive. However, a key lesson I learned in the 2023 episode is that such a yield won’t be sufficient to compensate for the risks and the fund can still suffer a large negative total return given its exposures. In particular, the fund’s heavy exposure to mortgage-related assets could be a cause for a negative total return, given my outlook on the yield spread.

Read the full article here

")

")

Q1 2024 Earnings Call Transcript")

")

")